https://www.facebook.com/NervoraBrainHealth

Art |

2026-05-23 12:14:13

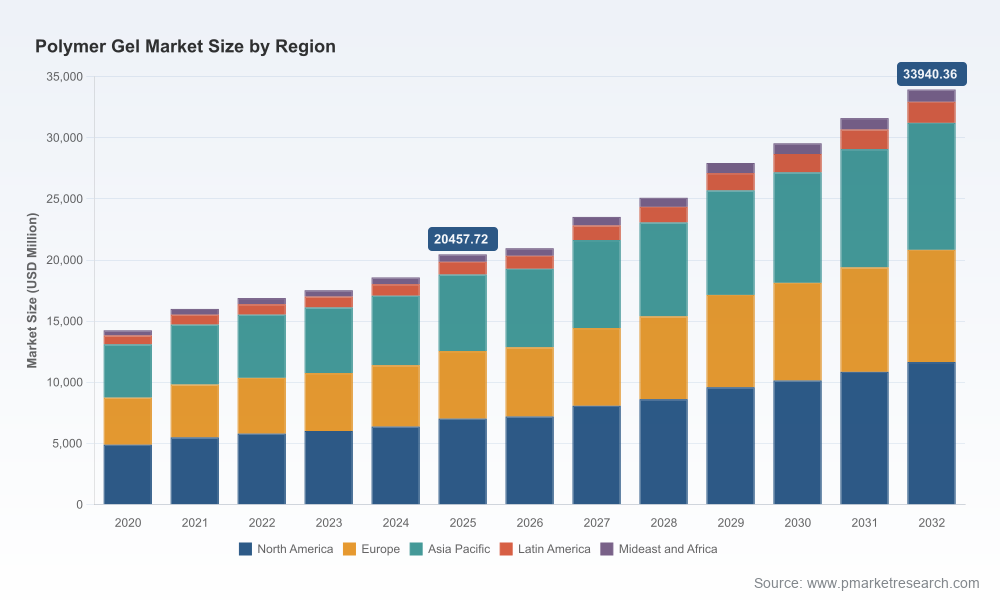

As companies prepare strategy and capital allocation decisions for 2026, the polymer gel market presents both clear growth opportunity and rising complexity. Our PW Consulting Polymer Gel Market report — grounded in a 2020–2025 historical baseline and a 2026–2032 forecast window — places the market within a disciplined commercial framework: the global market reached approximately USD 20,458 million in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 7.5% through 2032, reaching roughly USD 33,940 million by the end of the forecast horizon. These headline figures capture a market that is expanding steadily, but they mask meaningful variation by chemistry, application, and region — material insights that our full report disaggregates for commercial execution.

Polymer Gel Market

Investment timing and capacity strategy: With mid-decade capacity investments and pilot plants announced across leading producers, the market is at an inflection where near-term demand signals will determine which capacity additions are transformative versus marginal. Tactical decisions on greenfield vs brownfield expansion, pilot-to-commercial conversion, and modular-capex adoption will materially affect unit economics.

Polymer Gel Market

M&A and partnership targeting: The market’s moderate concentration (CR3 ~32.4%; CR5 ~48.2%) indicates room for consolidation in select value pools. Buyers should prioritize targets that deliver access to differentiated chemistries, regulated-market footprints, or step-change cost positions rather than broad-volume plays.

Polymer Gel Market

Supply-chain resilience and input-cost management: Volatility in key upstream feedstocks and geopolitical tariff actions necessitate hedging, vertical integration, or regional-sourcing strategies to protect margins and service-level commitments.

Performance-driven product evolution: End-markets with strict performance and safety requirements — notably healthcare and advanced industrial segments — are pushing suppliers to reformulate and engineer high-value polymer gels (e.g., hydrogels for wound care, specialty aerogel particulates for insulation and energy storage). Expect premiumization trajectories in niches where clinical, thermal, or electrochemical performance creates pricing power.

Regional demand rebalancing: Growth is not uniform. Mature markets will demand higher-value applications and regulatory compliance packages, while emerging regions will continue to drive volume growth in hygiene, agriculture, and personal care. Suppliers must match go-to-market models to these differentiated growth vectors.

Sustainability and regulatory embedding: New regulatory frameworks and material restrictions are altering formulation roadmaps and procurement sourcing. Regulatory-driven reformulation is both a risk and an innovation lever for incumbents and challengers alike.

The competitive map is composed of global chemical majors, specialty players, and regional specialists. Recent corporate activity underscores where leaders are placing strategic bets:

BASF SE (Ludwigshafen) completed a targeted SAP plant upgrade in Freeport, Texas (October 2025) focused on efficiency, logistics optimisation and carbon footprint reduction. This type of precision-capex indicates a play for differentiated cost-to-serve and sustainability credentials rather than simple volume expansion.

Evonik Industries (Essen) released an advanced superabsorbent polymer gel for wound care (July 2025), signalling product-led differentiation into clinical-grade materials where regulatory and performance barriers raise entry costs for competitors.

Sumitomo Seika (Osaka) executed both capacity expansion in Southeast Asia (June 2025) and a pilot SAP plant in Japan (May 2025), combining market-access and accelerated commercialization pathways — a classic “scale-fast, validate-fast” approach to regional demand capture.

Other players — spanning specialty formulators to raw-material focused firms — are selectively expanding capabilities in hydrogels, aerogels, and application-specific gels, underscoring a multi-front competitive dynamic between scale economies and application specialization.

Feedstock volatility: Acrylic acid — a primary upstream feedstock for many superabsorbent polymers and gels — showed material regional price movement into 2026. Price levels and directional shifts materially affect variable costs and margin sensitivity for producers and downstream formulators; scenario planning should incorporate both short-term price retractions and inflationary rebounds.

Regulatory tightening: The EU’s microplastics restriction and the prospective PFAS limitations are forcing early reformulation and additive substitution decisions. Suppliers that front-load R&D on non-intentional-microplastic formulations and PFAS-free alternatives will avoid costly late-stage reformulation and secure access to regulated tenders.

Trade policy and tariffs: Recent tariff actions on polymer imports create a near-term incentive to localize critical upstream intermediates or to redesign procurement strategies. Firms dependent on cross-border sourcing should model tariffs of 10% or higher into landed-cost calculations and evaluate tariff-engineering solutions.

Our report is built to inform boardroom and commercial decisions in 2026. We deliberately structure the content to transition leaders from insight to action:

Proprietary market model: A transparent, auditable demand-supply model with scenario toggles (feedstock price shocks, tariff pathways, and regulatory closures) so teams can stress-test capital and pricing strategies.

Commercial playbooks: Opportunity maps for product premiumization, regional go-to-market sequencing, and contract-structure templates for customers in healthcare, hygiene, agriculture, and industrial segments.

Supplier and asset due diligence packs: Technical and commercial dossiers for target assets and tiers of suppliers, including operational KPIs, CAPEX-to-IRR sensitivity, and de-risking checklists for pilot-to-scale conversions.

Regulatory tracker and reformulation matrix: A rolling legal-regulatory dashboard aligned to product categories, plus alternative-chemical pathways for PFAS and microplastics compliance.

Price and margin analytics: Unit-cost curves by manufacturing archetype, feedstock pass-through modelling, and recommended hedging instruments to stabilize gross margins during 2026–2028.

Reassess capacity near-term: Before committing to large greenfield projects, run a two-step check: (1) validate demand under conservative end-market scenarios and (2) quantify the margin delta from technology, location, and feedstock sourcing changes. Prioritise modular and reversible investments where possible.

Prioritize formulation-led differentiation: Invest in product-led R&D for clinical and high-value industrial substrates where technical specifications create defensible pricing. Collaborate early with key OEMs and clinical partners to shorten certification cycles.

Mitigate input and trade exposure: Build a layered sourcing strategy — combining hedged contracts, regional suppliers, and selective vertical integration — to smooth the impact of feedstock price swings and tariffs on margins and service commitments.

Embed regulatory foresight into product roadmaps: Use regulatory scenario planning as a product-development filter. This avoids stranded SKUs and opens premium channels where compliance is a barrier to entry.

Use M&A to acquire capability, not just capacity: Focus on deals that add proprietary chemistries, regulatory-compliant formulations, or customer intimacy in high-growth niches — transactions that raise CR5-level competitiveness without simply aggregating commodity volumes.

We designed the report as a decision-support instrument for C-suite and commercial teams: it translates macro growth (CAGR 7.5% through 2032) and headline market sizing into actionable scenarios, investment scorecards, and go-to-market playbooks. Rather than a static repository of numbers, the deliverable couples quantitative forecasts with qualitative strategy — competitor move analysis, regulatory mapping, and tactical templates that leaders can operationalise in 90–180 day cycles.

This release is a preview crafted to highlight the strategic framing and the critical levers that will determine winners and laggards in 2026. The full PW Consulting Polymer Gel Market report contains the detailed segmentation, granular regional and application breakdowns, company dossiers, and the interactive forecasting model necessary for tactical planning. To request the full report, schedule a briefing, or obtain tailored scenario runs for your portfolio, please visit PW Consulting’s research portal where the comprehensive dataset and consultant-led workshops are available.

2026 will be a year where disciplined strategy — not just optimism about volume growth — distinguishes companies that capture durable value in polymer gels. With measured investment, selective M&A, and regulatory-aligned innovation, market participants can convert the forecasted 7.5% CAGR into sustainable margin expansion and competitive resilience. PW Consulting’s new report is designed to be the operational blueprint for that conversion.

For detailed analysis of this topic, please visit the official page:Polymer Gel Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com