Middle East and Africa AGM Batteries for Cars Market Overview: Key Drivers and Challenges

Networking |

2026-04-01 07:42:58

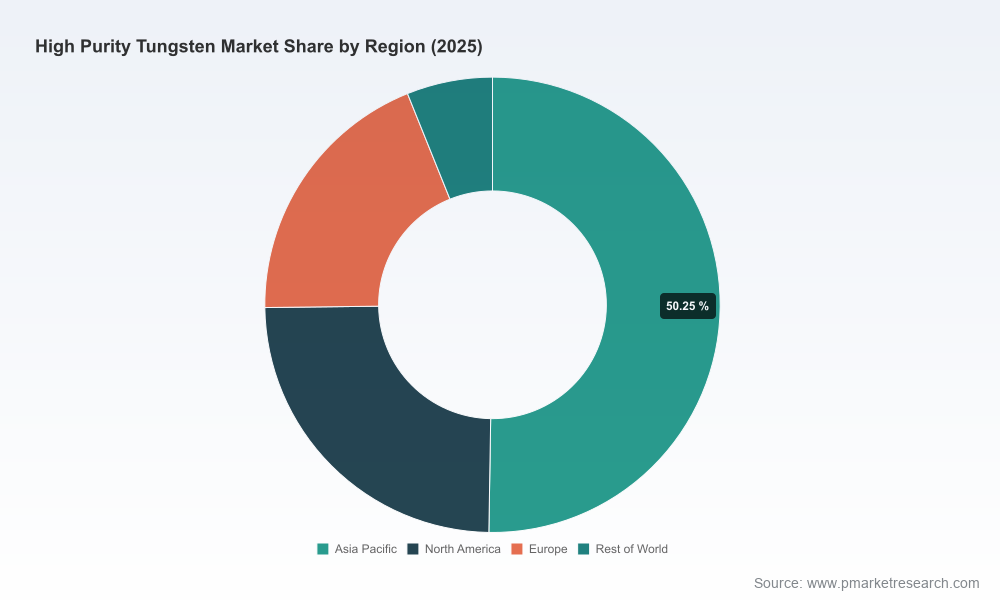

The global market for high purity tungsten — a critical enabler for semiconductor sputtering targets, advanced electronics, and high-reliability industrial applications — stands at a pivotal inflection point as companies set strategy for 2026 and beyond. PW Consulting’s new market study, grounded in an expanded historical dataset (2020–2025) and forward-looking forecasts to 2032, finds that the sector was valued at approximately USD 644.6 Million in 2025 and is forecast to expand at a compound annual growth rate (CAGR) of 6.5% through the 2026–2032 period, approaching the USD 1.0 Billion mark by the end of the forecast horizon. This research is designed as a decision-grade toolkit for executives, investors, sourcing teams, and public sector stakeholders navigating supply-chain disruption, policy shifts, and rapid technology evolution.

High Purity Tungsten Market

Supply-side volatility has become structural. Recent policy moves — including elevated U.S. tariffs on certain tungsten imports and new export controls instituted by major producing countries — have materially reshaped sourcing economics and transactional risk profiles. These shifts have driven raw material dislocations in 2025–2026 and prompted buyers to revisit procurement strategies that were tuned for stability, not strategic scarcity.

High Purity Tungsten Market

Feedstock and intermediary price dynamics: key upstream inputs such as ammonium paratungstate (APT) experienced notable price appreciation during 2025 and early 2026, and European benchmark APT indicators moved sharply as supply tightened. The result: increased feedstock cost pass-through risk for processors and end-users alike, and a renewed emphasis on cost-to-serve analysis across the value chain.

High Purity Tungsten Market

Geopolitical and onshore capacity initiatives are accelerating. New and expanded mine production in regions such as Central Asia and North America, together with project-level funding and permitting activity, are creating a multi-year rebalancing opportunity — but timing and quality of concentrates, downstream conversion capacity, and processing sophistication will determine which players capture value.

This is not a high-level narrative. The report is a working guide for 2026 decisions and includes:

Demand and supply modelling with scenario-based forecasts to 2032, reflecting alternative timelines for mine ramp-ups, export control regimes, technology adoption in semiconductors and displays, and macroeconomic sensitivity. (The report makes clear where baseline assumptions change materially under stress scenarios.)

Market structure and concentration analysis — including proprietary concentration metrics and competitive positioning assessments — that quantifies the relative heft of incumbent producers and identifies structural bottlenecks. Our market concentration analysis highlights the degree of supplier clustering and where single-point dependencies create risk.

Supply-chain risk heatmaps and mitigation playbooks that translate macro disruption into prescriptive actions: dual-sourcing priorities, minimum viable inventories by product grade, long-lead procurement checklists, and cost-optimization pathways under different tariff and trade-control scenarios.

Operational benchmarks and capex-to-output models for powder and mill-product producers, enabling rapid assessment of project economics for brownfield debottlenecking or greenfield capacity. These benchmarks include throughput-normalized capex, energy and yield sensitivities, and margin drivers across purity grades.

Commercial and M&A playbooks, including screening criteria for upstream assets, JV structures, and offtake frameworks. The analysis highlights target attributes that materially shorten time-to-market for critical high-purity grades and reduce counterparty risk.

Regulatory and procurement compliance matrices that align tariff exposure, export-control regimes, and national security procurement programs with sourcing options and contractual language recommendations.

The sector is characterized by a mix of integrated material producers, independent powder specialists, and regional champions. PW Consulting’s study profiles leading players — their business models, vertical integration strategies, downstream capabilities, and recent strategic moves — to help buyers and investors prioritize engagements.

Elmet Technologies LLC (Lewiston, ME, USA): A vertically integrated U.S. manufacturer producing tungsten metal powder via reduction of tungsten oxide and a broad array of mill products (plate, sheet, rod, and wire). Elmet’s integrated flow offers resilience for customers seeking nearshoring options and product traceability.

Buffalo Tungsten Inc. (Depew, NY, USA): A specialist powder producer with a long track record producing ultra-high-purity grades. Its experience in hydrogen-reduction routes and specialty carbide powders makes it an important supplier for niche high-reliability applications.

Global Tungsten & Powders Corp. (GTP): A broad-based producer with capabilities spanning powders, chemicals, and downstream components; part of a larger group that lends scale and cross-market reach, particularly into electronics and lighting.

H.C. Starck Tungsten GmbH, Plansee Group / Plansee SE, A.L.M.T. Corp., JX Nippon Mining & Metals, Xiamen Tungsten, Chongyi Zhangyuan, Masan High‑Tech Materials: These companies represent a mixture of European, Japanese, and Asian suppliers with differentiated strength in high-purity manufacturing processes, materials science innovation, and regional distribution networks.

Our competitive analysis does more than list names: it benchmarks technology routes (e.g., hydride-dehydride, hydrogen reduction, and chemical routes), evaluates downstream conversion capacities, and identifies which players offer the shortest supply chain for key end-markets. For executives considering partnerships or acquisitions, the report gives a calibrated view of capability gaps, integration complexity, and realistic timelines to commercial scale.

Project and exploration momentum in North America and Europe is shifting the supply calculus: several advanced projects have expanded land positions and regulatory approvals in early 2026, and offtake agreements are being used to de‑risk project financing.

Trade and export controls remain a dominant external factor: policy actions taken since late 2024 and through 2025 have materially altered trade flows and increased the effective landed cost of some Chinese-origin materials in certain markets.

Raw material pricing shocks in 2025–2026 have underscored the need for dynamic procurement and price-transmission modelling. The report includes a price-deck for APT and tungsten intermediates under multiple demand/supply scenarios to support budgeting and contractual hedging decisions.

Stress-test your sourcing strategy against at least three trade-policy scenarios. For many buyers, a mix of long-term offtake, strategic inventory, and nearshore partnerships will be superior to spot-market dependence.

Pursue targeted vertical integration only where it meaningfully shortens lead time or reduces single-source exposure. The economics of on‑site reduction/processing differ by purity grade — our capex-to-margin models show where integration unlocks value and where it does not.

Use supplier scorecards that incorporate geopolitical risk, processing technology, and ability to meet electronics-grade traceability requirements. The report includes a configurable supplier due-diligence template.

Prepare M&A and JV frameworks now. The market concentration metrics indicate material opportunity for consolidation and strategic partnerships — but success hinges on integration playbooks that preserve manufacturing quality and certification timelines.

Invest in product roadmaps that match purity and form-factor choices to your end-market roadmaps (for example, semiconductor targets versus display and photovoltaic applications). Small differences in grade and impurity profile can drive outsized manufacturing yield impacts.

Procurement leaders: quantify effective landed cost under tariff and export-control regimes and design contracts that allocate price and supply risk appropriately.

Manufacturing executives: evaluate brownfield debottlenecking versus greenfield capacity with clear capex and throughput benchmarks.

Investors and private-equity teams: screen assets and model exit pathways using sensitivity-tested EBITDA models tied to feedstock price scenarios.

Policy-makers and defense procurement offices: understand nearshoring options and the timelines required to build resilient domestic supply capability for critical materials.

PW Consulting’s study is intentionally deep on frameworks, scenarios, and executable guidance while preserving commercially sensitive segment-level datasets for licensed access. The executive summary above highlights the strategic levers companies must consider entering 2026: structural supply-risk, accelerating policy-driven realignment, and robust growth prospects underpinned by a steady mid-single-digit CAGR. For readers who require the granular regional and application breakdowns, supplier scorecards, downloadable financial models, and the full APT and powder price decks — all of which are essential for transaction due diligence and multi-year procurement planning — please consult the full report on PW Consulting’s High Purity Tungsten Market page.

For detailed analysis of this topic, please visit the official page:High Purity Tungsten Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com