Aircraft Carpets Market Emerging Opportunities by 2034

Networking |

2026-05-29 14:51:18

PW Consulting today releases a strategic preview of its forthcoming Bottle Valve Market report (base year 2025; forecast period 2026–2032), designed as an executive-level briefing to inform boardroom decisions entering 2026. Built on a multi-year historical base (2020–2025) and forward-looking market modeling, the study shows the global bottle valve market progressing from approximately USD 812.45 million in 2020 to USD 1,275.6 million in 2025, and heading toward a projected USD 2,216.06 million by 2032—implying a compound annual growth rate (CAGR) of 8.2% over the forecast horizon. This preview explains why that growth matters, what strategic choices it creates, and how senior executives can use our full report to convert insight into actionable moves.

Bottle Valve Market

A maturing but still-evolving market: An 8.2% CAGR signals sustained demand and profitable expansion opportunities — not a short-term spike. For corporations, this means 2026 is a pivotal year to move from exploratory pilots to scalable investments in product platforms, manufacturing capacity, and supply chain reconfiguration.

Bottle Valve Market

Moderate concentration, high opportunity for differentiation: Market concentration metrics point to a competitive landscape where the top three firms do not dominate decisively (CR3 ~38.5%), and the top five control just over half of share (CR5 ~52.7%). This structure favors both disciplined incumbents and well-funded entrants that can establish niche technical advantages or secure channel partnerships.

Bottle Valve Market

Regulatory and tariff forces changing economics: New regulatory moves — including the U.S. EPA’s tighter VOC standards for aerosol coatings (Jan 2025) and ongoing EU aerosol dispenser requirements — are reshaping formulation choices and product specs. In parallel, filled aerosol packages remain subject to tariff considerations in key markets. These non-market costs must be embedded in 2026 product roadmaps and pricing strategies.

Proprietary market-size and growth models calibrated to 2020–2025 historicals and stress-tested across multiple 2026–2032 scenarios, enabling executives to translate top-line growth forecasts into capacity, working capital, and pricing plans.

Competitive benchmarking and capability matrices for the industry’s leading manufacturers and technology specialists, including product portfolios, manufacturing footprints, R&D focus, and go-to-market channels — enabling targeted countermeasures or partnership strategies.

Regulatory-impact playbooks that convert legislative changes into concrete product changes, timeline implications, and cost-to-compliance estimates so R&D and regulatory affairs teams can prioritize workstreams in 2026.

Supply-chain risk assessments and mitigation templates: supplier concentration assessments, raw-material cost-sensitivity models, nearshoring and dual-sourcing trade-offs, and tariff mitigation options for filled packages.

An M&A and alliance checklist, including valuation frameworks and integration risk profiles tailored to the bottle valve space — designed for corporate development teams evaluating bolt-ons or strategic joint ventures.

Board-ready slide sets and an interactive dashboard for custom scenario runs — so C-suite leaders can stress test budgets and present investment cases with defensible assumptions.

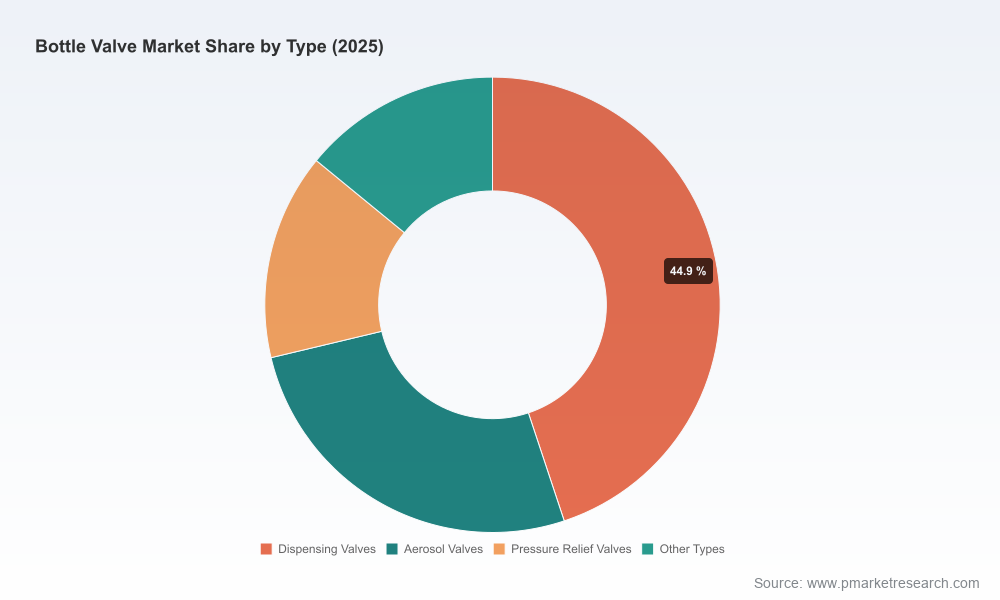

The market is characterized by a mix of long-established specialists and global packaging systems providers. Key players profiled in the report include:

Precision Valve Corporation (Greenville, SC, USA) — a near-century-profiled leader in aerosol valves and actuators with deep capabilities across tilt, 360-degree, metered and Bag-on-Valve platforms. Recent leadership change (new CEO appointed April 2025) and a product innovation award in 2026 for the SMART 35 aerosol valve underscore a renewed focus on advanced dispensing technologies and commercial execution.

Control Devices / Sherwood Valve (Pittsburgh, PA, USA) — following Control Devices’ acquisition of Sherwood Valve (announced January 2026), the combined entity strengthens its flow-control and compressed-gas valve portfolio, with implications for industrial gas and specialty cylinder markets.

AptarGroup Inc. (Crystal Lake, IL, USA) — a major global provider of dispensing solutions with strategic emphasis on pharmaceutical and beauty segments where regulatory compliance and precision metering are critical.

Lindal Group (Germany), Coster (Italy), Mitani (Japan) — regional and technology specialists that continue to advance aerosol and dispensing innovation, including Bag-on-Valve and precision metering systems.

Cavagna Group, Rotarex, and GCE — players more focused on cylinder and gas-control valves, important where bottled-gas safety, regulator integration, and high-pressure standards drive procurement decisions.

Together, these firms illustrate two strategic axes in the market: product-technology leadership (precision, metering, bag-on-valve) and scale/channel strength (global filling infrastructure, gas distribution networks). The 2026 competitive battleground will be contested on both axes.

Higher unit costs for advanced formats: Bag-on-Valve systems continue to command materially higher per-unit valve costs compared with traditional valve formats — a factor that must be reconciled against their marketing and formulation benefits. Our modeling shows unit-cost delta is an order-of-magnitude higher for Bag-on-Valve designs, which shifts go-to-market economics in premium personal care and pharmaceutical dosing applications.

Compliance-driven reformulation costs: tighter VOC rules and aerosol dispenser safety directives increase unit and compliance costs, compressing margins for commoditized product lines while increasing the value of differentiated, low-emission dispensing platforms.

Tariff and materials volatility: filled-package tariff considerations and raw-material supply disruptions need to be part of 2026 procurement strategy — particularly for companies relying on cross-border steel, aluminum, or specialty polymers.

Phase investments into scalable, differentiated platforms: Prioritize R&D and capital allocation toward valve technologies that deliver demonstrable performance or compliance advantages (e.g., precision metering for pharmaceuticals, low-reactivity aerosol solutions). Use staged funding tied to technical milestones to reduce exposure.

Embed regulatory scenarios into product-cost models: Run regulatory “what-ifs” for likely VOC and safety outcomes. Price, reformulate, or repackage proactively rather than reactively to avoid margin erosion and time-to-market penalties.

Reassess sourcing strategy with a total-cost lens: Given the unit-cost premium for advanced formats and tariff exposures on filled packages, deploy a mix of nearshoring, dual sourcing, and long-term supplier agreements to stabilize margins and reduce lead-time risk.

Use targeted M&A and partnerships to close capability gaps: With CR3/CR5 indicating moderate concentration, strategic acquisitions (or minority investments) can accelerate entry into high-value niches or secure critical supply. The Control Devices–Sherwood transaction is a recent example of how inorganic moves can reconfigure competitive positions quickly.

Operationalize commercialization playbooks for premium channels: Convert product innovation into revenue by aligning regulatory approvals, clinical or consumer testing, and premium channel distribution — especially for pharmaceutical and high-end personal care applications where certification and precision matter.

Patent filings and design awards (e.g., the SMART 35 recognition) as early indicators of competitive differentiation.

M&A activity and minority investments that close capability gaps or consolidate distribution networks.

Regulatory bulletins and tariff rulings that shift product feasibility or unit economics.

Raw-material and component-price trends that affect the delta between traditional and advanced valve formats.

This report is structured as an implementation toolkit: not only a market sizing and forecast, but a suite of operational templates, valuation frameworks, and regulatory playbooks that a C-suite can use to make defensible resource-allocation calls in 2026. For clients who require bespoke assistance, PW Consulting offers scenario workshops, integration planning for potential acquisitions, and tailored cost-to-serve modeling aligned to the bottle valve value chain.

This release is a strategic preview designed to surface the decisive issues executives must confront in 2026. The full report provides the granular segmentation, model inputs, and downloadable dashboards that corporate and investor decision-makers require to act with confidence. Visit our report landing page to obtain the comprehensive dataset, segment-level analysis, and advisory engagement options that will convert 2026 opportunity into measurable value.

PW Consulting — We translate market signal into strategic advantage.

For detailed analysis of this topic, please visit the official page:Bottle Valve Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com