North America Connectivity Infrastructure Investments Driving Industry Growth

Other |

2026-06-25 09:29:52

As PW Consulting’s senior strategy team and chief industry analysts, we are releasing a high-level briefing built from our forthcoming Industrial Grade Gamma-Butyrolactone (GBL) Market report (base year 2025, forecast window 2026–2032). This preview is designed to equip CFOs, procurement heads, product development teams, and M&A sponsors with the strategic context they need for resilient plans in 2026 — while directing executives to the complete study for granular, actionable datasets and supplier-level modelling.

Industrial Grade Gamma Butyrolactone Gbl Market

GBL is no longer a niche solvent; it sits at the intersection of battery materials, fine chemicals and high-performance solvents. Our top-line modelling shows an industrial-grade GBL market of USD 4,435.2 Million in 2025 that is forecast to expand to USD 6,443.25 Million by 2032, driven by a compound annual growth rate (CAGR) of 5.48% over the 2026–2032 forecast period. The first forecast year (2026) is projected at USD 4,718.94 Million, signaling steady near-term growth that compounds structural demand drivers such as battery electrode chemistries, specialty solvents for electronics and continuing needs in pharmaceuticals and agrochemicals.

Industrial Grade Gamma Butyrolactone Gbl Market

These macro dynamics matter because they change the calculus for supply strategy: a mid-single-digit CAGR coupled with episodic feedstock and regulatory shocks rewards partners who can guarantee quality, compliance and transparent lifecycle accounting — and penalizes firms that assume an “any-supplier” sourcing posture.

Industrial Grade Gamma Butyrolactone Gbl Market

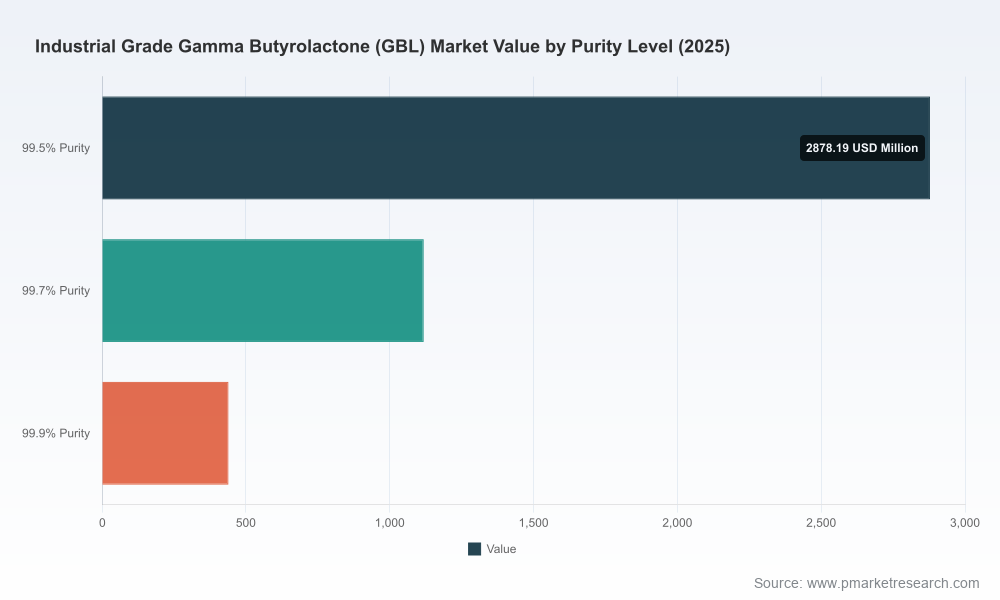

We intentionally omit proprietary granular tables in this preview — the full dataset includes regional, purity-level and application-level breakouts, granular price series and supplier-level capacity maps that are essential for negotiation and capital allocation.

Market concentration is meaningful but not monopolistic. The top three suppliers account for roughly 48.6% of installed commercial capacity, and the top five account for about 62.45% — a structure that enables disciplined behavior among incumbents while leaving room for regional and specialty entrants. From a strategic perspective, this concentration profile produces three practical effects:

Core players we assess in the full report and their strategic positions:

In sum, the competitive environment rewards two strategies: (1) securing differentiated product quality and compliance credentials, and (2) building flexible commercial frameworks that absorb episodic feedstock and price pressures.

GBL economics remain tightly coupled to 1,4-butanediol (BDO) feedstock dynamics and the broader oleochemical/oxirane markets. Our market workbench shows regional BDO price variance and ongoing short-run volatility; for instance, recent pricing observations in early 2026 indicate differential regional feedstock pricing that can change margin math for exporters and integrated producers.

Producers have responded with a mix of capacity management and commercial actions: some incumbents have announced modest capacity additions targeted at high‑purity grades used in electronics and battery materials, while others have applied selective price adjustments to offset feedstock inflation. The result is a market that is growing, but with capacity discipline and cyclic price pressure that make multi-year contracts and flexible tolling arrangements attractive to buyers seeking security of supply without overpaying for idled capacity.

These regulatory contours materially affect go‑to‑market models. For example, producers with robust product stewardship and compliance teams can capture higher-value contracts with electronics and pharmaceutical customers, while suppliers without those capabilities are increasingly relegated to lower-margin commodity business.

The full report converts the macro forecast and qualitative trends summarized here into practical tools: supplier heatmaps, contract negotiation playbooks, quantified business-case templates for sustainability investments, and scenario-tested demand curves for key downstream uses such as NMP synthesis and battery electrode solvents. It also contains a detailed appendix of recent supplier moves, including price actions, capacity investments and product stewardship updates — items that materially influence near-term negotiation leverage.

We designed the report to be a working document for 2026 planning cycles: usable at board level for capital allocation decisions, and at working level for procurement and legal to draft and negotiate robust supply agreements.

This preview is intended to guide 2026 actions and to demonstrate the kind of decision-grade intelligence PW Consulting delivers. The full Industrial Grade GBL Market report contains the granular regional, purity and application segmentation tables, rolling price-series, supplier-level capacity and contract modelling you need to operationalize the strategic choices summarized above.

Contact your PW Consulting account lead to schedule a briefing or to obtain the full report and associated modelling workbooks. For buy-side teams preparing negotiation windows in 2026, we recommend an immediate technical and contract review informed by the supplier scorecards and scenario playbooks included in the complete study.

For detailed analysis of this topic, please visit the official page:Industrial Grade Gamma Butyrolactone Gbl Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com