Cast Saw Devices Market Growth Supported by Increasing Fracture Incidence Worldwide

Health |

2026-06-02 14:04:28

PW Consulting’s Scar Tape Market report (base year 2025, historical 2020–2025, forecast 2026–2032) delivers an evidence-based roadmap for executives shaping product, commercial, and M&A strategies in a category poised for steady expansion. Our analysis shows the addressable market advancing from an evaluated USD 215.0 Million in 2025 to an estimated USD 348.62 Million by 2032, representing a compound annual growth rate (CAGR) of 7.15% over the forecast horizon. This release is designed as a strategic “trailer”: it surfaces the essential macro dynamics, competitive posture, regulatory context, and pragmatic playbooks you need to set 2026 priorities — while reserving the granular segment tables and proprietary benchmarking for subscribers and report purchasers.

Scar Tape Market

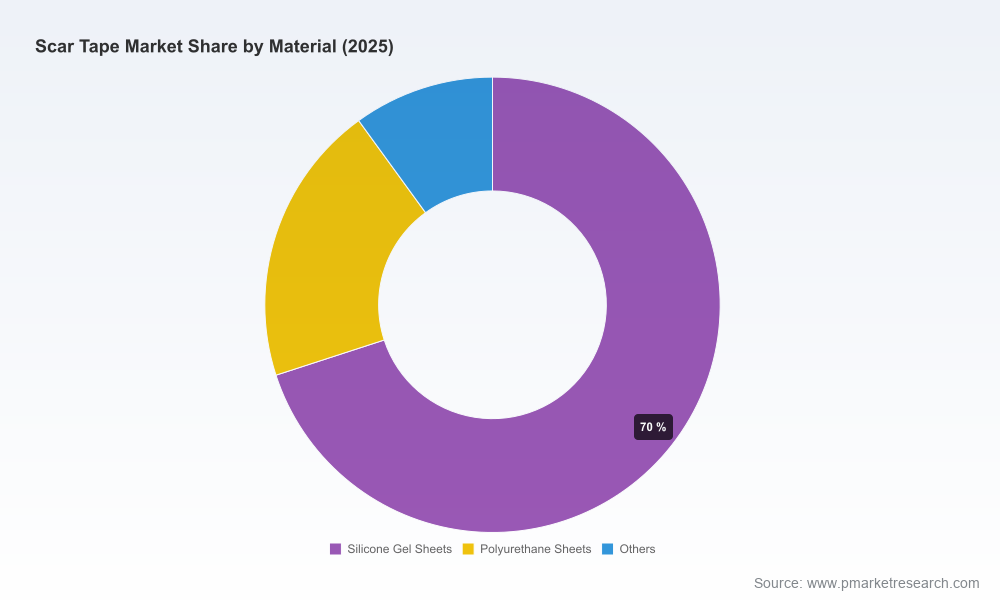

Clinical first-line positioning: Medical-grade silicone sheeting and adhesive systems continue to be recommended as non-invasive first-line therapy for hypertrophic and keloid scars. That enduring clinical endorsement underpins predictable demand streams across surgical aftercare, dermatology, and aesthetic segments.

Scar Tape Market

Commercial resilience: Stable clinical guidance, greater consumer willingness to invest in scar mitigation, and growing adoption in post-procedure protocols combine to create resilient revenue growth even as elective-care cycles fluctuate.

Scar Tape Market

Innovation vectors: Material science (silicones and substrates), wearable comfort, and integration with adjunctive energy- or drug-based modalities open pathways for premiumization and differentiated propositions.

Between 2020 and 2025 the Scar Tape category matured from early adoption into a well-established therapeutic niche with expanding clinical acceptance. Our top-line sizing captures that transition, with 2025 as the report’s base year and a modeled expansion driven by three structural forces: increased procedural volumes in reconstructive and cosmetic surgery globally; broader adoption of evidence-based post-op protocols; and product innovation improving patient compliance and reusability.

The predicted 7.15% CAGR to 2032 is not a forecast of uniform growth — it is the aggregate result of heterogeneous demand across clinical and consumer channels, pricing tiers, and product formats. Market concentration metrics indicate a moderately consolidated supplier landscape, where global incumbents coexist with a growing roster of specialized challengers and regional producers. That structure creates distinct strategic choices for incumbents, new entrants, and private equity buyers alike.

Regulatory classification: Silicone sheeting for scar management is generally regulated as a Class I medical device under key jurisdictions, which reduces regulatory barriers to market entry compared with higher-risk implantable technologies. Understanding the limits and opportunities of this classification is essential for lifecycle planning and market access.

Clinical mechanism and standard of care: The semi-occlusive effect of silicone sheets — regulating hydration and collagen deposition — remains the clinical rationale for their first-line use. That established mechanism supports stable adoption and provides a defensible clinical message for marketing, but it also raises the bar for demonstrable incremental benefits when pursuing premium pricing.

Adjunct innovations: Energy-based and combination therapies are converging with topical and device-based scar management. Notably, recent clearances in related scar treatment technologies highlight an expanding ecosystem of complementary interventions. Strategic partners and product roadmaps should account for integration opportunities rather than seeing those developments solely as competitive threats.

The category’s commercial architecture blends legacy medtech players with niche specialists focused exclusively on silicone scar care. Key market actors demonstrate distinct strategic postures you should benchmark against:

Mölnlycke Health Care AB — A heritage medical products company leveraging proprietary adhesion technologies to position reusable, patient-friendly silicone solutions for hypertrophic and keloid scars.

Smith & Nephew plc — Global footprint and established clinical channels allow premiumized silicone sheeting brands to scale across professional and consumer settings.

Biodermis — A U.S.-based specialist that targets both clinical and consumer use-cases with a product mix engineered for different anatomical challenges and surgical indications.

NewGel+ (Newmedical Technology) — Focuses on advanced medical-grade silicone formulations and claims around wearability and clinical efficacy for surgery, burns, and trauma.

Perrigo / ScarAway — Leverages established consumer channels and brand recognition to capture retail and OTC demand with sheet and tape variants.

Neodyne Biosciences (Embrace) — Technology-oriented proposition emphasizing stress-mitigation and active defense for new scars; an example of how differentiation can be engineered through design and claims.

For corporate strategists, the takeaway is straightforward: incumbent scale confers distribution advantages and clinical trust, but smaller, focused innovators are sources of product differentiation and acquisition opportunity. Our market concentration analysis — included in the full report — quantifies this balance and identifies where scale and specialty deliver the highest return on investment.

PW Consulting’s report is built for decision-makers. It goes beyond descriptive market commentary to provide operationally useful intelligence for 2026 planning cycles:

Top-line sizing and a transparent forecast model (2026–2032) with scenario sensitivity to procedural volumes, pricing, and adoption curves.

Competitive playbooks and company scorecards that evaluate R&D pipelines, channel strength, pricing strategies, and partnership fit.

Go-to-market templates for clinical, retail, and digital channels, including conversion metrics, promotional levers, and channel conflict mitigations.

Regulatory and reimbursement mapping that translates device classifications into practical market access timelines and compliance checklists.

Product roadmaps and R&D prioritization matrices aligning material innovation, wearability, and claims architecture to willingness-to-pay segments.

M&A and partnership targets with financial benchmarks and integration risk assessments to guide diligence and valuation negotiation.

Risk heatmaps and mitigation playbooks addressing supply-chain volatility, raw-material substitution, and IP exposure.

Our research crystallizes several actionable choices for different corporate archetypes in 2026:

For incumbents: double down on channel harmonization and outcomes data. Invest in real-world evidence studies that link scar product use to post-op recovery metrics valued by hospitals and payors. This supports premiumization and defends share against lower-cost entrants.

For product innovators and SMEs: prioritize clinical differentiation that is both defensible and scalable — e.g., materials that materially improve wear-time comfort or demonstrably enhance adherence without triggering new regulatory classification hurdles.

For private equity and corporate M&A teams: target bolt-on opportunities that provide distribution or R&D lift rather than broad geographic scale alone. Our scenario models show acquisition multiples compress when product pipelines are weak or channel access is limited.

For retail and e-commerce strategists: optimize the digital funnel for high-consideration medical consumables by pairing education-heavy content with conversion experiments; patient confidence and repeat-purchase drivers are central to lifetime value.

Blended channels: Effective commercialization increasingly requires a hybrid approach that aligns clinical endorsement with direct-to-consumer education and retail availability.

Subscription and reusable models: Given the reusability profile of many silicone sheeting products, subscription and replenishment models can unlock predictable revenue and higher lifetime value.

Quality and sustainability claims: Material provenance and clinical-grade manufacturing are differentiators; sustainability messaging — without undermining clinical credibility — can open new consumer segments.

Maintaining regulatory vigilance is table stakes. Silicone sheeting’s Class I status streamlines some pathways, but claims substantiation remains rigorously enforced. Additionally, advances in complementary therapies (for example, recent clearances of energy-based platforms for scar indications) expand the ecosystem and create partnership opportunities. Our analysts track these adjacent approvals and provide scenario analyses that quantify their potential to displace or augment silicone-based interventions.

Use the report for three immediate planning tasks:

Portfolio triage — identify which SKUs to accelerate, which to sunset, and where to invest to close clinically meaningful gaps.

Commercial playbook — build a 12–24 month channel and marketing plan tied to the forecast scenarios and conversion benchmarks we provide.

Diligence and M&A screening — apply our acquisition scorecards and integration playbooks to prioritize targets and structure conditional earn-outs linked to clinical and commercial milestones.

The report’s base year is 2025, with historical context from 2020 through 2025 and forecasts from 2026 to 2032. Our approach combines primary interviews with clinicians, purchasing managers, and category leaders; proprietary shipment and revenue models; and secondary sources including regulatory classifications and clinical literature. Scenario analysis is provided to stress-test demand under alternative assumptions for procedure volumes, pricing pressure, and channel mix.

This release is intentionally selective: it surfaces the strategic imperatives and high-level sizing that executives must consider in 2026 while reserving the detailed segmentation tables, regional and application-level splits, and vendor-by-vendor financial benchmarks for the full report. To access the complete dataset, downloadable models, and bespoke advisory options (including a two-hour strategy briefing with our senior analysts), please visit PW Consulting’s Scar Tape Market report page or contact our commercial team for licensing and enterprise access.

PW Consulting’s Scar Tape Market report is designed to convert insight into action. If your 2026 plan depends on credible forecasts, defensible valuations, or a playbook for winning in a clinically anchored, consumer-facing medical category — this is the intelligence you should build your plan around.

For detailed analysis of this topic, please visit the official page:Scar Tape Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com