Corporate Car-sharing Market Growth Driven by Electric Vehicle Adoption

Literature |

2026-07-03 11:51:18

As electrification initiatives accelerate across transportation, energy and heavy industry, flexible liquid cooled cables have emerged from niche industrial use into a strategic enabling technology for ultra-fast power delivery. PW Consulting’s latest market study — with 2025 as the base year and a detailed forecast to 2032 — shows that the global market is no longer measured in hundreds of millions of dollars of specialized orders but is entering a phase of sustained scale-up. Our model pegs the market at USD 560.0 Million in 2025 and projects a compound annual growth rate of 23.01% through the 2026–2032 forecast window, approaching roughly USD 2.39 Billion by 2032. This trajectory creates a distinct set of strategic decisions that corporate leaders will confront in 2026.

Flexible Liquid Cooled Cable Market

Technology convergence: Liquid cooling has moved beyond custom induction-furnace leads and battery-cell test benches into megawatt-class EV charging, data-center power delivery and advanced industrial electrification. The shift from bespoke supply to platform-enabled products is underway, altering procurement, service and aftermarket economics.

Flexible Liquid Cooled Cable Market

Regulatory and standards inflection: Safety and interoperability standards have tightened for high-voltage, high-current systems. Recent UL milestones for megawatt liquid-cooling systems and the continued dominance of IEC/ISO requirements mean product roadmaps and compliance programs must be synchronized from R&D to field operations.

Flexible Liquid Cooled Cable Market

Scale and concentration dynamics: The market is still moderately concentrated — our concentration metrics indicate meaningful leadership among a small group of suppliers, but not prohibitive dominance. That structure favors strategic partnerships, co-development agreements and selective M&A as viable routes for fast followers.

PW Consulting’s Flexible Liquid Cooled Cable Market report was designed to be operationally useful for senior executives, commercial leads, and engineering decision-makers. The study offers:

Proprietary market sizing and demand scenarios calibrated to 2020–2025 historical performance and our 2026–2032 forecast. Growth scenarios dissect installed-base replacement cycles, first-fit infrastructure deployments, and incremental demand from new megawatt EV projects.

Technology deep dives that translate materials science and thermal-hydraulic performance into procurement specifications: conductor metallurgy, hose and insulation choices, coolant chemistries, and manufacturability trade-offs.

Regulatory and standards matrix mapping applicable IEC, UL and ISO requirements to product design checkpoints and validation test plans, reducing time-to-compliance risks.

Competitive benchmarking and capability heatmaps that profile manufacturers across design, production capacity, customization, testing capabilities, and channel strength — intended to support sourcing, alliance and M&A diligence.

Commercial playbooks covering pricing models, aftermarket service contracts, field-reliability KPIs and warranty frameworks specifically tailored to high-current liquid-cooled deployments.

Supply-chain and raw-material sensitivity analyses that quantify exposure to copper pricing, lead times for specialized tubing and coolant systems, and mitigation levers such as strategic stocking or vertical integration.

Implementation roadmaps for OEMs, fleet operators, charging-network developers and data-center operators outlining short-, medium- and long-term procurement and engineering milestones to capture upgrading opportunities.

The ecosystem encompasses a mix of specialist fabricators, component-focused incumbents and system integrators. Our qualitative assessment of leading participants highlights three archetypes:

Specialist fabricators with deep application know-how — companies that excel in tailored water-cooled leads for induction and furnace applications. Their strengths are customization, rapid retrofit services and field-proven designs.

Platform innovators targeting EV ultrafast charging — firms that invest in integrated cable-and-connector platforms to deliver ergonomic, high-throughput systems for public and commercial charging deployments.

Scale manufacturers and materials specialists — players that can bring high-conductivity copper, advanced insulation and standardized manufacturing to bear, enabling cost and reliability advantages as volumes increase.

Representative players across these archetypes include established custom fabricators known for water-cooled leads and high-current flex cables, alongside European and North American manufacturers advancing direct liquid-cooled HV offerings for high-power EV charging. Recent market activity — from new product launches and catalog refreshes to field demonstrations of megawatt-class charging — illustrates how these archetypes are converging around common technical and commercial requirements.

Product integrations and ecosystem plays are intensifying. Notable integrations of high-current liquid-cooled CCS cable-and-connector solutions into charger platforms signal that system-level partnerships are becoming a de facto route to market for fast-charging infrastructure.

Field deployments of multi-hundred-kilowatt and megawatt-station prototypes have moved from lab demonstrations to live-site charging, validating user ergonomics, cooling strategies and maintenance protocols under operational stress.

Manufacturers continue to update product catalogs with faster delivery promises and optional safety features, reflecting an industry transitioning from bespoke build-to-order to scaled configurable platforms.

Standards and certifications are emerging as competitive moats. Early recipients of high-power UL certifications have a pathway to easier commercial acceptance among risk-averse buyers.

To convert market momentum into durable advantage, organizations should prioritize the following actions in 2026:

Align product and compliance roadmaps. Map product development milestones to evolving standards and certification milestones to avoid late-stage redesigns. Shortlist certification bodies and accelerate testing pipelines as early procurement and pilot programs scale.

Adopt a multi-path sourcing strategy. Balance engagement with specialist fabricators for custom applications and platform suppliers for standardized charging products. Structured supplier scorecards should incorporate manufacturability, testing capability, lead time, and field-support readiness.

Invest in modular product architectures. Design cable-and-coolant systems for interchangeability across charger and industrial platforms to lower SKU proliferation while preserving application-specific performance.

Mitigate supply-chain risk on copper and critical components. Run scenario analyses that quantify cost and lead-time exposure across alternative conductor grades and supplier geographies, and consider strategic inventory postures for ramp years.

Develop field-service and warranty economics. High-power systems will generate new maintenance regimes; firms that define clear service-levels, predictive-replacement thresholds, and spare-part strategies will reduce unplanned downtime for customers and capture aftermarket revenue.

Explore targeted partnerships and M&A. Given the market’s moderate concentration and rapid growth, partnerships for channel access, thermal-management IP or manufacturing capacity can accelerate go-to-market while de‑risking greenfield investments.

Prioritize human factors and ergonomics. As cables become the user interface for gigawatt-scale charging, cable weight, grip comfort, and thermal presentation will determine customer satisfaction and adoption rates.

Three demand vectors will dominate procurement conversations in the next 12–24 months:

Megawatt-class EV charging: Operators and OEMs will seek systems that deliver sustained high currents while remaining manageable for everyday users and maintainable over lifecycle horizons.

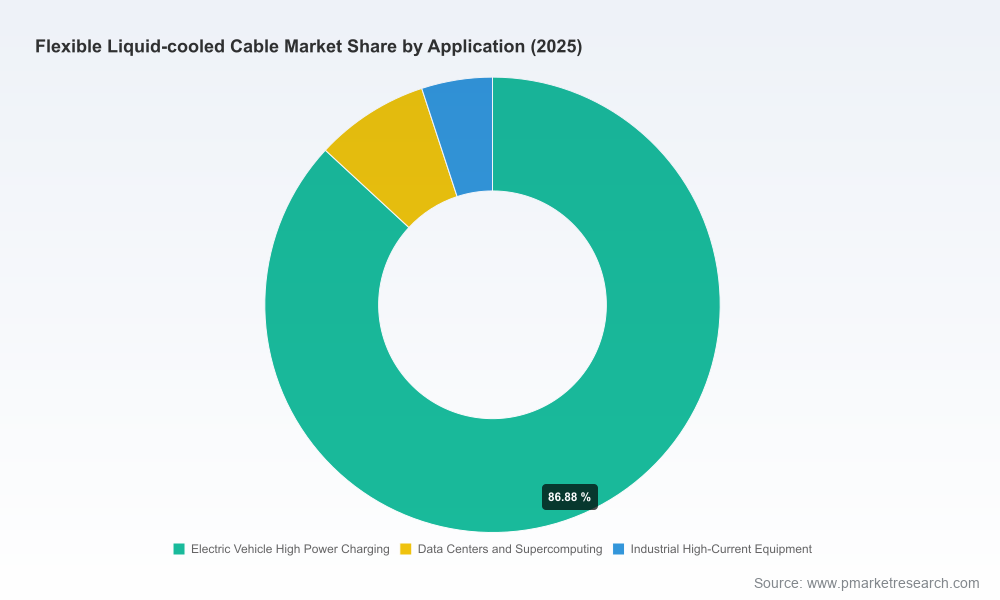

Data-center and HPC power delivery: Liquid-cooled flexible cables can enable compact high-density power distribution where thermal budgets are constrained.

Industrial high-current electrification: Heavy industry replacement of legacy buswork with flexible liquid-cooled leads will be driven by uptime and retrofit convenience.

PW Consulting’s scenarios differentiate between first-adopter pilot waves and mainstream commercial rollouts, identifying the inflection points when procurement transitions from engineering buys to operationalized purchasing decisions.

This briefing is intended as a strategic preview: it explains structural drivers, competitive dynamics and the core implications for 2026 decision-makers. The full PW Consulting report contains granular, actionable intelligence we deliberately withhold here to preserve its transactional value — including detailed segment-level demand matrices, supplier share estimates, regional roll-out timetables, and quantitative sensitivity models for raw-material price shocks and certification timelines. These elements are essential for procurement tenders, capex approvals and M&A valuation workstreams.

As the flexible liquid-cooled cable market scales, enterprises must treat it as a strategic system component rather than a commodity cable purchase. In practice that means integrating thermal and electrical specification disciplines into systems engineering, building certification roadmaps into product release plans, and crafting supplier relationships that secure both technology differentiation and manufacturing throughput. With a market expanding at north of 20% annually over the coming years, the cost of delay will be measured not just in price but in lost access to preferred platform suppliers, delayed certifications, and higher field-maintenance exposure.

For teams preparing 2026 budgets, PW Consulting recommends a phased investment posture: fund compliance and pilot deployments this year, secure supplier options and pilot-service agreements, then scale manufacturing and field-support investments as the market crosses its commercialization inflection. The full report provides the decision-grade schedules, RFP templates, and supplier shortlists needed to execute this plan with confidence.

To access the complete analysis, proprietary data tables, and operational toolkits referenced in this preview, please download the full Flexible Liquid Cooled Cable Market report from our website or contact PW Consulting’s sector team to schedule a briefing. Our analysts stand ready to translate these findings into bespoke roadmaps tailored to your functional priorities and risk tolerance.

For detailed analysis of this topic, please visit the official page:Flexible Liquid Cooled Cable Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com