https://www.facebook.com/ArthryonHeatReliefCreamNorway

Art |

2026-05-29 21:14:12

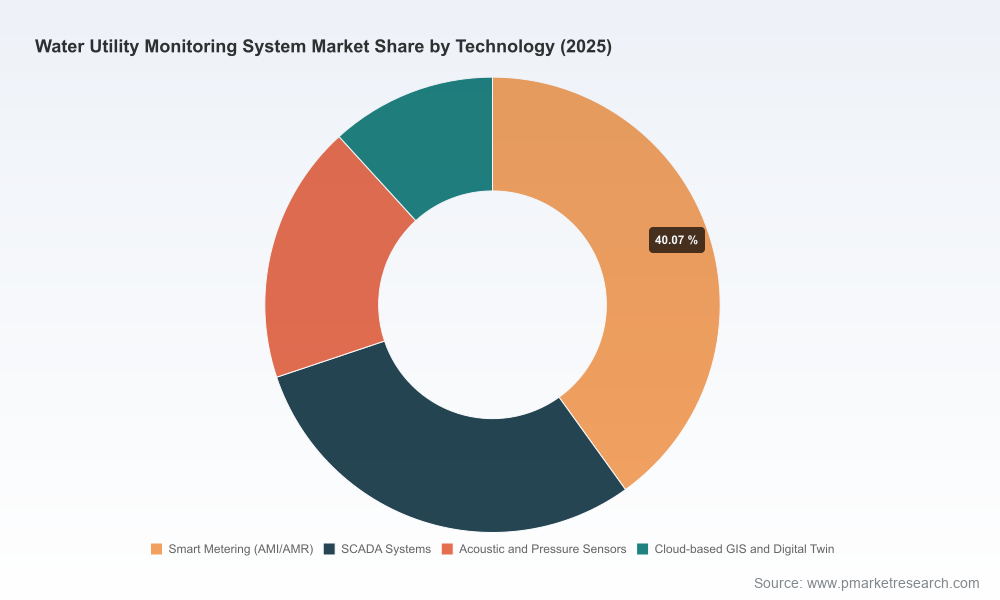

PW Consulting’s new Water Utility Monitoring System Market report (base year 2025; forecast 2026–2032) is designed as a decision-ready intelligence asset for utility executives, technology vendors, infrastructure investors, and municipal procurement teams preparing budgets and strategic plans for 2026. The sector has moved from early digitization pilots toward broad-scale operationalization: global market value more than doubled over the 2020–2025 window (rising from the low billions to over six billion USD by 2025) and is projected to continue at a robust compound annual growth rate of 14.33% through 2032, reaching the mid-teens of billions USD. This growth trajectory reflects accelerating deployments of smart metering, edge and cloud analytics, sensor networks, and solution-led services that together reshape how water is measured, managed, and monetized.

Water Utility Monitoring System Market

Timing and trajectory — The market is at an inflection point. Following strong acceleration in 2024–2025, 2026 will be the year many utilities move from discrete pilots to utility-wide rollouts. Organizations that align procurement, cybersecurity, and workforce transition plans to this timing will capture outsized operational and financial benefits.

Water Utility Monitoring System Market

Investment prioritization — With an expected enlargement of total addressable market over the forecast period, capital allocation decisions made in 2026 will determine multi-year returns. Our report translates market-scale projections into scenario-based investment ladders that help boards and CFOs evaluate replacement cycles, retrofit versus greenfield rollouts, and partner selection under constrained budgets.

Water Utility Monitoring System Market

Operational transformation — Smart monitoring is not just about meters and sensors; it redefines workforce models, service contracts, and customer engagement. The report provides practical frameworks to quantify labor and maintenance savings versus the incremental costs of cybersecurity and continuous monitoring.

Competitive positioning — For vendors and integrators, 2026 will reward scalable platforms, flexible commercial models, and embedded analytics. The report dissects recent strategic moves by leading vendors to highlight replicable go-to-market plays and partnership architectures.

Decision playbooks — Step-by-step procurement and implementation playbooks for utilities of varied sizes, including stakeholder maps, procurement clause templates, and phased deployment roadmaps to de-risk rollout.

Total cost of ownership (TCO) models — Configurable TCO templates that translate capital and recurring cost drivers into multi-year cashflow models. These templates explicitly model trade-offs such as manual reading labor savings versus recurring cybersecurity and monitoring services.

Risk and compliance matrix — A prioritized risk register aligned with EPA, CISA and regional telecom regulations for IoT spectrum and data privacy. The matrix includes mitigation options graded by cost, time-to-implement, and residual risk to support Board-level risk appetite decisions.

Procurement & contracting guardrails — Standardized KPIs, SLA structures, performance-based contracting clauses, and metrics for non-revenue water reduction, latency, maintenance windows, and cybersecurity incident response.

Implementation toolkits — Templates for network design (edge/cloud balance), sensor placement heuristics, data ingestion schemas, and interoperability checklists that accelerate vendor-neutral system integration.

Scenario and sensitivity analyses — Demand-driven scenarios (conservative, baseline, accelerated) that map to capex/opex profiles and show how variations in adoption rate materially shift ROI timelines and market sizing through 2032.

Executive dashboards and KPIs — Ready-to-use indicator sets and dashboard prototypes for real-time program governance, designed to align operational teams and elected leaders on measurable outcomes.

The competitive field remains concentrated around several established instrumentation, metering, automation, and analytics providers, but it is dynamically evolving through product launches, partnerships, and acquisitions. The three- to five-firm concentration metrics indicate a market where established vendors maintain strong footholds, yet meaningful share is available to innovators and regional specialists.

Badger Meter, Inc. (Milwaukee, Wisconsin) — Expanding sensing breadth through acquisitions and targeted coverage of sewer and manhole monitoring, signaling a play to bundle potable and wastewater monitoring into a single vendor-managed offering.

Itron, Inc. (Liberty Lake, Washington) — Continuing to scale AMI and communications capabilities through product and geographic expansion; recent projects emphasize high-frequency interval data for enhanced leak detection and non-revenue-water reduction.

Sensus (Xylem Inc.) and Xylem Inc. — Leveraging scale to integrate metering hardware with network optimization and digital twin capabilities, offering utilities a systems-level value proposition.

Neptune Technology Group, Kamstrup, Diehl Metering, Aclara, Landis+Gyr — Each plays to strengths in meter technology, communication modules, or regional channel presence; their strategies emphasize interoperability and lifecycle service arrangements.

ABB, Siemens, Schneider Electric — Industrial automation leaders are moving deeper into the water utility stack with SCADA modernization, cybersecurity-hardened solutions, and AI-enabled predictive control modules.

Hach (Danaher) and Mueller Water Products — Specialist suppliers continue to anchor water quality monitoring and infrastructure products that complement metering networks.

Recent moves underscore the competitive dynamics: acquisitions that broaden sensing portfolios, targeted project launches that demonstrate scaled AMI capabilities in emerging markets, and new product introductions that emphasize cybersecurity and AI-driven predictive insights. These developments are illustrative of two converging dynamics — horizontal breadth (bundling across potable, wastewater, and analytics) and vertical depth (advanced cybersecurity, digital twin, and predictive operations).

Cybersecurity as critical infrastructure — Guidance from national agencies treating water control systems as critical assets imposes explicit requirements for network segmentation, encryption, and continuous monitoring. These mandates elevate baseline costs and create a procurement premium for vendors with demonstrated compliance and incident response capabilities.

Infrastructure investment imperative — The industry faces multi-decade capital needs to replace aging assets and close service gaps. While the scale of required investment creates demand pull for monitoring solutions, it also necessitates staged financing and blended funding approaches that the report maps for municipal decision-makers.

Labor and operating model shifts — Smart deployments materially reduce manual meter-reading labor, but they reallocate cost into cybersecurity, data operations, and service contracts. Our operational models quantify these shifts and provide workforce transition plans to preserve institutional knowledge while enabling digital roles.

Local telecom and IoT policy — Spectrum and data privacy rules in jurisdictions such as parts of Southeast Asia influence technology selection (e.g., LPWAN choices) and vendor qualification criteria; PW Consulting’s regional risk notes flag the most consequential constraints for 2026 procurement cycles.

Board briefings — Use the Executive Risk Matrix and one-page scenarios to align capital allocation to risk appetite and service objectives before soliciting vendor proposals.

RFP preparation — Adopt the procurement guardrails and SLA templates to reduce negotiation friction and standardize evaluation of cybersecurity, data ownership, and upgrade pathways.

Vendor selection — Apply the vendor capability grid and integration checklists to shortlist partners that match your technical architecture and commercial preferences.

Pilot-to-scale pathway — Implement the phased deployment roadmap to convert pilots into city- or utility-wide programs while controlling scope, budget, and change management.

Consistent with our “trailer” approach to this announcement, the article purposefully avoids publishing granular segment and regional share tables, pricing benchmarks, and confidential vendor scorecards. These deliverables are part of the full PW Consulting report and supporting client workstreams because they contain proprietary, time-sensitive competitive intelligence and contractual templates that require controlled distribution. The high-level growth metrics, risk frameworks, and playbooks presented here are sufficient for early strategic alignment; the detailed, executable artifacts are available through the report portal for subscribers and clients.

Decision-makers in 2026 will be judged by their ability to convert strategic intent into executable programs that balance modernization speed, cybersecurity, and fiscal stewardship. PW Consulting’s Water Utility Monitoring System Market report provides the market trajectory, scenario analyses, procurement and implementation tools, and vendor insights necessary to make those trade-offs with confidence. With projected market expansion and continued vendor dynamism, the coming planning cycle is both an opportunity and a test: the utilities and suppliers that align governance, procurement, and operational change will capture the productivity and resilience gains inherent in smart monitoring at scale.

To access the full set of proprietary appendices — including vendor benchmarking matrices, configurable TCO models, RFP templates, and region-specific regulatory shortlists — please consult the PW Consulting report distribution channels.

For detailed analysis of this topic, please visit the official page:Water Utility Monitoring System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com