Inorganic Feed Mycotoxins Binders and Modifiers Market — Strategic Briefing for 2026 Decision-Makers

Executive snapshot

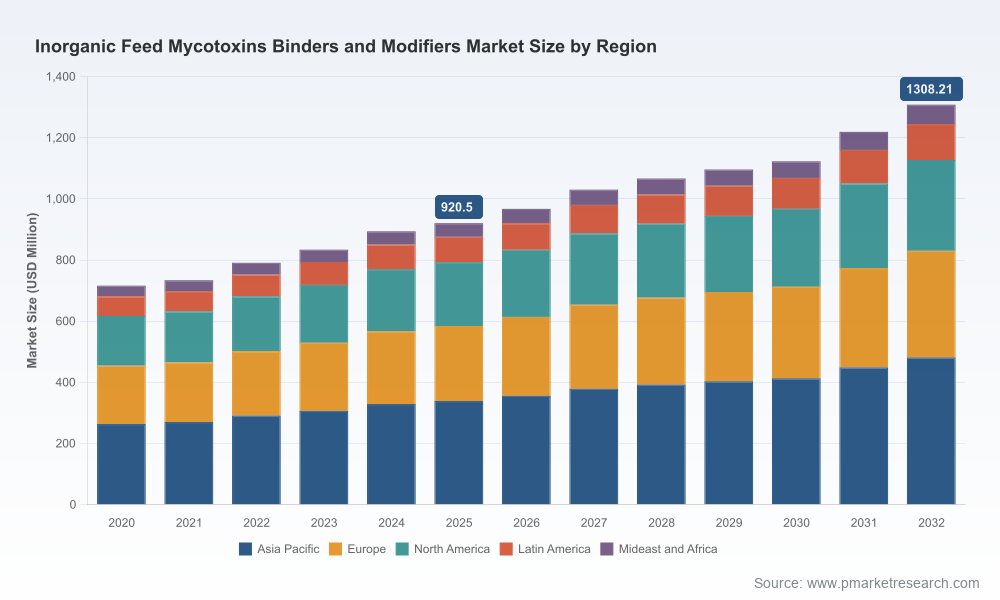

PW Consulting’s latest market intelligence on the Inorganic Feed Mycotoxins Binders and Modifiers market delivers a focused, strategy-ready synthesis for leadership teams preparing plans in 2026. Anchored on a robust base year of 2025 and a historical view from 2020–2025, the study combines rigorous market sizing, scenario-driven forecasts and pragmatic execution frameworks. Our base-year analysis places the global market at roughly USD 920.5 Million in 2025, with a forecast trajectory that grows to approximately USD 1,308.2 Million by 2032 (the 2026–2032 forecast period carries a compound annual growth rate of c. 5.15%).

Inorganic Feed Mycotoxins Binders And Modifiers Market

Why this matters for 2026 strategic choices

As supply chains normalize post‑pandemic and feed formulators prioritize animal health and yield resilience, inorganic mycotoxin binders are moving from niche risk-mitigation inputs to central components of feed strategy. The moderate yet steady CAGR we project signals a market that is sufficiently large to justify targeted investments — but also mature enough that scale, proven efficacy and regulatory alignment will determine winners. In 2026, executives face inflection points across four domains where our report is directly actionable:

Inorganic Feed Mycotoxins Binders And Modifiers Market

- Portfolio prioritization — deciding which binder chemistries and product formats to scale;

- Raw-material security — locking supply of mined clays and activated carbons under rising ESG scrutiny;

- Regulatory positioning — framing claims and trial design to satisfy EFSA and regional bodies; and

- M&A and partnerships — using inorganic binders as bolt-ons to broader animal-nutrition platforms.

What PW Consulting’s report delivers (practical, operator-focused content)

This is not an academic overview — it is a playbook for 2026 implementation. The report offers:

Inorganic Feed Mycotoxins Binders And Modifiers Market

- Market-sizing and trend maps: a verified historical series (2020–2025) and granular scenario forecasts across 2026–2032, with sensitivity analyses tied to raw-material pricing and regulatory shifts;

- Commercial due-diligence templates: seller and buyer scorecards, margin waterfall models, and quick valuation heuristics for bolt-on acquisitions in the inorganic binder space;

- Go-to-market blueprints: channel segmentation, premium versus cost-lead positioning, and multi-country launch checklists emphasizing feed mills, integrators and co-manufacturers;

- Regulatory & claims matrix: a navigable synthesis of regional approvals and accepted efficacy endpoints (including guidance on lab-to-field translation and nutrient-availability testing requirements);

- Procurement playbook: sourcing maps for bentonite, montmorillonite, sepiolite, zeolites and activated carbons; supplier risk-rating criteria; and contract clauses to mitigate grade volatility;

- Technical assessment framework: standardized trial protocols, KPI benchmarks for binding efficacy and safety scoring to compare competing inorganic chemistries;

- M&A target list and competitive heatmaps: prioritized candidates for acquisition and partnership aligned to strategic archetypes (scale players, specialty formulators, regional champions).

Competitive landscape — who matters and why

The market remains moderately fragmented: the top three companies account for a share that leaves substantial room for challengers, and the five-largest players collectively represent less than half of global revenues. This structure produces opportunities for consolidation, differentiated specialization and regional roll-outs.

- Amlan International (Oil‑Dri Corporation of America) — Chicago, IL, USA (https://amlan.com). Amlan’s focus on proprietary mineral technologies (notably Calibrin‑A and Calibrin‑Z) positions it as a technology‑led competitor. Recent activity includes product launches and partnerships aimed at India and Southeast Asia, signaling an aggressive go‑to‑market approach for poultry applications.

- Kemin Industries — Des Moines, IA, USA (https://www.kemin.com). Kemin brings broad feed-additive capabilities and an established TOXFIN range that leverages activated adsorbents; their strength is integrating inorganic binders into larger nutritional portfolios and global distribution.

- Tolsa — Madrid, Spain (https://www.tolsa.com). Tolsa’s product set combining bentonite, sepiolite and activated carbon caters to formulators demanding blended sequestration strategies. Their capabilities in clay processing and supply chain logistics are competitive differentiators.

- Bentoli Inc. — Cypress, TX, USA (https://www.bentoli.com). A focused supplier of clay-based solutions, Bentoli exemplifies the regional specialist model that can be attractive to strategic buyers seeking manufacturing footprint or niche technical expertise.

Notably, our competitive analysis does more than list incumbents: it scores companies on technical depth, route-to-market elasticity, regulatory readiness and acquisition appeal — metrics that are indispensable when building 2026 strategic plans.

Regulatory and raw-material dynamics that will shape 2026

Two intertwined forces determine near-term commercial viability. First, regulation: EFSA and EU frameworks emphasize demonstrated efficacy without compromising nutrient bioavailability or animal safety. For example, certain bentonite grades carry specific authorizations for aflatoxin mitigation under explicit inclusion limits — such nuances matter for labeling, claims and market access. Second, raw-material realities: inorganic binders predominantly derive from mined clays (bentonite, montmorillonite, sepiolite, zeolites) and activated carbons — commodities whose grades vary by deposit and processing. Our report models scenarios where grade availability, mining permitting and freight costs materially shift producer margins and feed-formulator adoption.

Recent industry moves — what to read into current signals

Public product activity in 2025 underscores two trends: rapid commercialization of differentiated mineral blends and region-specific partnerships to accelerate adoption. For example, a notable product launch and partnership targeted at India demonstrates how international formulators are prioritizing high-demand poultry markets with locally positioned offerings. Trade‑show showcases earlier in 2025 reinforced the importance of broad‑spectrum binders that claim efficacy against both polar and non‑polar mycotoxins — a capability increasingly expected by large integrators.

Strategic imperatives for 2026 (actionable recommendations)

Based on our integrated analysis, senior teams should prioritize the following:

- Fast-track regulatory dossiers for core products in priority markets. Invest in targeted field trials that align endpoints with EFSA-style efficacy expectations to reduce time-to-claim.

- Hedge raw-material exposure through dual-sourcing and toll-processing agreements. Consider backward integration or offtake arrangements for critical clay deposits where scale economics justify it.

- Adopt a two-tier product architecture: a cost‑efficient, commodity-grade binder for volume feed channels and a premium, validated binder (supported by peer-reviewed data) for intensive production systems.

- Pursue bolt-on M&A to gain processing capacity, regional distribution or specialty R&D — our M&A heuristics identify rational entry valuations and integration risk levers.

- Align commercial incentives with feed mills and integrators via performance-based contracts (e.g., outcome-linked rebates tied to aflatoxin reduction metrics), thereby accelerating adoption while sharing technical risk.

- Build a regulatory monitoring function to track subtle shifts in allowable inclusion rates, claim language and nutrient-interaction tests, converting compliance into a commercial advantage.

How executives should use this intelligence in 2026

C-suite teams and business unit leaders can extract immediate value from the report by using it as the basis for three rapid-decision workstreams:

- 90-day commercial pilot: select 2–3 formulations and conduct matched trials with strategic feed customers, using our KPI templates to measure ROI and inform launch commitments;

- M&A screening sprint: apply the report’s valuation templates to shortlist 6–8 targets, then run a two-week financial and technical deep dive on top candidates; and

- Supply security program: deploy our procurement scorecards to renegotiate supplier contracts and implement quality-audit checkpoints across critical mine sources.

Concluding note — depth without distraction

PW Consulting’s Inorganic Feed Mycotoxins Binders and Modifiers report is designed to be both a strategic compass and an operational manual for 2026. It provides the market-level sizing and validated CAGR to anchor investment theses while delivering pragmatic tools — from trial protocols to M&A playbooks — that shorten execution cycles. To preserve competitive advantage, this briefing intentionally omits the granular segment shares and regional breakdowns that are included in the full report. For the complete datasets, competitive heatmaps, and executable annexes that power tactical decisions, please visit our report page and request the full intelligence package.

For detailed analysis of this topic, please visit the official page:Inorganic Feed Mycotoxins Binders And Modifiers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com