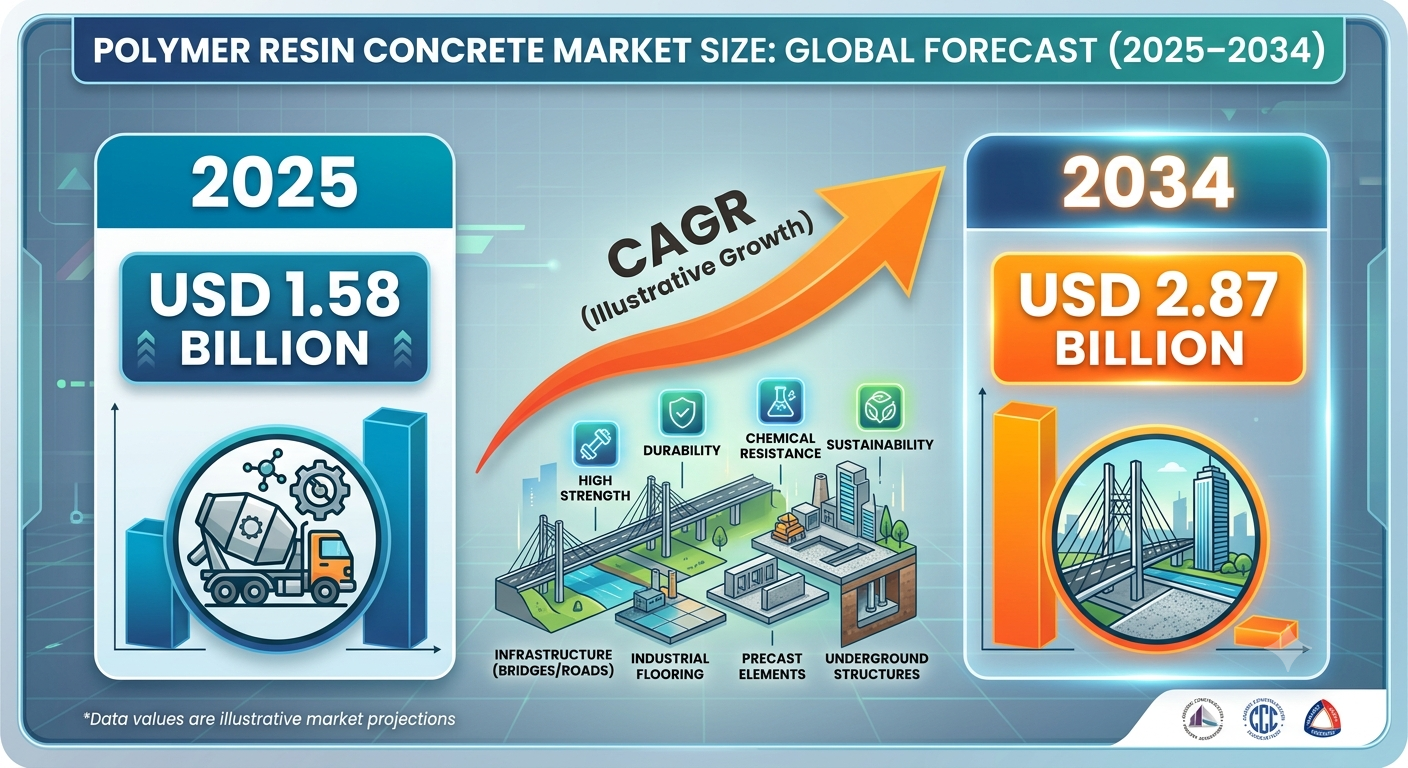

Polymer Resin Concrete Market Size to Expand from USD 1.58 Billion in 2025 to USD 2.87 Billion by 2034

Other |

2026-06-02 10:22:59

As fertility care moves from niche specialty clinics to mainstream health systems, corporate leaders face a converging set of commercial, regulatory and manufacturing pressures. PW Consulting’s new Fertility Drugs Market study — anchored on a 2025 base year and covering historical performance (2020–2025) with a forward-looking forecast to 2032 — translates those pressures into a set of actionable insights for 2026 decision-making. The global infertility drugs market expanded from roughly USD 3.95 billion in 2020 to about USD 5.32 billion in 2025 and, at a compound annual growth rate of 6.1%, is projected to approach the mid‑single‑digit billions by 2032. This growth backdrop creates both opportunities and vulnerabilities for branded manufacturers, biosimilar entrants, generics suppliers and clinical service providers.

Fertility Drugs Market

Transition from protection to competition: The coming 18–36 months will see an acceleration of generics and biosimilars entering fertility drug formularies, prompting pricing pressure on legacy biologics and branded injectables. Companies that remain reactive risk margin erosion; those that reposition now can capture volume, access and long-term loyalty.

Fertility Drugs Market

Policy and procurement shocks: Recent policy signals and regulatory updates have made payer and government procurement behavior less predictable. An emergent direct‑to‑consumer pricing initiative and public sector interest in cost containment make proactive access strategies essential.

Fertility Drugs Market

Supply chain and availability risk: Episodic shortages of key gonadotropin products have already affected clinical throughput in some markets. Firms that secure redundant supply lines and manufacture-critical-path biologics will have a distinct competitive edge.

Market momentum: The market’s multi‑year expansion through 2025, and our forecast growth through 2032 at a ~6.1% CAGR, is driven by a mix of rising demand for assisted reproductive technologies (ART), demographic trends, and increased treatment accessibility in emerging markets.

Concentration and contestability: The fertility drugs market exhibits a high degree of concentration among established specialty and pharma players; however, contestability is rapidly increasing as lower‑cost generics and biosimilars scale manufacturing and distribution.

Price vs. access tension: Stakeholders are navigating a clear trade‑off: tighter pricing corridors can broaden patient access but also compress manufacturer economics—shifting the commercial focus toward volume-based and value‑based contracting models.

Robust market sizing and forecasts: Year‑by‑year market estimates (historical and forecast) across the 2020–2032 window, including sensitivity scenarios for regulatory and supply shocks.

Granular go‑to‑market playbooks: Tailored commercial blueprints for branded biologics, biosimilars, and generics — covering pricing, channel strategy (clinic partnerships, specialty distributors, DTC models), and product launch sequencing.

Regulatory and patent landscape mapping: Timelines of exclusivity expiries, biosimilar approval pathways, and jurisdictional regulatory nuances that materially affect launch timing and market access.

Supply chain and manufacturing analysis: End‑to‑end risk mapping for biologics, recommended contingency investments, and near‑term capacity requirements for recombinant FSH and other high‑volume agents.

M&A and partnership target shortlists: Quantified opportunity cases for acquiring or partnering with regional manufacturers, biosimilar developers and clinic networks to secure demand and distribution.

Commercial diligence tools: Revenue projection templates, payor negotiation playbooks, and a checklist for pricing, contracting and rebate mechanics under emerging reimbursement regimes.

The competitive field is a mix of global incumbents with deep fertility portfolios, multinational generics houses, regional manufacturers and focused biotech players pursuing biosimilar recombinant gonadotropins. Key archetypes and strategic imperatives:

Branded biologics leaders (e.g., legacy specialty pharma): Maintain clinical differentiators (formulation, delivery convenience, clinician support programs) while preparing for share erosion. Consider strategic price/volume agreements, subscription models with major clinics, and investments in patient support to defend premium positioning.

Biosimilar and generic entrants: Scale manufacturing and regulatory programs rapidly, but prioritize selective market entry where reimbursement and clinic adoption can be unlocked via lower cost and supply reliability. Co‑development or co‑supply agreements with IVF networks will accelerate uptake.

Regional players and contract manufacturers: These firms can win on affordability and localized market knowledge. Global firms should evaluate bolt‑on acquisitions or long‑term supply partnerships to secure footprint and cost advantages.

Platform and service integrators: Firms that combine drug supply with clinical service platforms, digital patient engagement, and fertility financing can capture disproportionate lifetime value.

Generic launches: The market has seen new generic introductions for classic ovulation inducers, expanding affordable access and pressuring branded volumes. For companies holding branded equivalents, this mandates rapid lifecycle planning (label enhancements, service bundling, or line‑extensions).

Shortage events: Regulatory updates documenting shortages of essential gonadotropin products highlight fragility in the biologics supply chain. Firms must prioritize inventory management, contract manufacturing diversification and onshore buffer capacity to mitigate clinician and patient disruption.

Pipeline and R&D shifts: Expansion of biosimilar FSH programs and generics for antagonist agents are reshaping future competition; early mover positioning on biosimilars delivers commercial leverage when coupled with clinic partnerships.

Policy signals: Governmental and payer initiatives targeting IVF drug pricing and novel procurement routes create upside for low‑cost suppliers but raise commercial complexity for branded manufacturers. Anticipatory pricing strategies and public tender playbooks are now essential.

Reassess portfolio segmentation: Conduct rapid portfolio triage by margin, strategic fit and defendability. Prioritize investment in products with clear clinical differentiation or where supply reliability can be a durable competitive advantage.

Lock in supply resilience: Allocate capex or strategic M&A capacity to secure biologics manufacturing, GMP fill/finish partners and regional buffer inventories for key hormones and gonadotropins.

Build biosimilar readiness: If pursuing biosimilars, fast‑track regulatory dossiers, secure clinical comparability strategies and pre‑negotiate supply to major ART networks to accelerate uptake post-approval.

Deploy hybrid commercial models: Experiment with bundled clinic contracts, outcome‑based arrangements, and DTC pricing pilots where regulations allow. Use pilots to prove value to payers and clinics before scaling.

Prepare for policy volatility: Model aggressive pricing and tender scenarios. Design payer negotiation strategies that preserve core margins via non‑price value (training, adherence tools, patient financing).

Pursue strategic partnerships: For multinational players, selective alliances with regional manufacturers and specialty distributors can offer immediate access, local regulatory know‑how and cost advantages.

Our Fertility Drugs Market report is not just a numbers exercise — it is a practical playbook. PW Consulting offers bespoke services that translate this analysis into executable plans: commercial due diligence for M&A, market access and pricing playbooks, supply chain audits and biologics manufacturing advisory, and tailored payer engagement strategies. Clients receive scenario models calibrated to their portfolio and bespoke risk registers to guide board-level decisions.

This article highlights the strategic contours and immediate priorities that should drive executive attention in 2026. To preserve the integrity of our market models and to support confidential decision processes, detailed segmentation breakouts, price grids, and the full competitive scorecards are available through the full report portal. PW Consulting’s Fertility Drugs Market report provides the granular data, revenue-level segmentation and company-level forecasts needed for transaction diligence and commercial planning.

Contact PW Consulting to request the full report, a tailored executive briefing, or a workshop to translate these findings into an operational plan tailored to your organization’s risk profile and strategic aspirations.

For detailed analysis of this topic, please visit the official page:Fertility Drugs Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com