Ultra White Rolled Solar Glass Market — Strategic Outlook for 2026

PW Consulting today releases an executive briefing distilled from our comprehensive Ultra White Rolled Solar Glass Market report (base year 2025, forecast 2026–2032). This briefing is written for corporate strategy teams, manufacturing executives, project financers, and policy leads who must make high-stakes decisions in 2026 anchored in credible market economics, competitive position, and near-term operational risks. The full report contains the granular segmentation, scenario models and vendor-level data that underpin the conclusions summarized here; this preview highlights strategic implications while intentionally withholding core segment-level figures to preserve the report’s advisory value.

Ultra White Rolled Solar Glass Market

Market trajectory you need to know

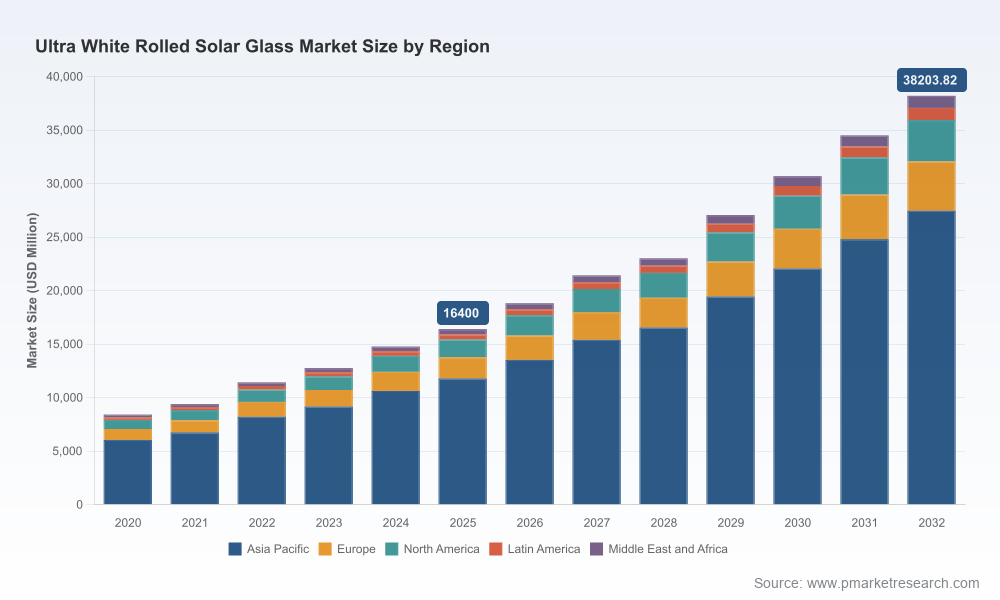

- Industry momentum: The global Ultra White Rolled Solar Glass market has demonstrated sustained expansion during the prior half-decade and reached a sizable industry scale in the 2025 base year. Our forecast horizon (2026–2032) assumes continued structural demand driven by module efficiency upgrades, rising BIPV applications, and supply-chain localization efforts.

- Growth rate: The market is projected to expand at a compound annual growth rate (CAGR) of approximately 12.84% through the 2026–2032 forecast window under our core scenario assumptions.

- Scale by 2032: Under base-case modeling, the industry reaches a multi-decade high by 2032, reflecting both accelerated replacement cycles in mature PV markets and large-scale deployment in emerging economies.

Why this matters for 2026 decision cycles

2026 is a pivotal year for players across the value chain. Policy timing windows, capital budgeting, and new capacity commissioning converge this year, creating discrete opportunities and risks:

Ultra White Rolled Solar Glass Market

- Capital allocation choices made in 2026 — whether to greenfield, brownfield, or retrofit — will be locked into asset lives that outlast short-term demand cycles. Our analysis provides CAPEX/OPEX ranges, break-even timelines and payback sensitivity illustrations to inform board-level capital approvals.

- Procurement and contract strategies for module manufacturers should prioritize supply continuity and product differentiation. Ultra white rolled glass suppliers with anti-reflective capabilities and patterning options are becoming table-stakes for frontline module efficiency gains.

- For project developers and OEMs, timing of module ordering against furnace commissioning calendars and domestic-content incentives can materially affect project-level economics. The report’s scenario tools translate market growth and policy windows into actionable procurement timelines.

Key market dynamics and risk vectors

- Demand dynamics: Upgrade cycles in crystalline silicon modules and higher adoption of advanced module formats are primary demand drivers. The market is also sensitive to BIPV uptake in select geographies and accelerating thin-film niche applications.

- Supply-side structure: The sector exhibits notable concentration—our concentration metrics indicate that the top three producers account for a majority share of global capacity, with the top five firms commanding an even larger portion of the market. This concentration influences pricing power, technology diffusion, and supplier conduct.

- Raw material exposure: Inputs such as ultra-low iron silica sand and specialty coatings introduce supply risk. While the underlying raw material markets are expanding, localized shortages or logistics disruptions can cause output volatility at furnace level — a core stress test included in our report.

- Regulatory and incentive environment: Evolving tax and subsidy frameworks in major markets materially affect manufacturing economics. Recent North American policy actions and incentive allocations have already shifted near-term location economics for patterned and rolled solar glass production; our regulatory scenarios quantify how different incentive mixes alter investment returns.

- Technology and product differentiation: Anti-reflective coatings, pattern geometry, and tempered processing are the principal levers suppliers use to improve module-level performance. Firms that pair material science with high-throughput production benefit from superior margin profiles.

Competitive landscape — what to watch in 2026

The market map in our report synthesizes capabilities, geographic footprints, technology mixes and strategic moves across incumbent and emerging players. Key observations:

Ultra White Rolled Solar Glass Market

- Leading integrated producers retain a structural advantage through scale, raw material integration and established module OEM relationships. These firms continue to invest selectively in additional furnace capacity and geographic diversification to serve faster-growing module clusters.

- Regional entrants and smaller specialized manufacturers are seizing niche opportunities — for example, localized supply in high-tariff markets, or premium product segments where ultra-high transmittance and tailored surface patterns command a premium.

- Recent new-builds and recommissionings in North America and Southeast Asia signal a shifting supply map. Domestic production restarts in the United States and commissioned facilities in Southeast Asia alter logistics and trade-arbitrage calculations for module makers and project developers.

- Strategic alliances and offtake frameworks are becoming more common as OEMs seek supply security; the report profiles typical contract structures, minimum take-or-pay terms, and pricing indexation approaches observed in current commercial practice.

Company vignettes (strategic takeaways)

- Major global manufacturers continue to drive scale and product breadth. Market leaders leverage high-throughput production, vertical integration and advanced coating capabilities to secure long-term OEM relationships.

- Well-funded regional players capitalize on local policy incentives and near-shore advantages to win share in their domestic or adjacent markets. Expect targeted capacity additions and product differentiation plays rather than broad global expansion from many of these firms.

- New U.S.-based capacity and expansions in North America are strategically significant for onshore supply chain resilience and domestic content considerations. These facilities are also changing the negotiation dynamics for module and system buyers seeking domestic supply.

What the report contains — practical tools for execution

Beyond narrative, the full PW Consulting report is an operational manual for strategic decision-makers. Highlights include:

- Top-down market sizing and three-tier demand scenarios (conservative, base, accelerated) aligned to policy and technology trajectories.

- Supply-side mapping down to furnace-level capacities, lead times for commissioning, and an assets-at-risk heat map that flags single-point-of-failure facilities.

- Benchmarking of CAPEX and OPEX for new-build and retrofit furnaces, including sensitivity tables for energy costs, raw material pricing and labor assumptions.

- Vendor and supplier due diligence templates — a practical checklist for offtake negotiations, quality audits and technology fit assessments.

- Commercial templates: model contracts, indexation clauses, and suggested hedging structures for glass supply agreements.

- Investment cases and M&A playbooks tailored to strategic buyers, financial sponsors and local manufacturers seeking bolt-on consolidation.

- Regulatory scenario analysis that translates alternative incentive designs into NPV and IRR impacts for representative greenfield projects.

Implications for three strategic stakeholders

- Manufacturers and CAPEX planners: Prioritize flexible furnace designs and modular coating lines to capture both current premium product demand and anticipated future shifts in module specifications. Align commissioning timelines with the 2026 policy windows to optimize access to available incentives.

- Module OEMs and integrators: Lock supply through multi-year offtake and invest in co-development agreements for glass–cell optical synergy. Factor in lead-time buffers and dual-sourcing strategies where concentration risk is elevated.

- Investors and project developers: Use the report’s scenario models to stress-test returns under shifting tariff, incentive and raw material cases. Financing structures that accommodate timing slippage and indexed pricing will be resilient in 2026’s volatile policy environment.

How PW Consulting adds value

Our analysis combines primary interviews with plant operators, procurement executives and technology providers, proprietary capacity-build schedules, and a bottom-up demand model calibrated against observed module shipments and announced project pipelines. The resulting report empowers executives to convert market intelligence into investment decisions, supply agreements, and regulatory engagement strategies.

Next steps — where to find the full intelligence

This release is intentionally selective. For access to the complete dataset, including segmented regional and application-level demand curves, furnace-level capacity tables, supplier-by-supplier benchmarking, and the full set of downloadable financial models and contract templates, please visit the PW Consulting report landing page. The full report is the recommended resource for any leadership team preparing for capital allocation, strategic sourcing, or M&A in 2026.

PW Consulting remains available to support bespoke analysis, scenario workshops, and transaction due diligence informed by the report’s findings. Engage our industry practice for tailored briefings or to commission confidential, deal-specific modeling.

For detailed analysis of this topic, please visit the official page:Ultra White Rolled Solar Glass Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com