Acute Care Telemedicine Services Market: Strategic Imperatives for 2026

PW Consulting’s new market research brief on Acute Care Telemedicine Services synthesizes five years of historical data and a seven-year forecast to deliver a pragmatic, decision-ready view of a market undergoing rapid normalization and scale. With a 2025 base year and a projected compound annual growth rate (CAGR) of 14.82% across the 2026–2032 forecast window, this market is transitioning from experiment to mission-critical infrastructure for health systems, regional networks, and specialist-provider platforms. Our goal in this summary is to surface the strategic signals that matter for 2026 planning while preserving the granular, monetized splits that make the full report essential for transaction and investment decisions.

Acute Care Telemedicine Services Market

Market snapshot: growth trajectory you cannot ignore

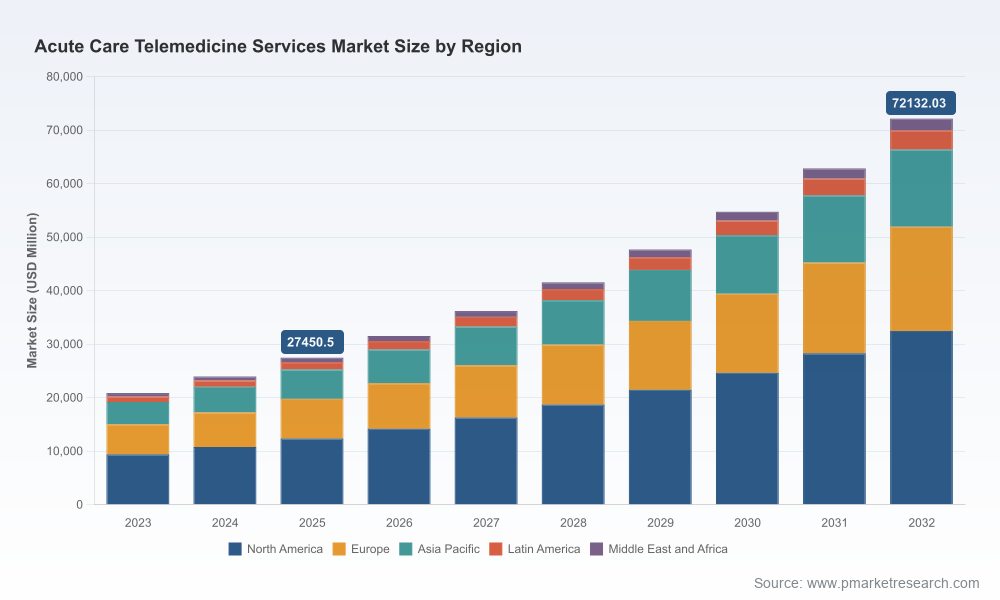

Acute care telemedicine has demonstrated sustained, high-double-digit expansion at the enterprise level. Our topline model shows the market expanding from approximately USD 20.85 billion in 2023 to USD 27.45 billion in 2025 (base year), and continuing to roughly USD 31.5 billion in 2026 as providers and payers embed virtual acute care into operational protocols. By 2032, the market reaches a multi-decade inflection point, projected at roughly USD 72.13 billion under our base-case assumptions. This trajectory—driven by clinical adoption, capital reinvestment, and scope expansion across ICU, stroke, emergency, and hospitalist workflows—creates palpable strategic options for incumbent health systems, vendor platforms, and new entrants.

Acute Care Telemedicine Services Market

Why this report matters for 2026 decision-makers

- Investment timing: The market’s 14.82% CAGR implies accelerating returns if investments align with operational readiness. 2026 is a pivotal year for organizations to move from pilot programs to scaled service lines without overpaying for legacy point solutions.

- Competitive positioning: Market concentration metrics show a mid-level aggregation—top three firms capture roughly 38% of spend, and the top five roughly 52%—indicating meaningful incumbent advantage but abundant room for focused challengers.

- Regulatory & reimbursement sensitivity: Near-term reimbursement policy and interstate licensure rules will be the primary constraining variables; scenario planning around reimbursement parity and licensure portability is a non-negotiable for 2026 budgets.

- Operational complexity: Successful scale requires more than video carts—EHR interoperability, command-center staffing models, quality governance, and local credentialing workflows determine the difference between tactical wins and failed implementations.

What the full PW Consulting report delivers (practical, executable content)

- Historical market tracking (2020–2025) and a granular, auditable topline model for 2026–2032 that supports customized scenario adjustments.

- Segment-level frameworks (regional, service-line, delivery-model) with revenue drivers and sensitivity levers—note: precise segment monetizations are reserved for the full report to preserve competitive value.

- Buyer personas and procurement playbooks for three archetypal buyers: tertiary health systems, regional networks/rural hospital consortia, and digital-native platform vendors.

- Go-to-market blueprints, including contracting archetypes, pricing models tied to reimbursement regimes, and integration checklists for EHR, imaging, and bedside monitoring.

- Operational playbooks for staffing (credentialing, scheduling, retention), technology stack selection (latency, security, standards), and quality measurement (clinical KPIs and compliance triggers).

- Vendor scorecards, a monitored M&A pipeline, and exit scenarios to inform negotiations and investment committees.

Competitive landscape: pragmatic analysis of core players

The acute care telemedicine ecosystem is a mix of large-platform vendors, regional networks, and specialty-focused providers. Each group plays a distinct role in shaping adoption patterns.

Acute Care Telemedicine Services Market

- Access TeleCare (Dallas) has repositioned through a strategic rebrand to emphasize multi-specialty acute coverage. Its 24/7 model and hospital-focused services make it a go-to partner for hospitals seeking turnkey, specialty-rich coverage.

- Eagle Telemedicine (Leawood) is representative of the nimble regional provider: focused deployments for rural and critical-access hospitals, with the agility to win in lower-density markets where tailored workflows and rapid local partnerships matter most.

- Avera eCare (Sioux Falls) operates at scale as a network incumbent, providing command-center oversight and deep integration into hospital workflows—an exemplar for large health systems exploring internal command-center models or outsource partnerships.

- Teladoc Health (Purchase) and Amwell (Boston) each leverage platform breadth and enterprise sales channels to package acute modules into broader virtual care suites; their strengths lie in enterprise integration, product roadmaps, and cross-sell to ambulatory telehealth customers.

- Sound Physicians (Tacoma) offers an interesting hybrid: clinical-first programs that blend tele-hospitalist services with on-site management, attractive to health systems seeking to preserve clinical governance while scaling remote coverage.

Strategic takeaway: buyers should segment shortlist decisions by whether they prioritize clinical coverage depth, operational integration, or platform extensibility. Winners in 2026 will pair credible clinical outcomes with predictable implementation timelines and transparent price-to-benefit profiles.

Recent moves and what they signal

- Rebranding and capability expansion among specialty-focused vendors signal intensified competition for hospital-level contracts, not just episodic telehealth engagements.

- Expansion by regional providers highlights continued demand in underserved geographies—these markets are defensive opportunities for health systems seeking to maintain referral networks.

- Strategic partnerships between network-scale operators and regional health systems point to a pragmatic hybrid model: centralized clinical command centers with locally embedded operational ownership.

Market dynamics and operational risks

- Reimbursement: Policy has been supportive recently—examples include parity initiatives for tele-stroke and tele-ICU under certain Medicare rules. However, much of the near-term policy environment is time-limited, requiring payers and providers to model at least two alternative reimbursement scenarios when sizing investments.

- Licensure and workforce: Interstate practice remains constrained by state licensure unless clinicians use compacts. Staffing shortages are driving labor cost inflation—our review of workforce studies attributes a 15–20% increase in acute telemedicine physician staffing costs in many rural programs—making efficient rostering and occupancy optimization essential.

- Technology standards and quality: Vendors and health systems must meet video, bandwidth, and data-integration thresholds to support clinical decision-making; adherence to ATA guidelines and Joint Commission accreditation requirements will be table stakes for enterprise contracts.

- Consolidation risk: Market concentration metrics indicate that top firms control meaningful share but not dominance. This creates M&A opportunity windows for strategic buyers and private equity, and competitive pressure on midsize vendors to consolidate or specialize.

Actionable playbook for 2026—what leadership teams should do now

- For CFOs: Build multi-scenario financial models that stress-test reimbursement rollbacks, variable clinician rates, and integration capex. Use the report’s ROI templates to size payback windows under conservative and upside cases.

- For Chief Medical Officers & Clinical Ops: Prioritize clinical pathways that yield measurable outcomes within 6–12 months (e.g., door-to-needle for tele-stroke, ICU readmission reductions) and tie vendor contracting to these KPIs.

- For CIOs: Lock in interoperability and cyber‑security requirements up-front; insist on vendor SLAs for latency and video resolution aligned with ATA guidance, and budget for EHR and monitoring integrations.

- For Corporate Strategy & BD: Evaluate three strategic moves—build (internal command-center), buy (vendor acquisition), or partner (long-term network agreements)—using our decision framework that weighs speed, cost, clinical control, and scalability.

How PW Consulting supports your 2026 roadmap

Our acute care telemedicine engagement suite blends market intelligence with hands-on execution support—tailored market-sizing with customizable scenarios, vendor selection RFPs and scorecards, contract negotiation support, integration roadmaps, workforce optimization models, and M&A diligence. We intentionally provide enough topline visibility here to guide executive priorities while reserving the monetized segmentation and vendor-level financials for clients and authorized report purchasers to preserve commercial value.

Next steps

Leaders preparing 2026 capital plans and operational roadmaps should use this research as a timing and prioritization lens. If your organization is evaluating scale vs. specialization, negotiating enterprise vendor agreements, or assessing acquisition targets, PW Consulting’s full Acute Care Telemedicine Services Market report offers the calibrated, monetized insight and execution templates you need to de-risk those decisions. The complete report includes the full segmented financial model, vendor scorecards, and playbooks referenced above—available through our client portal and authorized distribution channels.

PW Consulting’s analysis is designed to convert growth expectations into executable programs. For boards, operating committees, and investor teams, 2026 is the year to move beyond pilots and lock in the operational architectures and commercial contracts that will define competitive advantage in this rapidly expanding market.

For detailed analysis of this topic, please visit the official page:Acute Care Telemedicine Services Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com