What Is Driving Growth in Statin Market Amid Rising Cardiovascular Disease Cases?

Networking |

2026-05-11 10:58:15

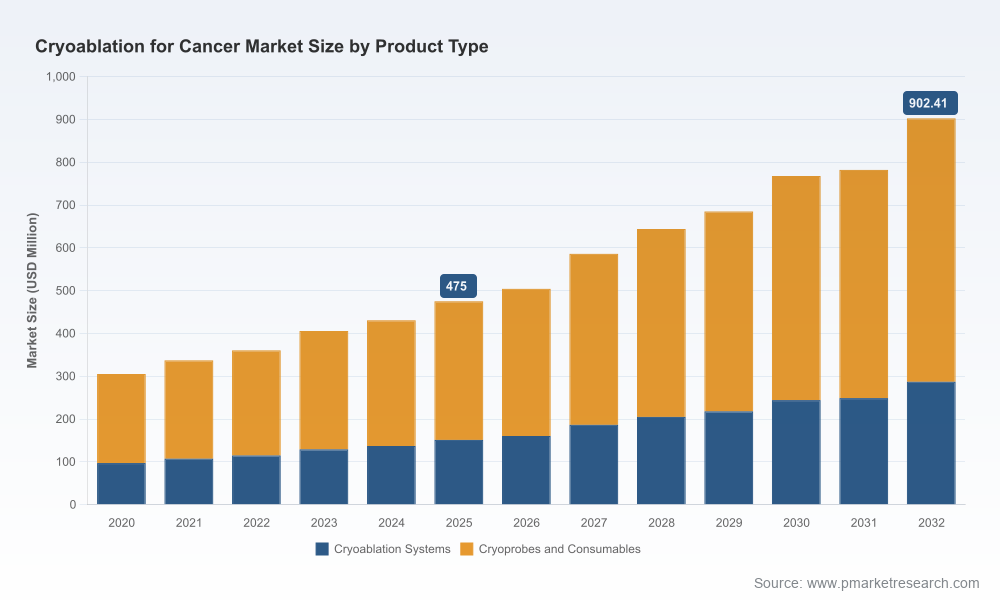

PW Consulting’s new Cryoablation For Cancer Market report equips executive teams with the market intelligence required to shape investment, clinical and commercialization strategies in 2026. The global market has demonstrated steady expansion over the last half decade and, according to our base-case model, is expected to continue on a high-growth trajectory — rising from a 2025 market size of approximately USD 475 million to just over USD 900 million by 2032, representing a compound annual growth rate of about 9.42% across the 2026–2032 forecast window. Market concentration is notable: the three largest suppliers control the majority of demand and the five largest players account for well over four-fifths of the market, underscoring both competitive intensity and potential consolidation dynamics.

Cryoablation For Cancer Market

Clinical adoption is at an inflection point. Regulatory milestones and guideline updates in 2025–2026 have begun to reframe cryoablation from a niche modality toward a mainstream option for clearly defined patient cohorts. These changes create immediate commercial opportunities — and reputation risks — for companies that either lead evidence generation or are slow to adapt.

Cryoablation For Cancer Market

Payer and reimbursement pathways are evolving. Recent coding and coverage movements signal that procedural reimbursement and device reimbursement pathways exist for select applications; however, realization of durable commercial returns will depend on granular payer engagement, outcomes-driven contracting and care-path integration.

Cryoablation For Cancer Market

Capital intensity and procurement realities matter. Adoption decisions hinge on hospital and ambulatory surgical center capital planning and the ability of suppliers to support acquisition financing, disposable economics and maintenance services. Equipment buyers are increasingly comparing total cost of ownership across device platforms and consumable models.

Competitive positioning will be decided by three levers: clinical evidence, integrated service offerings (capital + disposables + clinical support), and channel economics. Firms that combine best-in-class clinical data with pragmatic commercialization playbooks will capture disproportionate share.

Regulatory and guideline developments in early 2026 have validated the clinical pathway for cryoablation in selected low‑risk early‑stage indications, accelerating interest from both clinicians and payers. These changes create a narrow window for first-mover advantage in evidence-based label expansion and real-world outcomes programs.

Device coding and reimbursement clarifications for interventional oncology consumables and procedure components reduce execution risk for commercial launches — but do not eliminate the need for active payer negotiation and real-world cost-effectiveness demonstration.

Healthcare provider capital pressures remain elevated. Hospitals are balancing deferred asset replacement against rising depreciation and service demand, which is reshaping procurement timelines and favoring flexible acquisition and as‑a‑service models.

The market is led by a compact set of global incumbents and specialist innovators. Each cluster of players brings a distinct strategic playbook:

Large medtech integrators (e.g., Medtronic) — leverage installed base, cross‑selling channels and global regulatory reach to bundle cryotherapy into broader oncology and surgical portfolios. Their competitive edge is scale of clinical support and distribution, but they must prove differentiated clinical outcomes versus niche players to avoid commoditization.

Interventional platform leaders (e.g., Boston Scientific & Galil Medical) — focus on catheter and probe innovation, image‑guided systems and multi‑needle capability, positioning cryoablation as an interventional oncology tool that complements ablation modalities. Strong coding and reimbursement know‑how for probes and consumables supports their commercial model.

Focused innovators (e.g., IceCure Medical) — pursue fast, indication‑specific regulatory strategies and pragmatic evidence-generation programs. Recent regulatory approvals and approved post‑marketing study designs have materially altered the competitive calculus in specific breast‑conserving treatment pathways. Such players can disrupt care pathways rapidly in narrowly defined populations.

Specialist and regional suppliers (e.g., CooperSurgical, Erbe, Metrum Cryoflex and others) — serve niche clinical segments, OEM partnerships and regional channels. Their agility in pricing and service models makes them preferred partners for certain health systems and smaller clinics.

Service providers and distributors (e.g., HealthTronics, BVM Medical) — compete on deployment, training and procedure volume growth, often enabling adoption in markets where capital constraints would otherwise be a barrier.

Collectively, these dynamics produce a market where the top three firms control a significant share of commercial demand and the top five establish a de facto standard of care in many geographies. For new entrants and adjacent incumbents, the path to scale will require either significant clinical differentiation or a transaction strategy that fills gaps in probes/consumables, clinical evidence or distribution reach.

We designed this report to be immediately actionable for commercial, clinical and corporate development teams. Key deliverables include:

Proprietary market-sizing and forecasting model with scenario variants (conservative, base, aggressive) and sensitivity levers you can manipulate to test pricing, reimbursement and adoption assumptions.

Executive go‑to‑market playbooks for hospital, ASC and outpatient oncology channels, including procurement decision maps and capital procurement negotiation templates.

Reimbursement and payer engagement toolkit: coding pathways, dossier outlines, and outcomes measures that payers are demanding across early‑adopter indications.

Clinical evidence heatmap and trial prioritization matrix that ranks indications by expected clinical impact, time‑to‑value and cost to generate pivotal evidence.

Competitive benchmarking dashboard that maps product capabilities, clinical claims, service offerings and distribution intensity — designed to support M&A screening and partner selection.

Commercial scenarios and revenue models that isolate recurring consumable economics from capital revenue, helping commercial teams build sustainable margin plans.

Regulatory pathway maps and recommended study designs for label expansion and post‑market evidence collection in primary oncology use cases.

Prioritize focused evidence generation: Invest in tightly defined, pragmatic trials that align with payer endpoints and guideline committees. Early, high‑quality real‑world evidence will unlock uptake faster than broad randomized programs in many settings.

Design modular commercial offers: Combine flexible capital acquisition options with consumable bundles and procedural training. Buyers are looking for predictable per‑procedure economics and low operational friction.

Engage payers early and often: Map reimbursement pathways for each jurisdiction and secure coverage pilots tied to outcomes metrics. Coding clarity in interventional oncology and procedural reimbursement are necessary but insufficient — outcomes and cost offsets sell contracts.

Scan for bolt‑on M&A and partnerships: For firms needing rapid capability build, prioritize targets that close gaps in probe technology, disposables volume, or regional distribution rather than large transformational deals.

Embed clinical champions into commercialization: Commercial launches must be clinician‑led. Invest in key opinion leader networks, procedural proctorship and a small set of real-world registries to sustain adoption momentum.

Our analysis highlights opportunity vectors, but execution risk is material. Key uncertainties include the pace of guideline adoption across specialties, local payer coverage variability, and competing ablation technologies. Importantly, this briefing is a high‑level orientation: the full report contains the granular segmentation, regional demand models, and company‑level revenue estimates that many clients require to finalize budgets, M&A bids and strategic partnerships. In keeping with our “trailer” principle, we have deliberately withheld itemized regional and application split numbers here to prioritize a clear strategic narrative; the complete dataset and interactive models are included in the full report package.

Executives preparing 2026 budgets should use the report to stress‑test investment priorities across R&D sequencing, clinical evidence spend and commercial rollout. Corporate development teams can accelerate target screening using our acquisition fit matrix, while commercial leaders can begin rapid prototyping of bundled offers aligned to payer value metrics.

The complete Cryoablation For Cancer Market report from PW Consulting includes the full market model, downloadable scenario worksheets, competitive scorecards, reimbursement playbooks and a prioritized evidence‑generation roadmap. For teams seeking tailored support, PW Consulting offers advisory sprints to align the report’s insights with your organization’s balance sheet, clinical assets and commercial capabilities. Visit our report page to request the full dataset, a sample of the interactive dashboards, or to schedule a briefing with one of our senior strategists.

For detailed analysis of this topic, please visit the official page:Cryoablation For Cancer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com