Press Hardening Machine Market 2026 Strategic Brief — PW Consulting

Executive summary

The press hardening machine market is entering a decisive phase for capital allocation and product strategy. Our newest market research shows the sector expanding at a steady compound annual growth rate (CAGR) of 7.32% across the 2026–2032 forecast window. That pace translates into a structural increase in installed capacity and capital expenditure pressure for automotive OEMs and tier suppliers alike: the industry baseline measured in 2025 sits just above the USD 1.0 billion threshold and is projected to approach the mid–billion range by the end of the forecast horizon.

Press Hardening Machine Market

This press is written as a practical intelligence note for executive teams planning 2026 investments. It highlights where value will be created and captured, what levers materially affect returns, and which strategic options are most resilient under near‑term uncertainties — while intentionally withholding granular segmented figures to encourage direct access to the full report for procurement teams and M&A due diligence.

Press Hardening Machine Market

Why this matters for 2026 decision cycles

- CapEx prioritization: With sustained mid‑single digit growth, 2026 is the year to decide whether to refurbish existing hot‑stamping capacity, invest in energy‑efficient retrofits, or greenfield for EV‑centric components.

- Supplier selection and partnership design: OEMs face trade‑offs between turnkey suppliers who deliver line integration and specialist equipment vendors. Our analysis indicates measurable ROI differences when automation and in‑line monitoring are bundled versus sourced piecemeal.

- Risk management: Raw material cost volatility is not peripheral — steel input costs can dominate production economics. Strategic sourcing, hedging strategies, or engineered material substitutions should be evaluated prior to committing funds.

Market dynamics and the structural drivers

Three structural forces are shaping demand:

Press Hardening Machine Market

- Vehicle lightweighting and safety mandates: Press hardening enables ultra‑high strength steels (UHSS) with tensile strengths up to 2,000 MPa, supporting significant body‑in‑white weight reductions while preserving crash performance. For models where manufacturers choose extensive press‑hardened content, material composition can represent a sizable share of vehicle weight — a core reason adoption persists, especially in premium and mass EV platforms.

- Energy and process efficiency: Advances in servo press technology and furnace design materially change operating economics. Field data and supplier benchmarks show that servo press configurations can reduce drive energy consumption substantially, while multi‑layer furnace architectures reduce thermal losses at scale. These improvements compress payback timelines for new projects but require precision engineering and controls.

- Compliance and process assurance: In‑line thermal monitoring (pyrometers, infrared cameras) and closed‑loop controls are becoming operational prerequisites to meet automotive heat‑treat standards. Traceability and process documentation are now embedded expectations in supply agreements and audit cycles.

Competitive landscape — what to watch

The market exhibits a concentrated supplier structure at the top end: a relatively small number of established equipment providers control a meaningful portion of high‑specification lines, while a broader set of specialized builders address custom or retrofit segments. This concentration affects negotiation leverage, lead times, and the availability of turnkey services.

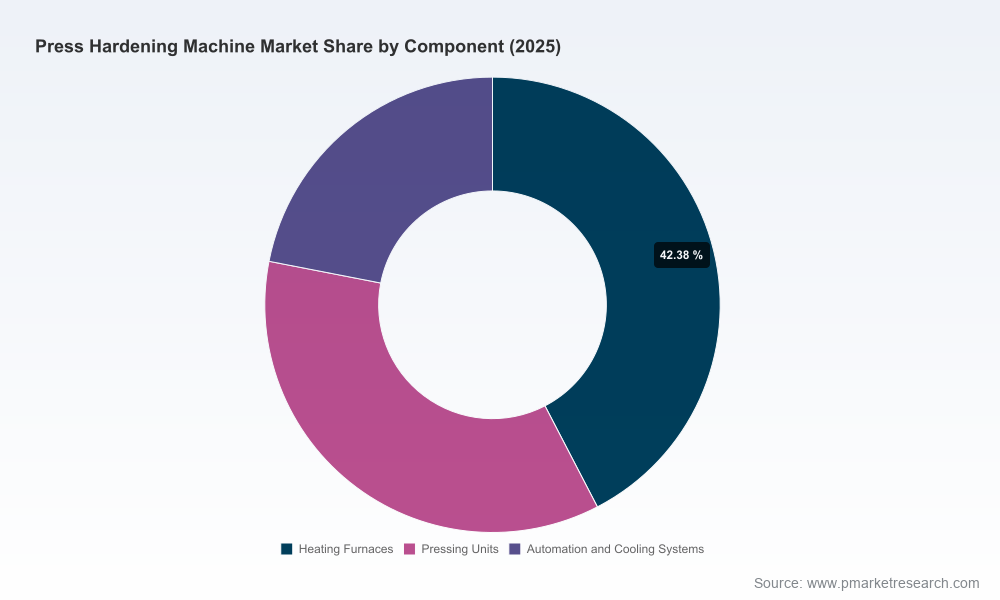

- Tier‑one turnkey integrators: Longstanding companies that deliver complete lines — including servo and hydraulic presses, multi‑layer furnaces, automation and in‑line quality monitoring — dominate large automotive projects. Their offerings increasingly incorporate energy‑savvy architectures and digital monitoring suites that support reliability commitments.

- Specialist manufacturers: Firms focused on bespoke hydraulic or servo press platforms remain critical for non‑standard part families, low‑volume platforms, and retrofit markets. These players often win on lead time, customization, and integration with existing plant automation.

- Recent product activity: Notable vendor initiatives in the last 18 months illustrate the market’s directional shifts — integrated multi‑part line concepts intended for EV components, and trade show activity focusing on heated platen and hot stamping innovations. Such activity signals a technology adoption curve where energy efficiency and multi‑part integration become differentiators.

Practical contents of the full report (operational, not exhaustive)

For procurement directors, plant managers, and corporate strategy teams, our report translates market intelligence into executable tools and templates. Key deliverables include:

- Forward‑looking market sizing by year and scenario (2026–2032) with transparent assumptions, sensitivity analyses, and base/optimistic/pessimistic scenario outputs tied to vehicle production trajectories and UHSS adoption rates.

- Capital investment frameworks and standardized ROI models that capture purchase price, integration cost, energy savings, throughput effects, maintenance profiles, and risk‑adjusted payback timelines.

- Vendor scorecards and negotiation playbooks: technical checklists for servo vs hydraulic choices, furnace architecture assessment, automation maturity mapping, and warranty/service commitment templates.

- Supply chain stress tests: stress scenarios for raw material spikes (reflecting that raw inputs account for the majority of steel manufacturing cost), lead‑time disruption simulations, and mitigation roadmaps including dual sourcing, inventory buffers, and flexible contracting.

- Factory readiness and upgrade checklists designed for 90‑day, 6‑month and 18‑month implementation milestones — covering civil works, utilities, controls integration, and operator training requirements.

- Regulatory and quality compliance playbook: how to operationalize in‑line monitoring to satisfy automotive heat‑treat standards, continuous monitoring KPIs, and audit preparation guidance.

- M&A and partnership screening heuristics: a calibrated model that ranks acquisition or JV targets on technology fit, installed base quality, geographic access, and integration cost to accelerate content localization strategies.

Strategic implications and recommended 2026 playbook

Our analysis yields three pragmatic pathways executives should consider when finalizing 2026 budgets:

- Efficiency retrofit first (low capex, high near‑term certainty): Prioritize retrofits that reduce energy consumption and increase throughput — a strong option where existing assets can be modernized with servo drives, improved furnaces, and added process monitoring. The combination often yields compressed paybacks and lowers operational risk.

- Turnkey new‑line investments (medium capex, rapid capability build): For OEMs committing substantial press‑hardened content to new platforms (including EVs), investing in integrated lines from established turnkey suppliers reduces time to ramp and transfers integration risk. Expect premium pricing for end‑to‑end delivery, but also stronger performance guarantees and digital support.

- Selective verticalization (capital and strategic exposure): For firms seeking control over critical supply chain elements or intending to capture aftermarket service revenue, acquiring or partnering with specialized press builders can create downstream opportunities — particularly where differentiation in tooling, part complexity, or production security matters.

Across all pathways, three cross‑cutting priorities matter: implement energy‑efficiency metrics into project IRR models, embed process monitoring requirements into supplier contracts, and stress‑test exposure to steel price volatility before final capital commitments.

Competitive intelligence highlights

Industry leaders continue to emphasize integrated solutions and energy gains. Recent vendor initiatives include multi‑layer furnace systems and multi‑part line concepts aimed at EV components; trade show activity highlights continued product innovation in heated platen and hot stamping technologies. These moves align with buyer demand for reduced operating cost and faster ramp capability.

From a market structure perspective, top players collectively hold a clear majority of high‑specification line supply, creating both opportunity and friction for new entrants. For buyers, that means securing favorable terms often hinges on playing multiple suppliers against each other while validating performance claims through staged acceptance tests and thermal traceability protocols.

How to use this brief and next steps

- If you are finalizing 2026 capital budgets: use our ROI templates and sensitivity scenarios to benchmark proposed projects against energy and throughput improvements rather than headline equipment prices.

- If you are negotiating supplier contracts: insist on performance SLAs tied to in‑line monitoring outputs and phased acceptance tied to documented CQI‑equivalent process records.

- If you are scouting M&A targets or JV partners: apply our acquisition heuristics to identify targets whose installed base and technology roadmap compress time‑to‑market for new press‑hardened content.

Conclusion — the strategic choice for 2026

Press hardening remains a core manufacturing technology for structural safety and lightweighting. The market’s projected expansion at a ~7.3% CAGR through the forecast period creates an environment where timely decisions on energy retrofits, turnkey investments, or targeted acquisitions will materially affect competitiveness. PW Consulting’s full report packages the data, models, and execution templates that procurement, operations, and corporate strategy teams need to move from intent to implementation in 2026.

For teams ready to translate strategy into procurement and plant‑level action plans, the full report delivers the granular tools — including vendor benchmarking, capex calculators, and contract templates — required to finalize commitments with confidence.

For detailed analysis of this topic, please visit the official page:Press Hardening Machine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com