Adult EEG Cap Market Growth Analysis: Innovations and Key Drivers to Watch

Health |

2026-05-25 14:36:02

PW Consulting’s latest Automotive DSP Amplifier Market report (base year 2025, forecast period 2026–2032) arrives at a critical inflection for both OEMs and suppliers. The global market reached approximately USD 2.98 billion in 2025 and — driven by broader electrification, smart-cockpit feature adoption, and aftermarket premiumization — is modelled to expand at a compound annual growth rate (CAGR) of 8.75% to reach roughly USD 5.36 billion by 2032. Market concentration is meaningful but not locked-in: the leading three companies account for a substantial portion of revenue while the top five capture a clear majority, underscoring both incumbent advantage and room for disruption.

Automotive Dsp Amplifier Market

Time-sensitive platform choices: 2026 is the year many vehicle programs move from prototype integration to production sourcing for high-performance audio subsystems. Decisions about DSP architecture (on-chip vs. discrete), Class-D amplifier topologies, and digital input strategies will determine multi-year BOM cost and feature trajectories.

Automotive Dsp Amplifier Market

Software is now a product differentiator: Competitive advantage is shifting from raw wattage to sophisticated signal processing — room correction, object-based audio, immersive audio staging, and adaptive ANC. Suppliers who pair best-in-class DSP silicon with robust tuning ecosystems will capture up-sell and content-partnership opportunities.

Automotive Dsp Amplifier Market

Supply-chain and regulatory constraints compress options: AEC-Q100 qualification, functional safety expectations, semiconductor lead-time volatility, and pressure on rare-earth components are reshaping sourcing and inventory strategies in ways that must be resolved before supplier contracts are finalized in 2026.

Aftermarket and OEM channels diverge: Premium aftermarket players and boutique brands continue to command brand-driven margins, while integrated solutions and semiconductors target scale with OEMs. Strategies for channel-specific product roadmaps must be decided now to capture the accelerating premiumization of cabin audio.

Our deliverables are designed to convert insight into prioritized action. The report combines a validated quantitative market model with a suite of operational playbooks and tools targeted at procurement, product, and corporate development teams:

Dynamic market model (2020–2032) with scenario toggles — baseline, accelerated EV/infotainment adoption, and constrained-supply scenarios — enabling rapid sensitivity testing for program-level revenue exposure.

Technology roadmaps and feature-matrix templates mapping DSP capabilities (e.g., sample-rate headroom, processing cores, algorithm support) against price bands and integration complexity.

Supplier risk heatmaps — AEC-Q100 / functional safety readiness, supply-chain fragility scores, and mitigations prioritized by impact to lead-time and cost.

Go-to-market playbooks for OEM and aftermarket launches — channel positioning, sample/test lab protocols, acoustic tuning service models, and bundling strategies for infotainment ecosystems.

Commercial negotiation levers and modeled TCO/ROI calculators for silicon vs. module buy decisions, licensing vs. in-house DSP development, and long-term BOM scenarios.

M&A and partnership screening criteria — a pragmatic filter for identifying targets that fill capability gaps (software stacks, calibration platforms, certification breadth) or provide geographic/ channel entry.

Regulatory & qualification checklist tailored to automotive audio subsystems — an executable roadmap to reduce certification risk and shorten time-to-production.

The market is shaped by two overlapping competitive sets: specialist audio brands that dominate the premium aftermarket and boutique OEM segments, and semiconductor and Tier-1 suppliers that enable mass-market integration. Our assessment synthesizes company-level strategy, product capability, and go-to-market posture.

Audiotec Fischer (Germany) — A leader in premium aftermarket performance, its HELIX and BRAX lines combine high-end DSP features with award-winning hardware and calibration tools. Recognition such as recent industry awards underscores their brand equity in experience-led audio tuning, an asset when OEMs seek perceived luxury differentiation.

Audison (Italy) — Focused on high-power D-Class implementations and OEM-integration-ready modules, Audison’s Forza series exemplifies how boutique players are extending into white-label and OEM partnerships to harvest higher-volume opportunities without diluting premium positioning.

Alpine Electronics (Japan) — Alpine’s Status line and Hi-Res DSP platforms are positioned to bridge aftermarket fidelity and OEM integration. Their engineering depth in vehicle acoustic calibration and infotainment integration makes them a natural partner for automakers seeking turnkey premium audio packages.

AudioControl (USA) — Strong in OEM signal-processing and module design, AudioControl’s focus on integration presents a playbook for scaling from niche acoustics to program-level supply.

Mosconi and ARC Audio — These boutique manufacturers provide compact, high-performance DSP amplifiers and processors tailored to audiophile aftermarket demand, highlighting a persistent premium segment that rewards engineering-led differentiation.

STMicroelectronics, Texas Instruments, Analog Devices, NXP — These semiconductor players are strategic enablers. Their automotive-grade Class-D amplifiers, DSP cores, and integrated audio SoCs underpin OEM strategies for integrated, software-updatable audio platforms. Recent product launches and processor announcements reflect an arms race in processing headroom and functional-safety-ready silicon.

Collectively, this competitive set yields a market structure where the top three firms capture a significant share while the top five control a clear majority — creating an environment that rewards scale and differentiated IP, but still allows well-executed entrants to carve sustainable niches.

Recognition matters: Award-winning products and software (e.g., high-profile DSP hardware and tuning tools) accelerate brand adoption with premium OEM programs and the aftermarket community.

Silicon cadence: New high-frequency Class-D amplifiers and advanced DSP cores launched in 2025 increase integration options for automakers but also raise validation and software workload.

Supply risk: Persistent semiconductor lead-time volatility and rare-earth constraints are real and measurable — they necessitate inventory hedging, alternate bill-of-materials planning, and strategic supplier partnerships.

Regulatory rigor: AEC-Q100 compliance and automotive functional-safety expectations are non-negotiable. Firms that build certification roadmaps early will shorten new-program timelines and reduce rework costs.

OEMs: Treat audio subsystems as modular software-enabled platforms. Shortlist silicon vendors based on both hardware metrics and tooling support. Negotiate dual-sourcing where feasible and embed certification milestones into supplier contracts.

Tier suppliers and module integrators: Invest in calibration-as-a-service and remote tuning capabilities to create recurring revenue streams. Lock in long-lead components and qualify alternate magnet/rare-earth substitutes to reduce single-supplier exposure.

Semiconductor vendors: Offer reference designs and validated stacks (including safety documentation) to accelerate OEM adoption. Emphasize software ecosystems that enable feature differentiation.

Aftermarket brands: Double down on experiential marketing (in-vehicle demos, acoustics labs) and premium content partnerships. Consider OEM-tier partnerships for co-branded premium packages.

Private equity & strategic investors: Prioritize targets with defensible calibration tooling, IP in algorithmic processing (room correction, object-based audio), and demonstrable pathway to OEM certifications — these traits materially increase exit multiples.

Our report is more than a market forecast; it is a decisioning toolkit built for teams that must execute in 2026. We combine market sizing with executable templates — procurement playbooks, supplier risk matrices, product-roadmap alignment grids, and M&A screening filters — so that leaders can move from insight to contract, product spec, or acquisition target within weeks, not months.

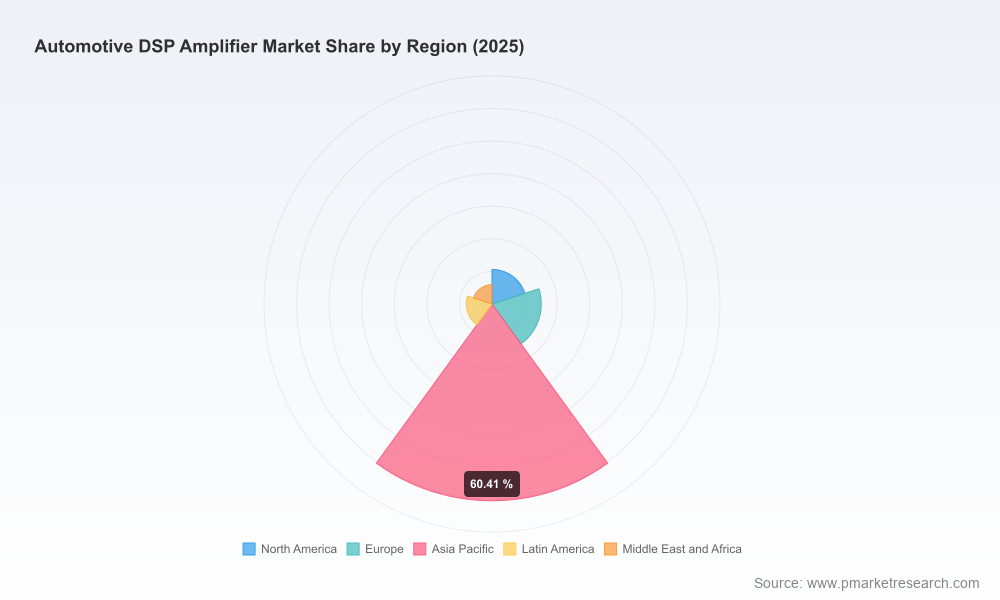

To respect commercial confidentiality and maintain the “trailer” principle of this release, we have intentionally withheld granular regional and application-level breakdowns from this summary. The report itself contains those detailed splits, interactive models, and granular supplier scorecards that are essential for program-level negotiation and investment underwriting.

If your 2026 plans involve platform choices, supplier contracts, or M&A related to automotive audio, PW Consulting can provide an in-depth briefing and an interactive model tailored to your specific exposure.

Contact our Automotive Electronics team to schedule a workshop: we will run scenario planning against your vehicle programs, map supplier qualification gaps, and produce a prioritized, time-bound action plan to de-risk 2026 milestones.

In a market moving as quickly as automotive DSP amplifiers — with evolving silicon, software, and supply dynamics — the decisions you make this year determine your competitive position for the rest of the decade. PW Consulting’s Automotive DSP Amplifier Market report equips leaders with the frameworks, models, and tactical playbooks to turn uncertainty into opportunity.

For detailed analysis of this topic, please visit the official page:Automotive Dsp Amplifier Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com