Lip Fillers Market Size, Share, and Growth Opportunities

Other |

2026-06-26 06:52:23

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a concise but forward-looking briefing drawn from our latest Off Road Fuel Tank Market study. This release is intended to orient executive decisions for 2026 — highlighting the macro trajectory, the competitive landscape, and the practical levers that will determine winners and laggards across materials, OEMs, and aftermarket channels. Think of this as a trailer: we show the analytical frame and strategic implications while reserving full segment-level detail for the full report.

Off Road Fuel Tank Market

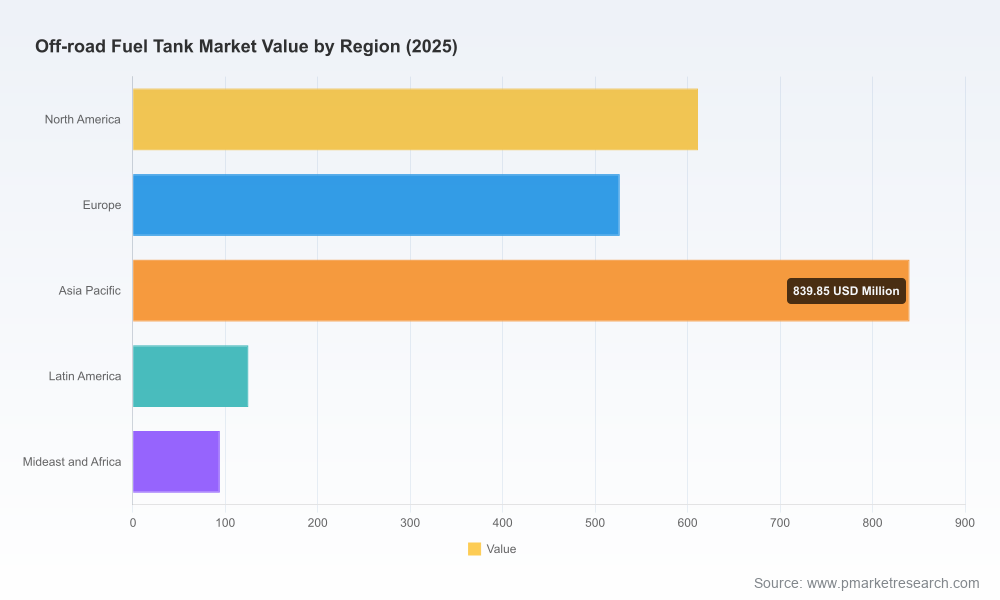

The off road fuel tank market has moved steadily through the early 2020s and enters 2026 on an upward trajectory. Our bottom-up sizing shows the market expanding from the low‑mid billions in 2020 to roughly 2.2 billion USD by the 2025 base year, and we project continued growth to exceed 3.1 billion USD by 2032, representing a compound annual growth rate (CAGR) of about 5.48% across the 2026–2032 forecast window.

Off Road Fuel Tank Market

For corporate leaders, that steady, multi-year growth profile implies two simultaneous strategic imperatives: (1) build scalable capabilities to capture expanding demand, and (2) adapt product, cost and compliance strategies to a changing input-cost and regulatory environment. The next sections unpack the drivers behind those imperatives and translate them into actionable choices for 2026.

Off Road Fuel Tank Market

Regulation as a design constraint and differentiation lever: Emissions and permeation standards from agencies such as EPA and CARB are tightening enforcement on evaporative emissions for small off-road equipment. At the same time, heavy-duty greenhouse gas standards are extending scrutiny into off‑highway fuel systems. These regulatory forces are accelerating adoption of multi-layer plastic constructions and other permeation-reduction technologies — making compliance an entry requirement rather than a value-add.

Raw material volatility and its asymmetric impact: Metal and polymer pricing dynamics are materially changing input cost profiles. Notably, aluminum mill shapes and steel mill products experienced pronounced increases year-over-year, and HDPE prices have risen into the mid‑triple digits per metric ton in the recent period. These trends force a re-evaluation of make-versus-buy dynamics, material mix strategies, and hedging approaches across metal and plastic fuel tank producers.

Channel bifurcation — OEMs versus aftermarket: Demand for factory-fitted tanks (driven by OEM procurement cycles and regulatory compliance) continues alongside resilient aftermarket demand for extended‑range, replacement and auxiliary systems used in exploration, large-scale construction, and resource extraction. The two channels have distinct margin structures, service expectations and product innovation cadences.

Application-driven secular tailwinds: Construction, agriculture, mining and specialty off-road segments each present different lifecycle pacing and durability expectations. As equipment electrification progresses unevenly across applications, diesel and liquid-fuel tanks retain strategic relevance in heavy-duty and remote operations, underscoring continued investment focus.

The market remains moderately consolidated: the top three players account for a meaningful share of industry revenue while the top five approach roughly half of the market — a structure that creates space for niche specialists and potential scale consolidators alike.

Strengths: Broad metal fabrication capabilities across steel and aluminum, deep OEM relationships, and the ability to produce a wide range of capacities for specialized off‑highway applications. Strategic implication: IFH is well-placed to win specifications where customer requirements emphasize metal durability or bespoke configurations. For 2026, focus on modular platforming and cost pass-through clauses will preserve margins amid metal price volatility.

Strengths: Durable system designs tailored to harsh environments and heavy construction equipment. Strategic implication: Leverage engineering services and lifetime warranty frameworks as competitive differentiators in OEM procurement negotiations, while exploring design-for-cost initiatives to mitigate input-price pressure.

Strengths: High-volume blow molding expertise, multi‑layer HDPE capability and compliance with low‑permeation standards. Strategic implication: This player exemplifies the scale and regulatory alignment required to dominate plastic tank supply for agricultural and turf equipment. For 2026, securing polymer supply and optimizing resin usage will be a priority.

Strengths: European footprint, plastics know‑how and regulatory certifications for small off‑road vehicles. Strategic implication: European regulation and export channels favor established suppliers with certified processes. Partnerships with vehicle OEMs and standards bodies will protect access to premium segments.

Strengths: Aftermarket specialization — extended range systems, advanced polymers and custom aluminum/stainless solutions. Strategic implication: These brands command customer loyalty in niche aftermarket channels. Strategic plays for 2026 include expanding channel partnerships, product bundling with filtration or refueling systems, and premium service offerings for remote operations.

Strengths: Heavy-duty fleet solutions (large-capacity beds and lube trucks) and highly engineered safety bladders respectively. Strategic implication: Operators in mining and racing require extreme reliability and certified safety. Targeted R&D and service contracts will be the primary routes to margin expansion.

Prioritize material and supplier diversification: With metal and polymer prices elevated and volatile, build dual-sourcing strategies and identify substitute materials where lifecycle analysis supports the switch.

Lock in polymer supply or secure resin off-take agreements: For manufacturers pivoting to multi-layer HDPE, upstream security directly reduces production disruption risk and stabilizes margins.

Embed regulatory compliance into product roadmaps: Treat permeation and emissions limits as design constraints from day one. Multi-layer plastics, barrier coatings, and certification playbooks shorten time-to-market.

Revisit pricing architecture and cost-pass mechanisms: Transparent indexation clauses tied to aluminum, steel and resin indices can protect margins while reducing negotiation friction with OEM customers.

Develop aftermarket service propositions: Extended-range refueling, on-site maintenance packages and modular retrofit kits unlock recurring revenue beyond OEM cycles.

Target bolt-on M&A to fill capability gaps: Given the market’s moderate concentration, acquiring specialized blow-molding capacity, testing labs, or regional distribution can accelerate growth more predictably than greenfield investments.

Invest in lightweighting and recyclability R&D: Material and carbon constraints increasingly shape procurement decisions among large equipment OEMs.

Optimize factory footprints: Rebalance production between metal and plastic lines in response to material cost curves and proximity to key OEM clusters.

Leverage digital twins and accelerated testing: Rapid validation of permeation, crash and thermal performance reduces certification timelines and accelerates specification wins.

Scenario‑proof strategic plans: Build alternate investment cases reflecting high‑input‑cost and accelerated electrification scenarios to guide CAPEX decisions in 2026.

Our full Off Road Fuel Tank Market report goes far beyond the strategic highlights above. It includes operational and commercial tools designed to be put into practice immediately:

Transparent methodology and a reconciled market-size model covering 2020–2032, with scenario variants for input-cost stress and regulatory tightening.

Supplier benchmarking and a competitive capability map across metal and plastic fabrication, testing and certification capacities.

Cost build-ups and margin sensitivity analyses that show how aluminum, steel and HDPE price movements flow to gross margins.

Regulatory matrix and compliance playbooks for EPA, CARB and heavy-duty emissions standards, with design requirements and certification timelines.

Go‑to‑market playbooks for OEM contracts and aftermarket scaling, including channel economics and service-model templates.

M&A pipeline candidates and integration checklists targeted at capability fill‑ins and regional access.

To respect the “trailer” principle, we intentionally omit granular segment tables and regional breakdowns in this release. The full dataset — including detailed regional and application splits, company-level share estimates, and downloadable financial models — is available to report subscribers and corporate clients via our secure portal.

2026 represents a window where strategic choices around materials, compliance, and channel focus will compound into multi-year advantage or erosion. The market’s steady CAGR near 5.5% offers attractive topline opportunities, but the combination of raw material cost shifts and tightening emissions/permeation rules raises the bar for operational excellence and regulatory foresight.

Executives who treat 2026 as a year to secure material supply, embed compliance into product design, and selectively scale aftermarket and service revenue streams will find themselves best positioned as the market expands toward the early 2030s. The PW Consulting Off Road Fuel Tank Market report is structured to be a decision-making tool for that agenda — giving you the numbers, scenarios and playbooks to act with confidence.

For access to the full report, detailed segment data, and customized briefings for your executive team, please visit our report page or contact PW Consulting’s Industry Advisory Desk.

For detailed analysis of this topic, please visit the official page:Off Road Fuel Tank Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com