Circular Liquid Crystal Polymer Connector (LCP) Market Assessment: Growth Opportunities, Innovation and Industry Outlook

Networking |

2026-06-04 16:23:27

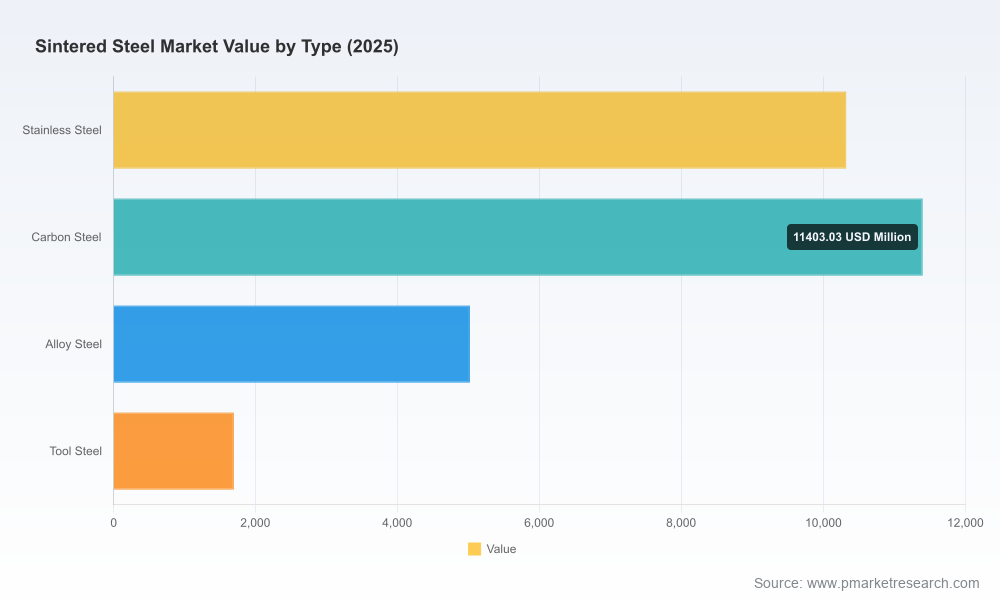

As companies finalize 2026 budgets and capital plans, the sintered steel value chain sits at a crossroads of steady demand expansion and accelerated structural change. Our new PW Consulting market study shows the global sintered steel market reached approximately USD 28.45 billion in 2025 and is projected to grow at a 5.39% compound annual growth rate through 2032, surpassing the USD 41 billion mark by the end of the forecast window. This steady macro trajectory belies a landscape in which raw-material volatility, regulatory tightening, electrification, and additive manufacturing will materially rewire competitive advantage over the next 18–36 months.

Sintered Steel Market

Capital allocation: With predictable top-line growth but rising input-cost risk, capex must be tied to flexibility — not just scale. Investments that increase throughput without improving supply optionality or material efficiency risk margin erosion.

Sintered Steel Market

Supply security: Recent iron-powder price shocks underline the need for multi-source strategies and hedging mechanisms across powder grades.

Sintered Steel Market

Product roadmaps: The shift toward electric drivetrains and higher-efficiency motors demands new powder chemistries and soft-magnetic composites; companies that pre-validate materials for EV and e-machine specifications shorten time-to-win with OEMs.

Regulatory compliance: New REACH impurity thresholds for nickel-containing powders and persistent trade measures (e.g., maintained tariffs) require proactive compliance and sourcing plans to avoid sudden supply disruptions.

Forward-looking market sizing and scenario modelling: Base-year (2025) calibration and seven-year forecasts to 2032 using bottom-up demand drivers and scenario overlays that stress-test material-price, tariff, and adoption assumptions.

Commercial playbooks: Route-to-market and pricing frameworks segmented by product family, production technology, and customer type — designed for use in commercial planning and negotiation playbooks.

Supply-chain and procurement diagnostics: A framework to quantify single-source exposure, cost-to-serve by powder grade, and inventory levers that protect margins during spot-price spikes.

Technology and CapEx roadmaps: Comparative assessment of sintering, powder metallurgy routes, and additive manufacturing (including binder-jetting powders) with time-to-scale, unit-cost, and quality-compatibility estimates.

Regulatory and sustainability impact matrix: Compliance timelines, capital implications of tighter impurity limits, and recommendations for low-carbon material sourcing.

M&A and partnership targeting: A prioritized list of capability targets (material producers, binder-jetting powder specialists, regional toll-sinterers) with fit/gap analysis against buyer objectives.

Executive decision-support appendix: Board-ready slides, KPI dashboards, and a one-page investment thesis for each strategic option.

The sintered steel sector remains moderately concentrated: the top three players account for roughly a third of the market and the top five approach half the market — an arrangement that creates meaningful advantages for established producers while leaving space for disruptive entrants with differentiated technology or supply propositions. For buyers and investors, this structure implies a dual strategy: cultivate strategic relationships with incumbents to secure scale supply, while selectively partnering with nimble innovators to access new materials and processes.

GKN Powder Metallurgy (Bonn, Germany) — A global leader in sintered transmission and structural components. GKN’s recent capacity expansion in North America to support EV drivetrain demand is a deliberate play to lock OEM platform wins. For companies evaluating supplier partnerships, GKN’s scale and OEM relationships make it a strategic anchor, but procurement teams should insist on transparent pricing mechanisms to manage input-risk pass-through.

Hoeganaes Corporation (Bala Cynwyd, PA, USA) — A leading atomized powder supplier. Its launch of a high-strength powder grade in 2024 signals a push to capture higher-margin, performance-sensitive automotive parts. For parts manufacturers, early engagements around validation programs with Hoeganaes can shorten qualification cycles.

Hoganas AB (Hoganas, Sweden) — Specialist in high-performance powders and soft-magnetic composites. The Somaloy 700 series launch for high-efficiency electric motors is a noteworthy example of product-level innovation aligning with e-machine demand. Manufacturers focused on EV motor components should incorporate testing paths for soft-magnetic composites into 2026 development roadmaps.

Sumitomo Electric Industries (Osaka, Japan) — Established in sintered parts for shock absorbers, gears, and bearings. Sumitomo’s integration of powder metallurgy with automotive supplier relationships positions it as a reliable partner for tier-1 developers.

Mitsubishi Materials Corporation (Tokyo, Japan) — Produces sintered components across automotive and electronics. Its diversified manufacturing footprint can be advantageous for customers seeking redundancy and regional compliance support.

Hitachi Powdered Metals (Chiba, Japan) — Specializes in precision gears and structural parts for transmissions. Hitachi’s emphasis on quality and process control makes it a natural partner where durability and tight tolerances are non-negotiable.

Porite Taiwan Co., Ltd. (Taoyuan, Taiwan) — Niche player in precision sintered parts for power tools and appliances. Porite is representative of regional specialists that can provide agility and competitive cost structures.

Bound Metal Powders (Burton, MI, USA) — An example of an advanced-materials entrant focusing on binder-jetting powders. As additive manufacturing transitions from prototyping to production for certain sintered components, firms like Bound Metal will be essential partners in qualification and scale-up.

Raw-material shocks: Iron powder prices rose materially in late 2024 amid supply disruptions — a price trajectory that can quickly compress margins without active procurement mitigants. Our modelling shows that volatile powder input costs materially increase break-even payback periods on greenfield sintering lines unless productivity or yield improvements are captured.

Trade and tariff pressure: Persisting import tariffs in key markets raise the cost of cross-border powder flows and create incentives for near-shore production or toll-sintering agreements.

Regulatory tightening: Updated chemical registration requirements in major jurisdictions introduce new testing and impurity-control costs for nickel-containing powders — an area where early compliance planning prevents last-minute supply shortages.

Labor and fixed-cost inflation: Rising labor rates in advanced manufacturing countries increase the premium on automation and yield improvement investments.

Procurement: Build a two-tier hedging strategy. Combine multi-sourcing for critical powder grades with contractual price collars for three- to five-quarter windows. Where possible, secure capacity options at toll-sinterers rather than heavy fixed-capex upfront.

R&D and product development: Co-invest in qualification programs. Prioritize partnerships with powder innovators and additive-specialist powder manufacturers to accelerate e-machine and high-performance part validation.

Manufacturing footprint: Target modularity. Invest in modular sintering cells and automation that allow rapid repurposing between product families to defend against demand shifts.

M&A and JV strategy: Be targeted on capability gaps. Acquire or JV for differentiated powders, binder-jetting competencies, or regional tolling capacity rather than broad geographic consolidation.

Regulatory readiness: Resource a compliance war room. Assign cross-functional teams to track impurity thresholds, testing protocols, and registration timelines to avoid production halts.

Price Shock Scenario: A 15–25% sustained rise in powder input costs compresses margins across commodity parts. Response: convert capex to contract capacity options, increase scrap-reduction investments, and reprioritize higher-margin product lines for production.

Regulatory Tightening Scenario: Faster-than-expected impurity limits for nickel powders lead to a three- to six-month qualification delay for some suppliers. Response: dual-qualify multiple powder grades and secure chemical analytics partnerships to shorten requalification timelines.

EV Acceleration Scenario: Rapid EV adoption increases demand for e-machine components and soft-magnetic composites. Response: fast-track partnerships with soft-magnetic powder suppliers and reallocate plant capacity to support medium-volume, high-margin EV component runs.

Proprietary demand models that translate OEM platform timelines into powder- and component-level demand curves (available in the full report).

Supplier scorecards that synthesize capacity, technology leadership, quality assurance, and commercial flexibility into transaction-ready diligence packs.

Decision templates for CFOs and COOs that put capital, working-capital, and procurement levers into a single sensitivity dashboard for board review.

We have intentionally withheld granular regional and application-level datapoints from this brief to preserve the strategic exclusivity of our full analysis. The full Sintered Steel Market report contains exhaustive regional and application segmentation, pricing and margin matrices, supplier revenues and capacity mapping, and downloadable scenario models that boards and investor committees can use directly in 2026 planning cycles.

For purchasing inquiries, bespoke briefings, or to commission a tailored 2026 playbook based on your company’s position (buyer, supplier, or investor), contact PW Consulting’s Sintered Steel practice. Our clients use the full report to align procurement contracts, capex approvals, and M&A roadmaps with defensible, data-backed scenarios — in short: to move from reactive firefighting to proactive advantage.

For detailed analysis of this topic, please visit the official page:Sintered Steel Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com