The Evolving Landscape of the Insourcing Contract Logistics Market Size

Other |

2026-04-22 13:07:12

PW Consulting is pleased to release a strategic preview of our forthcoming Suppository Base Market report. This brief synthesizes the report’s highest-value takeaways for executive teams, R&D leaders, procurement heads, and corporate development professionals who must make informed decisions in 2026. The analysis draws on a comprehensive historical series (2020–2025), a detailed base-year assessment (2025), and scenario-based forecasts through 2032. All monetary figures in the underlying study are expressed in USD (Million) and modeled against a central-case compound annual growth rate (CAGR) of 5.5% for the 2026–2032 forecast window.

Suppository Base Market

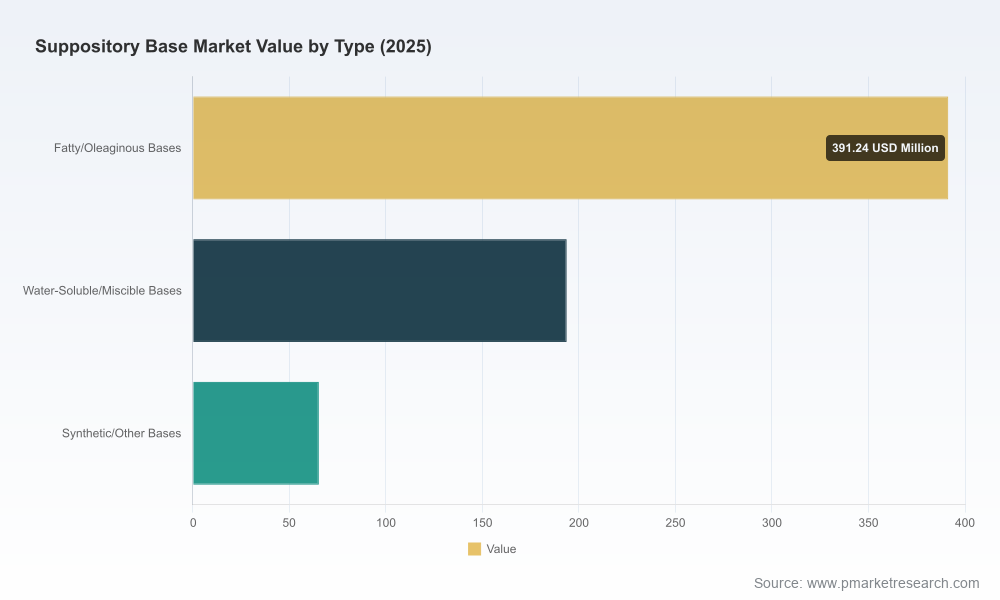

Suppository bases occupy an essential niche at the intersection of compounding pharmacies, generics injectables/ovules, and specialty drug delivery. After a stable recovery period through 2020–2025, the global market reached a meaningful scale in the base year (2025), reflecting both product innovation and renewed demand from outpatient and hospital compounding channels. Our base-case outlook—anchored to a 5.5% CAGR—projects continued expansion through 2032 underpinned by formulation diversification, increasing preference for vegetable-origin hard fats in regulated markets, and steady growth in therapeutic areas reliant on local mucosal delivery.

Suppository Base Market

For decision-makers, three strategic implications follow immediately:

Suppository Base Market

Our historical series shows steady expansion from 2020 to 2025, with the market scaling materially during the recovery and consolidation phase. The base year (2025) serves as the foundation for our scenario modeling across 2026–2032. The central forecast anticipates sustained growth, with a mid-horizon plateau and continued upside in the terminal years driven by incremental formulation uptake and geographic penetration.

Notably, the forecast curve exhibits non-linear behavior in response to episodic demand shifts and supply dynamics: tactical shocks in raw material availability or regulatory actions can compress near-term growth while accelerating substitution and innovation in later years. The 5.5% CAGR used for the central scenario is intentionally conservative, providing a robust planning baseline for capital allocation, capacity planning, and M&A prioritization.

Our full report contains a granular segmentation by region, base type, and application, supported by supplier-level share analysis and an exhaustive list of commercial grades. In this preview we intentionally avoid publishing core subsegment percentages and dollar splits to preserve the commercial sensitivity of those data and to direct readers to the full report for transaction-grade intelligence.

Qualitatively, the market structure reflects:

The market exhibits moderate concentration: the top three suppliers account for a meaningful but not dominant share, and the top five increase the cumulative share substantially. This structure creates a market dynamic where leading incumbents set technical standards and mid-sized specialists compete on formulation support and channel depth.

Key suppliers profiled in the report include established specialty ingredient producers and compounding-focused distributors:

Recent industry movements underscore these realities. For example, IOI Oleo’s 2025 catalog refresh emphasized registered grades and GMP production, reinforcing their positioning around quality compliance. In mid-2026, Medisca intensified promotion and availability of several natural and PEG-based bases to serve compounding demand—an action that illustrates distribution-focused competition and the importance of market presence at the pharmacy level.

Regulatory alignment is a core determinant of commercial opportunity. WITEPSOL®-type hard fats conforming to European Pharmacopoeia standards and produced under EU GMP—and with documented US FDA cGMP inspection histories—command preference in regulated procurement. Meanwhile, the USP maintains lists of commonly used bases (including hydrogenated vegetable oils and PEG mixtures), which continue to serve as the de facto technical baseline for compounding and regulatory acceptance.

Procurement teams should prioritize suppliers with transparent pharmacopoeial compliance, readily-available Certificates of Analysis, and documented inspection records. These compliance assets shorten qualification lead times for tenders and reduce the risk profile for hospital and institutional buyers.

The full PW Consulting Suppository Base Market report is built for direct application in corporate planning and includes the following actionable deliverables:

Based on our modeled scenarios and supplier analysis, we recommend five priority actions for corporate leadership:

Boards and C-suite teams will find the report useful across capital allocation, commercial strategy, and risk management conversations. The combination of a validated historical base, a conservative central forecast (5.5% CAGR), and scenario-based sensitivity analyses provides a defensible foundation for budgeting, capacity investments, and M&A valuation multiples. Supplier scorecards and contract-structuring templates are purpose-built to translate strategic intent into executable procurement and integration plans.

This preview is intended to demonstrate the practical depth of our Suppository Base Market research while reserving the segment-level splits, supplier share tables, and transaction-ready data for the full report. PW Consulting’s full study includes downloadable data tables (USD Million), granular segmentation, and proprietary concentration metrics that support a variety of corporate use cases.

For procurement teams, R&D heads, and M&A groups seeking the transaction-grade dataset and full analytical appendix, the comprehensive report and data workbook are available through PW Consulting’s research distribution channels. Engaging with the full study will enable you to convert the insights presented here into immediate sourcing actions, formulation programs, and inorganic opportunity assessments.

The suppository base market is neither niche nor static; it is evolving along lines that are meaningful for manufacturers, distributors, compounding networks, and healthcare providers. With a disciplined planning baseline (historical 2020–2025, base year 2025) and a central forecast framed by a 5.5% CAGR through 2032, corporate decision-makers in 2026 can move from reactive supply arrangements to strategic sourcing, targeted R&D, and selective consolidation. PW Consulting’s full report provides the operational templates and market intelligence needed to act with precision—ensuring your organization turns market growth into sustainable competitive advantage.

For detailed analysis of this topic, please visit the official page:Suppository Base Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com