Oil Spill Absorbent Solutions for Offshore and Onshore Sites

Other |

2026-02-13 05:50:40

As laboratory digitization, tighter clinical quality standards, and product-differentiating optical innovations reshape the landscape for desktop refractometers, executives face a discrete window in 2026 to convert technical capability into sustainable commercial advantage. PW Consulting’s forthcoming Desktop Refractometers Market report synthesizes multi-year market dynamics, competitive positioning, and actionable go-to-market frameworks to inform board-level and business-unit decisions for the 2026–2032 planning horizon.

Desktop Refractometers Market

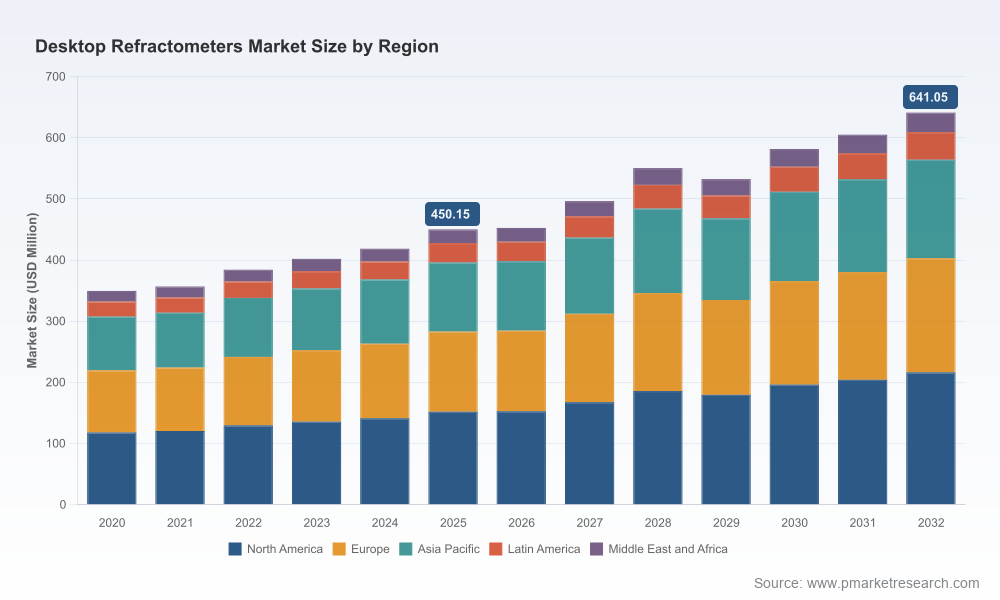

Desktop refractometers sit at the intersection of clinical diagnostics, food & beverage quality control, and chemical research. After a consistent recovery in the early 2020s, the market reached an estimated USD 450.15 Million in 2025. Our forecast model, built from device-level shipment trends, pricing trajectories, and service/consumables demand curves, shows a steady expansion at a compound annual growth rate (CAGR) of 5.18% across the 2026–2032 period, delivering clear room for market share reallocation and profitable portfolio upgrades.

Desktop Refractometers Market

Two structural features make this space strategically compelling for 2026:

Desktop Refractometers Market

The report is intentionally operational in scope — it is built to serve strategic planners, corporate development teams, and business unit leaders preparing 2026 budgets and strategic roadmaps. Key deliverables include:

Importantly, the report preserves commercial confidentiality where it matters most: while we provide a granular segmentation framework by geography, device architecture, and application, the publication deliberately refrains from republishing raw subsegment revenue breakdowns in this press overview. This “teaser” approach helps decision-makers validate strategic hypotheses while encouraging direct engagement with our full dataset for transaction-level planning.

We profile the incumbent ecosystem to reveal how market leaders and fast followers are structuring advantage. The sector’s leading manufacturers — including well-known names from Japan, Europe, and North America — demonstrate a consistent playbook: combine precision optics with domain-specific workflows (e.g., clinical urine/serum measurement or pharmaceutical QC), and leverage certification compliance as a market-access gatekeeper.

Market concentration metrics reflect a landscape where top players maintain substantial revenue share but do not fully saturate demand; this creates openings for targeted specialists and regional champions. PW Consulting’s competitive profiles include product roadmaps, channel economics, and a capability matrix to help acquirers and incumbents evaluate fit for consolidation or alliance strategies.

Two regulatory touchpoints are especially relevant for 2026 commercialization decisions:

Additionally, optical component economics — notably the reliance on medical-grade sapphire prisms — create a cost floor for high-durability clinical models. Sapphire prisms, while expensive relative to other prism materials, provide sterilization compatibility and optical stability; pricing pressure on these inputs can compress margins or justify premium pricing for durable, serviceable units. Our supply-chain modules include a prism-cost sensitivity analysis and recommended sourcing strategies.

We see five pragmatic strategic plays for market participants preparing for the 2026 decision season:

For corporate strategists and product leaders, the report is structured as an executable toolkit rather than an academic exercise. Practical applications include:

True to our “teaser” principle, this press summary outlines directional insights and the strategic playbook you need to start 2026 planning with clarity. The full PW Consulting Desktop Refractometers Market report, however, contains the transaction-grade detail required for execution: full segmentation by geography, device type, and end-use application; unit shipment projections; margin curves by product family; and detailed competitor financial profiles and pipeline intelligence. If your 2026 plan depends on precise subsegment sizing, channel economics, or acquisition target valuations, accessing the full dataset is essential.

Desktop refractometers may be a mature instrument class, but the convergence of digital enhancement, regulatory tightening, and evolving buyer preferences is creating a renewed opportunity set. With a market baseline near USD 450 Million in 2025 and a mid-single-digit growth trajectory through 2032, the period around 2026 will separate companies that preserve margin through capability and service-led models from those that compete solely on price. PW Consulting’s report equips leaders to make those strategic choices with confidence — and the full dataset arms dealmakers with the precision required to act.

To engage with the full analysis, proprietary datasets, and custom scenario modeling for your organization’s 2026 planning cycle, contact PW Consulting to request access to the Desktop Refractometers Market report and our advisory services.

For detailed analysis of this topic, please visit the official page:Desktop Refractometers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com