Az online kaszinók evolúciója: Milyen új trendek alakítják a jövőt 2025-ben?

Technology |

2026-05-31 11:43:16

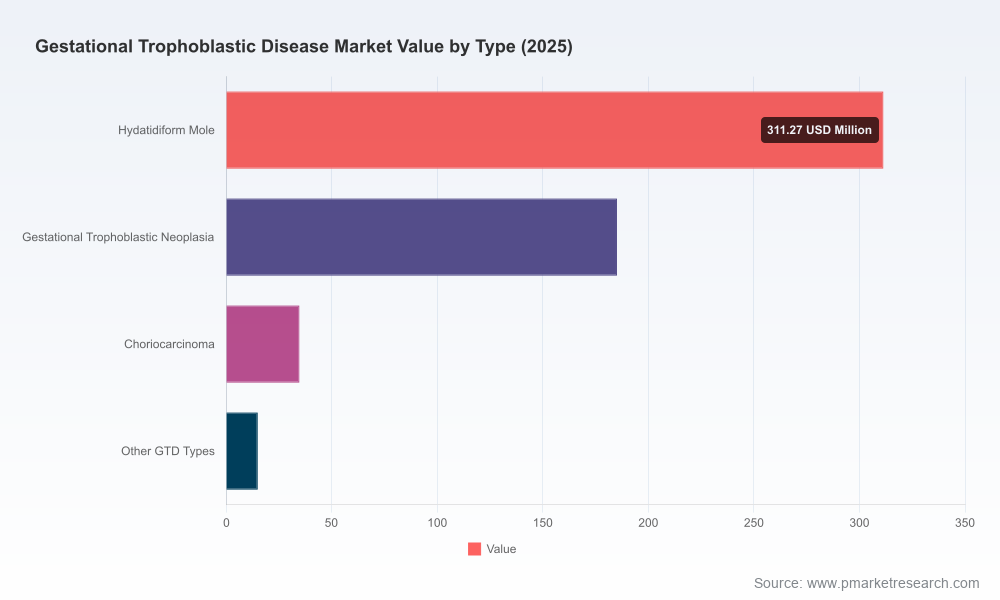

PW Consulting’s latest market study on Gestational Trophoblastic Disease (GTD) reframes the commercial and clinical landscape for 2026 decision‑makers. The GTD market has expanded steadily from approximately USD 412 million in 2020 to an estimated USD 546 million in 2025, and is projected to reach roughly USD 810 million by 2032—a compound annual growth rate (CAGR) of 5.81% across the 2026–2032 forecast horizon. Market concentration is moderate: the top three firms account for about 42.2% of revenue and the top five for roughly 58.4%, signalling a competitive environment where both brand and generic suppliers matter.

Gestational Trophoblastic Disease Market

This release presents the strategic takeaways from the full report and explains why the study is essential for manufacturers, investors, payers, and clinical groups planning moves in 2026. In keeping with our “trailer” approach, we demonstrate analytical depth and practical guidance while reserving the full, granular segmentation and numerical matrices for licensed subscribers.

Gestational Trophoblastic Disease Market

Clinical momentum around targeted immunotherapy and antibody approaches is altering treatment algorithms and payer narratives. Trial data presented at ESMO’s Sarcoma & Rare Cancers Congress (March 2026) showed avelumab plus an 8‑day methotrexate schedule achieved a 21% improvement in complete response (96.6% hCG normalisation) versus methotrexate alone in low‑risk GTN (TROPHAMET data with external controls). That result—and subsequent guideline incorporation—creates immediate market access and formulary implications.

Gestational Trophoblastic Disease Market

New international consensus guidance (2025) already recommends avelumab as an option in some countries to potentially avoid escalation to multi‑agent chemotherapy, embedding immunotherapy into treatment pathways and altering demand dynamics for single‑agent and multi‑agent chemotherapeutics.

Regulatory and reimbursement shifts (e.g., NHS England guidance recommending pembrolizumab for patients who fail two or more lines) demonstrate payers’ willingness to accept high‑cost therapeutics in refractory cases—setting a precedent for coverage decisions that will reverberate through 2026 contract negotiations and pricing strategies.

The market trajectory—from the mid‑hundreds of millions in 2025 to an approximately USD 810 million opportunity by 2032—reflects a mixture of stable demand for well‑established chemotherapeutic agents and an expanding addressable market driven by immunotherapies, off‑label checkpoint inhibitor use, and evolving diagnostics/monitoring practices. The 5.81% CAGR is underpinned by three structural forces:

Incremental adoption of immuno‑oncology into earlier lines of therapy (shifting product mix and revenue per treated patient);

Continued reliance on generics and injectables for standard regimens, sustaining baseline volume; and

Improving detection, follow‑up (hCG monitoring), and centralized care pathways that increase treatment capture and follow‑on healthcare utilisation.

Driver — Therapeutic innovation: Positive avelumab data and active exploration of checkpoint inhibitors (pembrolizumab, camrelizumab, toripalimab) for chemo‑resistant GTN expand therapeutic options. Strategic implication: innovators should prioritise lifecycle programmes, label expansion strategies, and payer evidence generation to secure first‑line or earlier‑line access.

Driver — Guideline alignment: International consensus recommending immunotherapy options accelerates uptake in markets with guideline‑driven procurement. Strategic implication: market access teams must synchronize HTA dossiers and real‑world evidence plans with guideline timelines to avoid access lag.

Headwind — Reimbursement scrutiny: Off‑label and trial‑based use of checkpoint inhibitors without formal regulatory approval for GTN in most regions creates reimbursement uncertainty. Strategic implication: manufacturers should invest in pragmatic trials, registries and outcomes agreements to de‑risk payer adoption.

Headwind — Generics and pricing pressure: A significant volume of GTN care relies on generic methotrexate, actinomycin D and other injectables. Strategic implication: producers of branded immunotherapies must craft value propositions that clearly demonstrate cost offsets (e.g., avoiding multi‑agent chemotherapy and reducing hospitalisations) to withstand tendering and price compression.

Emerging risk/option — Non‑drug modalities and repurposing: Focused ultrasound remains early‑stage; statin repurposing for choriocarcinoma is in preclinical discussion. Strategic implication: keep an R&D radar on non‑traditional entrants and repurposing studies—these can provide acquisition, licensing or partnership opportunities down the line.

The report profiles incumbent and potential entrants across drug classes and supply chains. Key strategic observations:

Big pharma oncology players (e.g., Pfizer, Novartis, BMS) retain influence via established chemotherapy portfolios and oncology pipelines. Their dual role as suppliers of standard agents and partners in immunotherapy development gives them optionality to protect share as regimens evolve.

Generic manufacturers (e.g., Teva, Hikma, Fresenius Kabi) underpin the standard‑of‑care backbone. Their cost leadership and manufacturing scale create barriers to price increases for older agents but also position them as natural partners for combination product launches or co‑supply agreements.

Immune‑oncology incumbents and alliances (e.g., Merck with pembrolizumab; Merck KGaA/Pfizer for avelumab) are the catalysts for change. Their trial programmes and real‑world evidence strategies will determine how quickly immunotherapy moves from salvage therapy to earlier lines.

Strategic playbooks emerging from our analysis: (1) innovators must integrate payer evidence and guideline engagement from phase II onward; (2) generics firms should evaluate bundled service offerings (diagnostics + drug + monitoring) to maintain margin; (3) mid‑sized firms can pursue focused niches (e.g., diagnostic monitoring devices or regional supply agreements) to exploit areas of lower concentration.

TROPHAMET downstream analyses and external validation cohorts — will payers accept single‑arm comparison data as sufficient for earlier‑line coverage?

Guideline adoption timelines across major markets — the 2025 consensus was a leading indicator; local guideline updates will drive adoption waves.

HTA outcomes and NHS‑style coverage determinations for checkpoint inhibitors in GTN — successful coverage decisions create a template for other markets.

Regulatory filings and label extension strategies for immunotherapies — formal approvals would materially change market dynamics and revenue concentration.

PW Consulting’s full GTD Market report is structured to support immediate strategic decisions in 2026. Key deliverables include:

A validated market model (historical 2020–2025; forecast 2026–2032) with scenario toggles to test uptake assumptions for immunotherapies, diagnostics, and surgical interventions;

Granular commercial matrices: product‑level forecasts, pricing bands, revenue waterfalls by payer segment and sales channel (note: detailed regional and segment tables are proprietary to the full report and not published in this release);

Competitive profiles and capability heat maps for the leading suppliers, including manufacturing footprints, tender exposure, and product vulnerability analyses;

Market access playbooks and recommended evidence packages tailored to five archetypal market types (early adopter, guideline‑driven, tender‑dominated, mixed reimbursement, limited‑access);

Commercial execution checklists for 12–24 month horizons focused on pricing, contracting, clinical engagement, and real‑world evidence programmes;

Risk register and opportunity scan covering technology disruption (e.g., focused ultrasound), repurposing science (e.g., statins), and supply chain stress tests.

R&D and portfolio owners: Prioritise immunotherapy combination studies that include economic endpoints and biomarker‑guided cohorts. Early payer engagement is non‑negotiable.

Commercial leaders: Model three adoption scenarios (conservative, guideline‑led, accelerated) and build flexible pricing strategies—consider outcome‑based agreements for high‑cost immunotherapies to accelerate formulary acceptance.

Manufacturing and supply chain: Expand capacity for sterile injectables and plan dual‑sourcing for core chemotherapeutic agents—supply disruptions can rapidly shift tender outcomes.

M&A and corporate development: Look for bolt‑on assets in diagnostics, hCG monitoring, and registries; evaluate acquisition targets that offer differentiated access to GTN centres of excellence.

Payers and hospital systems: Prepare budget impact assessments for likely immunotherapy uptake scenarios, and negotiate bundled care pathways to capture downstream savings from avoided multi‑agent chemotherapy and hospital stays.

2026 is the year when clinical data, guideline evolution, payer precedent, and commercial readiness converge to reshape GTD care pathways. The market offers steady growth—anchored by established chemotherapies—and a material upside driven by immunotherapy adoption and improved diagnostics. Competitive dynamics are neither monopolistic nor atomised, creating room for manoeuvre through partnerships, differentiated evidence generation, and smart contracting.

PW Consulting’s full report supplies the detailed segmentation, numerical scenarios, and playbooks that commercial, clinical and policy leaders need to convert insight into outcomes. For access to the complete datasets, proprietary regional and treatment splits, and executable market‑entry templates, visit our report page or contact the PW Consulting industry desk to request a briefing.

For detailed analysis of this topic, please visit the official page:Gestational Trophoblastic Disease Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com