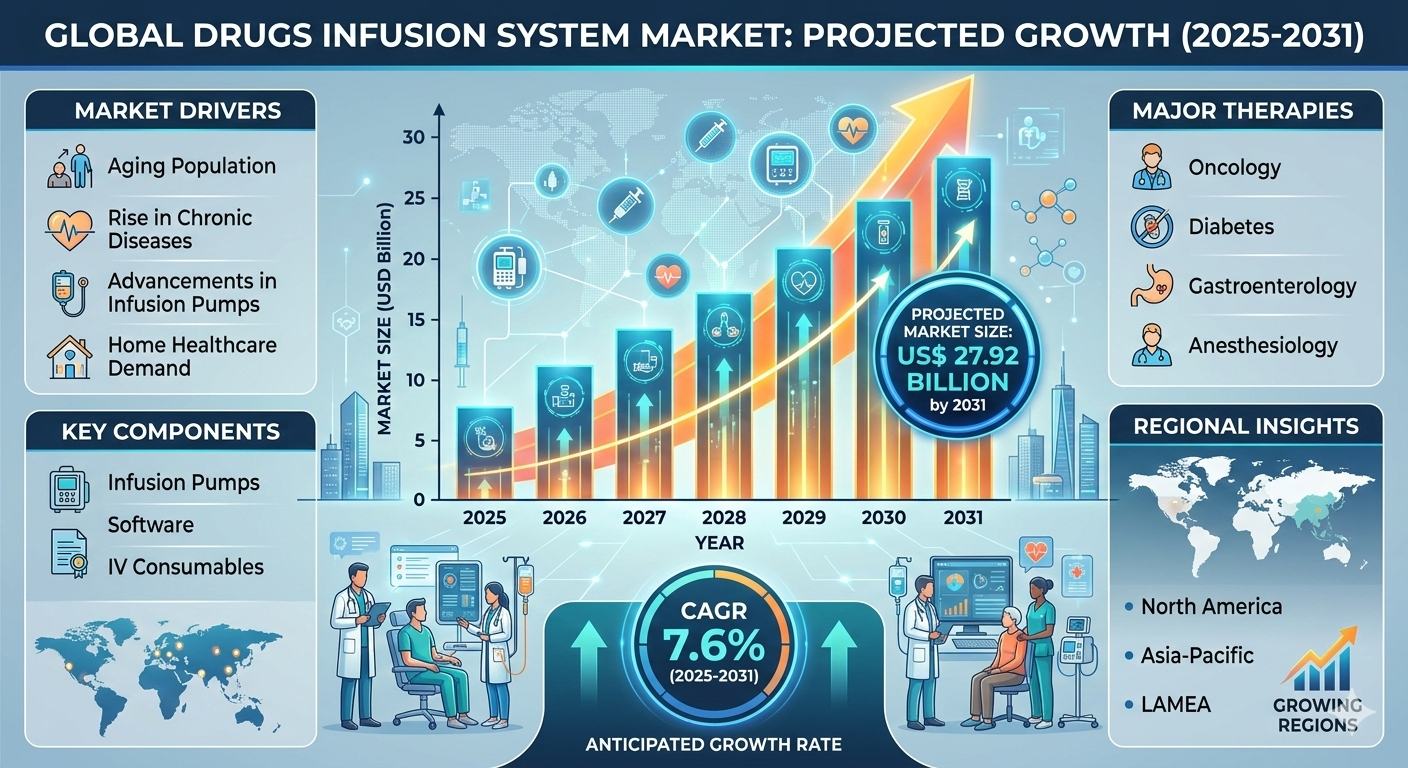

Drugs Infusion System Market to Reach US$ 27.92 Billion by 2031

Health |

2026-02-27 06:54:43

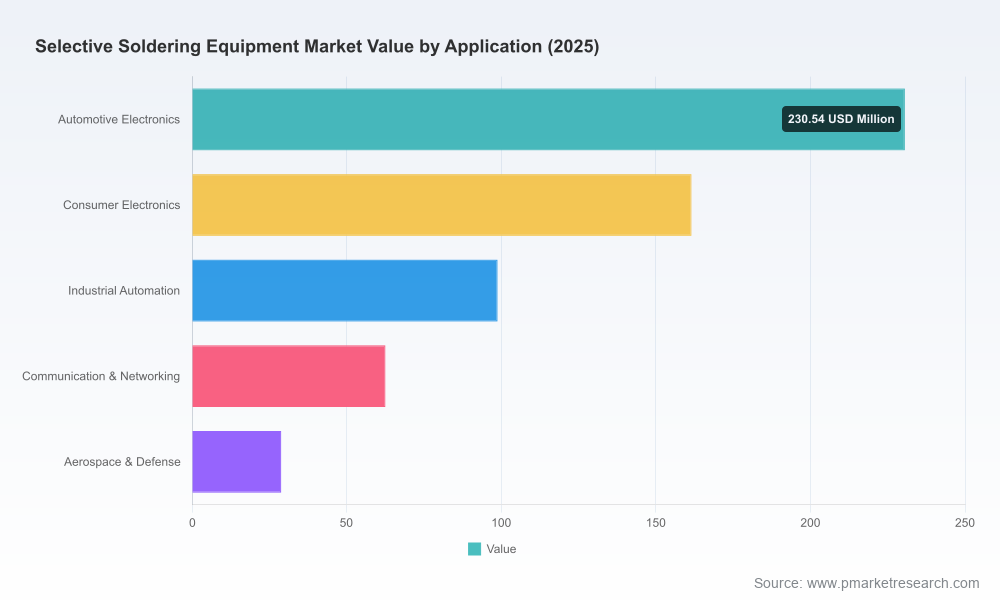

PW Consulting’s latest Selective Soldering Equipment Market report (base year 2025, forecast 2026–2032) synthesizes market-scale intelligence, supplier benchmarking, and decision-ready tools designed to inform capital allocation and operational strategies throughout 2026. The global market has expanded meaningfully over the past half decade — from roughly USD 420 million in 2020 to USD 582 million in 2025 — and our forecast hub for 2026 begins at approximately USD 663 million, reflecting a compound annual growth rate of 6.8% over the forecast window. This briefing highlights the report’s strategic value, the competitive dynamics you need to monitor, and the action-oriented playbook we recommend for manufacturers, C-suite executives, procurement leads, and private equity investors considering exposure to the selective soldering ecosystem.

Selective Soldering Equipment Market

Capital allocation is time-sensitive. Equipment lifecycles, lead times for specialized machines, and integration timelines into SMT lines mean procurement decisions made in 2026 will influence production capacity and cost curves for years. Our report aligns market timing with practical procurement and deployment scenarios.

Selective Soldering Equipment Market

Technology inflection points demand selective evaluation. Mixed-technology PCBs, lead-free mandates, and miniaturization are raising the bar on precision soldering. The report maps technology readiness, retrofit vs. greenfield economics, and total cost of ownership (TCO) tradeoffs across machine classes.

Selective Soldering Equipment Market

Supplier selection is now a strategic choice. Market concentration metrics indicate a moderately consolidated landscape (CR3 ≈ 48.6%; CR5 ≈ 64.2%), which creates differentiated access to service networks, spare parts, and upgrade roadmaps. Our analysis identifies which vendor strengths matter most by segment, geography, and production scale.

Robust market sizing and scenario models: longitudinal market sizing from 2020 through 2025 with point forecasts for 2026–2032, plus downside and upside scenario runs tailored to macro shocks and technology adoption curves.

Decision-ready TCO templates: capex-to-opex conversion models, nitrogen and consumables sensitivity analyses, and break-even calculators for retrofit vs. new-build investment cases.

Vendor benchmarking and scorecards: structured comparisons across product families, service footprints, spare-parts availability, software maturity, and upgrade paths — enabling defensible vendor shortlists and RFP criteria.

Integration playbooks: stepwise plans for pilot programs, line integration, quality validation (including IPC-related acceptance thresholds), and operator training plans to accelerate yield improvement and reduce time-to-first-build.

M&A and partnership intelligence: valuation heuristics, consolidation scenarios informed by market concentration, and strategic partnership vectors for OEMs, contract manufacturers, and component suppliers.

The selective soldering market blends deep incumbency with pockets of rapid innovation. Established platform providers coexist with high-engineering specialists and regional vendors that excel in retrofit and niche applications. Below are strategic synopsis notes on the names that shape vendor selection conversations in 2026.

Kurtz Ersa GmbH (Germany) — A global leader with modular VERSAFLOW and ECOSELECT platforms. Strengths include electromagnetic pump technology and multi-nozzle configurations that span entry-level to high-volume operations. Recent activity: launched the VERSAFLOW FIVE and showcased it alongside reflow/rework platforms at multiple industry expos in early 2026, signalling continued investment in throughput-focused systems.

Nordson SELECT (United States) — Offers a full spectrum of selective soldering solutions, including standalone, in-line, and multi-station systems backed by an extensive global service network. Their positioning is compelling for manufacturers prioritizing after-sales support and global spare-part continuity.

SEHO Systems GmbH (Germany) — Known for robust process design (fluxing, preheating, soldering zones) and high productivity platforms. SEHO’s engineering focus often appeals to customers seeking near-zero rework and consistent first-pass yields.

Pillarhouse International Ltd (UK) — Pioneer of the selective soldering concept with a patent-rich heritage. Best suited to buyers looking for high-engineering standards and proven platform architectures.

JUKI Corporation and Apollo Seiko (Japan) — JUKI brings batch-platform expertise (e.g., Cube series) while Apollo Seiko emphasizes robotic and dual-pot inline innovations. Apollo’s recent showings in late 2025 hinted at an expanded inline roadmap focused on precision for mixed-technology PCBs.

DDM Novastar, RPS Automation, TM Soldering Solutions, INERTEC, VennTek-SASinno, Hentec — These vendors occupy critical niches: cost-sensitive short-to-medium run systems, mini-wave precision solutions, legacy-system support, compact modular inline platforms, and regionally-focused supply. Their importance grows where speed-to-deployment, local service, or tailored engineering matter more than global brand scale.

Material and consumables interplay: The broader solder flux submarket is sizable and growing, and its dynamics affect consumables availability, pricing, and specification choices for selective soldering processes. Procurement teams should couple equipment decisions with proven consumable supply agreements.

Regulation and quality standards: Selective soldering is frequently deployed to meet stringent acceptance criteria (e.g., IPC-class requirements related to voiding). Industries such as aerospace, medical, and automotive require validated processes; equipment choices must be validated against those thresholds before scaling.

Technology adoption drivers: Miniaturization, lead-free mandates, and the proliferation of electric vehicle and ADAS electronics are structural demand drivers. These trends favor systems capable of high-precision micro-jet control, advanced flux application, and repeatable thermal control.

Labor and efficiency gains: Process comparisons show selective soldering can materially reduce solder usage and related operating costs versus legacy wave processes, while lowering nitrogen consumption when systems are optimized. These efficiency gains compound with scale and should be quantified in your TCO models.

Supply-chain and lead-time risk: Recent vendor product launches and ongoing trade-show visibility suggest product refresh cycles are accelerating. Buyers must balance first-mover advantages against integration risk and longer-than-expected lead times for popular models.

Prioritize pilots aligned to your highest-risk boards: Run short pilot programs on mixed-technology and lead-free boards that historically have had the most rework or yield variability. Use those pilots to validate vendor claims on yield, cycle time, and consumable usage.

Lock consumables supply concurrently with equipment procurement: Negotiated consumables contracts (flux, solder) reduce the risk of production interruptions and provide levers for ongoing cost savings.

Score vendors on service depth, not only machine specs: Given the market concentration dynamics, service network and upgrade paths materially influence long-term uptime and TCO.

Build retrofit pathways into capital plans: For many brownfield lines, modular inline solutions or hybrid retrofit kits deliver faster ROI than full-line replacements. Quantify retrofit vs replacement in your TCO templates.

Monitor consolidation for M&A opportunities: Mid-sized vendors with strong regional footprints can be attractive acquisition targets for in-house manufacturing expansion or to secure local service continuity.

Consider this briefing an operational trailer — it highlights trends, vendor positioning, and the strategic choices that will matter in 2026 without publishing the granular segment-by-segment figures that underpin our proprietary models. The full PW Consulting report contains the underlying datasets, interactive scenario models, vendor scorecards, sample RFP templates, and downloadable TCO calculators that procurement, operations, and investment teams can put into immediate use.

To access the complete intelligence pack — including the full breakdowns by machine class, application case studies, and our recommended shortlists for different buyer archetypes — visit the PW Consulting report page or contact your account lead. For decision-makers who must reconcile growth plans with practical execution timelines, this dataset and the associated playbooks are designed to close the gap between strategy and the factory floor in 2026.

PW Consulting — translating market insight into executable industrial strategy.

For detailed analysis of this topic, please visit the official page:Selective Soldering Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com