Home Fragrances Market Insights

Other |

2026-05-25 07:25:02

As enterprises accelerate deployment of high‑performance computing and hyperscale infrastructure, liquid cooling has moved from pilot projects to procurement tables. PW Consulting’s HFO Cooling Fluids For Data Center Market report—based on a 2025 base year and a 2026–2032 forecast horizon—translates this technical shift into actionable intelligence for 2026 decision cycles. The market we model grew from a modest base in 2020 to an inflection point by 2025, and our top‑line projection shows sustained expansion through 2032 (compound annual growth rate of 18.02% across the forecast period). All monetary figures in this preview are expressed in USD Million; the full dataset and interactive models are available in the report.

Hfo Cooling Fluids For Data Center Market

Between 2020 and 2025 the market for HFO-based cooling fluids moved from early adoption to commercial scale—our modeled trajectory reflects that maturation. In 2020 the market measured in the low hundreds of USD Million; by the report base year (2025) it exceeded the mid‑hundreds, with the forecast showing a rapid escalation into the high end of the projection window by 2032. This expansion is being driven by three converging forces: regulatory pressure to lower direct greenhouse gas emissions, the operational economics of higher rack‑level power densities, and an expanding vendor ecosystem delivering application‑specific chemistries for immersion and refrigerant‑based chiller solutions.

Hfo Cooling Fluids For Data Center Market

For 2026 planning, that trajectory implies two immediate implications for enterprise stakeholders: first, procurement and design specifications written in 2026 will have to anticipate a faster shift to ultra‑low GWP chemistries; second, supplier selection should account for not just current performance but near‑term scale‑up, regulatory compliance pathways, and raw‑material exposure. Our report converts these macro signals into procurement scorecards, compatibility matrices, and cost‑build scenarios tailored for CAPEX and OPEX tradeoffs.

Hfo Cooling Fluids For Data Center Market

These deliverables are designed for CFOs setting 2026 budgets, CTOs piloting immersion on critical workloads, and procurement leads negotiating multi‑year supply agreements.

The HFO cooling fluids market is concentrated. The top three suppliers account for a material majority of available commercial capacity, and the top five approach near‑total market control—indicative metrics that buyers must factor into negotiation and contingency planning (CR3 ~72.45%; CR5 ~88.3%). Within that structure, a small set of specialty chemical suppliers and refrigerant incumbents have pivoted to data‑center focused products and strategic partnerships with system integrators and hyperscalers.

Understanding each supplier’s manufacturing strategy, product qualification pipeline, and commercial posture is central. The full report maps these variables into a supplier choice matrix that buyers can use to prioritize suppliers by risk tolerance and time‑to‑deploy targets.

Policy changes are accelerating the shift to ultra‑low GWP solutions. Notable regulatory milestones include U.S. EPA rules introducing GWP ceilings for certain equipment classes starting in 2027, continued implementation of the Kigali Amendment and national HFC quota systems, and evolving EU F‑Gas guidance favoring ultra‑low GWP fluids. These frameworks create a window in which selection of higher‑GWP refrigerants increases retrofit and compliance risk.

On the supply side, HFO manufacturing depends on a narrow band of fluorinated intermediates and olefin feedstocks. Price volatility in these inputs has already led to supplier pass‑throughs and discrete product price actions—events that materially affect project economics for large scale rollouts. The report provides models for hedging, price indexation clauses, and alternative sourcing strategies to mitigate this exposure.

We designed this report to be a decision‑ready resource for 2026. It blends a high‑resolution market model—anchored to a 2025 base year and projecting through 2032—with primary vendor due‑diligence, manufacturing risk maps, and procurement templates. Rather than a purely descriptive market brief, the report contains executable templates and an interactive scenario engine that enables teams to stress‑test vendor commitments, cost assumptions, and regulatory outcomes.

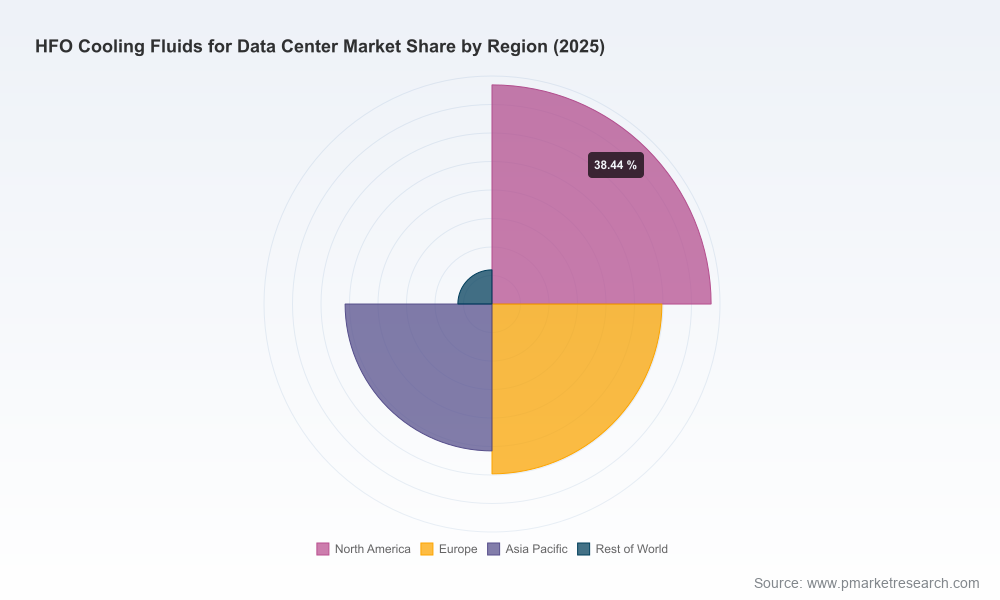

Importantly, this article intentionally highlights the strategic insights and operational outputs without disclosing the granular regional and application revenue splits that underpin our models. Those segment‑level allocations, along with supplier‑level revenue breakdowns and downloadable Excel models, are contained in the full PW Consulting report and are the key assets procurement and engineering teams use to finalize 2026 budgets.

For teams preparing capital approvals and vendor selections in 2026, PW Consulting’s HFO Cooling Fluids For Data Center Market report provides the analytic foundation, test protocols, and commercial playbooks required to move from intent to deployment. To access the full dataset, vendor scorecards, and the downloadable scenario model, please consult the official report page for subscription and licensing options.

For detailed analysis of this topic, please visit the official page:Hfo Cooling Fluids For Data Center Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com