Automated Side Load Garbage Trucks: Strategic Imperatives for 2026 — PW Consulting Market Brief

PW Consulting’s new market study on Automated Side Load Garbage Trucks outlines the strategic inflection points municipal fleets, private waste operators, OEMs, and investors must act on in 2026. Built on a verified historical dataset (2020–2025) and a forward-looking forecast (2026–2032), the report synthesizes commercial, regulatory, and technical drivers into an operational playbook for decision-makers. This release highlights the report’s core messages and tactical value while preserving the detailed segmentation and proprietary numerical matrices that drive our models — a curated preview designed to demonstrate analytic depth and motivate access to the full report for procurement- and investment-grade intelligence.

Automated Side Load Garbage Trucks Market

Market Trajectory — What the topline numbers tell you

The automated side load garbage truck market has transitioned from niche replacement demand to a mainstream fleet modernization category. In raw terms, the market expanded meaningfully through the early-2020s and reached approximately USD 2,050 Million in our base year (2025). Our forecast shows sustained growth through 2032 at a compound annual growth rate (CAGR) of 6.42%, with the market surpassing the USD 3 billion threshold by the end of the forecast window. The pace of adoption and capex cycles embedded in the forecast reflect a mix of replacement, regulatory-driven fleet renewals, and new deployments where automated collection unlocks operating efficiencies.

Automated Side Load Garbage Trucks Market

Why 2026 is a decision year

- Regulatory deadbands and procurement cycles converge in 2026: municipalities and private contractors who delay decisions risk losing access to lead-time constrained configurations (electric variants, CNG integrations, and specialized chassis).

- Technology transition management: electrification pilots completed in 2023–25 are now ready for scaling, but operational readiness — depot power, skilled technicians, and TCO visibility — remains uneven.

- Competitive repositioning: established body manufacturers and newer niche specialists are sharpening value propositions around total cost of ownership (TCO), uptime guarantees, and service networks; procurement strategies made in 2026 will materially affect cost curves through the late-2020s.

Report contents — practical deliverables for operators and investors

This study was written as a practitioner’s toolkit. Key deliverables include:

Automated Side Load Garbage Trucks Market

- Market sizing and multi-year forecasts (2026–2032) with scenario variants calibrated to fuel price shocks, regulatory tightening, and technology learning curves.

- Operator-grade TCO models that decompose capex, maintenance, energy/fuel, and residual value under diesel, CNG/LNG, and electric powertrains.

- A procurement playbook for RFPs and vendor evaluation — including scoring templates for durability, service footprint, interoperability, and safety compliance.

- Deployment playbooks for pilots and scale-ups covering depot infrastructure, workforce transition, and change-management milestones.

- Regulatory and safety checklist tied to compliance timelines (emissions rules, OSHA/ EU Machinery Directive requirements, and local low-emission zones).

- Operational risk heatmaps and mitigation steps for supply-chain disruption, component obsolescence, and warranty exposure.

- Vendor profiles and strategic positioning maps (high-level competitive assessment included in this brief; full vendor scoring in the paid report).

Competitive landscape — who matters and why

The automated side loader market remains anchored by a set of established body manufacturers that combine deep field experience with product breadth. The ecosystem includes legacy innovators, high-volume production houses, and specialized narrow-focus builders. Our report examines each company through the lens of product robustness, electrification readiness, service network, and aftermarket economics. Highlights from companies covered (high-level):

- Heil Environmental (Chattanooga, Tennessee, USA) — Recognized for a broad automated side loader portfolio and electric collection body offerings. Strengths: mature arm mechanism designs and product lines tailored to both residential and commercial collection operations.

- McNeilus Truck and Manufacturing (Dodge Center, Minnesota, USA) — Emphasizes flexible arm geometries and models engineered for constrained routes; notable for adaptable integration across diesel and electric chassis.

- Labrie Enviroquip Group (Quebec, Canada) — Known for modular designs that span manual, semi-automated, and fully automated applications, appealing to mixed-fleet operators in North America.

- New Way Trucks (Scottdale, Iowa, USA) — Offers high-capacity lifting systems and under-CDL options, attractive to fleets balancing crew-size economics with route productivity.

- Amrep (California, USA) — Differentiates on materials and wear resistance, delivering bodies optimized for longevity in heavy-use municipal applications.

- Curbtender Inc. (USA) — A specialist historically credited with commercializing the automated side loader; continues to focus solely on this niche with multiple model variants.

- KANN Manufacturing (USA) — Supplies high-compaction automated side loaders with diverse body size options for heavy municipal duty cycles.

These firms, along with a broader supplier base, operate in a market that demonstrates moderate concentration — meaning market leadership exists, but differentiated offerings and service depth create pockets of competitive advantage. Our concentration analysis (CR3 and CR5 indicators) and supplier scoring appear in the full report; those metrics are central to procurement risk assessments and are intentionally withheld from this preview.

Regulatory and technical drivers shaping procurement

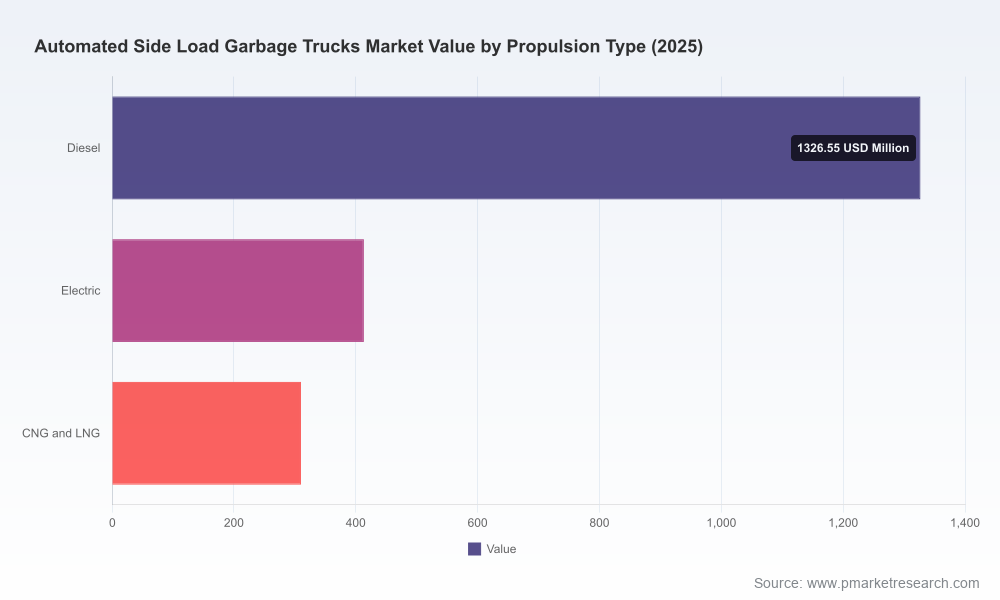

- Emissions and low-emission mandates: Stringent rules in key jurisdictions are accelerating electrification and adoption of CNG/LNG where electric infrastructure is constrained. This creates mixed-fleet strategies through the late 2020s.

- Safety and machinery standards: Mandatory incorporation of anti-collision sensors, operator presence detection, and emergency override systems is now a baseline requirement in several markets — impacting retrofit strategies and specification language for new builds.

- Technical ergonomics: Automated arms and hydraulic systems are engineered to handle containers from small curbside formats up to heavy-duty formats with long reach and high compaction ratios; electric body variants commonly use independent battery systems to power collection duties separate from the vehicle chassis.

Practical strategic recommendations for 2026

- Adopt a staged electrification roadmap. Start with high-visibility routes and depots with available grid capacity while keeping a defined conversion path for secondary depots. Use TCO models to compare independent-body battery systems versus integrated chassis solutions.

- Write procurement specifications that prioritize serviceability and uptime guarantees. Require supplier commitments on parts availability, technician training, and depot commissioning support.

- Negotiate performance-based contracts that align supplier incentives with lifecycle outcomes (uptime, fuel/energy consumption, safety incidents).

- Use pilot programs to validate infrastructure scaling assumptions. Insist on pre-defined success criteria and a commercial transition clause if a pilot meets or exceeds targets.

- Assess acquisition targets and partnerships through the lens of aftermarket control — service networks and parts supply are often more valuable than marginal improvements in vehicle efficiency.

- Factor regulatory risk into fleet replacement cycles; where compliance windows are near, choose solutions that minimize retrofit exposure.

How PW Consulting supports execution

We translate these insights into executable deliverables: custom TCO scenarios, procurement templates, vendor due diligence, pilot design and evaluation, and integration roadmaps for depot infrastructure. Our hands-on engagements typically include a stakeholder-aligned decision calendar and an implementation scoreboard that ties capex commits to measurable operating targets.

Next steps — where to get the full intelligence

This brief is a strategic preview. The full PW Consulting Automated Side Load Garbage Trucks Market Report delivers the granular segmentation, region- and propulsion-specific forecasts, proprietary supplier scoring matrices, and downloadable TCO models that procurement teams and investors need to finalize 2026 decisions. For teams preparing RFPs, capital plans, or M&A screens this year, the depth contained in the full study materially reduces execution risk and accelerates time-to-value.

Contact PW Consulting to arrange a licensed copy of the report, a briefing, or a tailored workshop to convert these insights into a 12–36 month action plan.

For detailed analysis of this topic, please visit the official page:Automated Side Load Garbage Trucks Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com