Molecular Blood Typing, Grouping and Infectious Disease NAT Market

Other |

2026-06-23 06:05:57

As PW Consulting’s Lead Industry Analyst, I present a focused strategic briefing derived from our comprehensive Nickel Boride Alloy Market study. This note is designed as a high-value prelude for executives making resource allocation, sourcing, and M&A decisions during 2026. We reveal the directional conclusions, scenario-driven implications, and tactical recommendations you can act on immediately — while preserving the granular segment-level data and proprietary models that are available in the full report.

Nickel Boride Alloy Market

Key macro picture: the Nickel Boride alloy market is entering a sustained growth phase. Using 2025 as the analytical base year, our forecast through 2032 projects a compound annual growth rate of approximately 5.48%. In nominal terms, the global market expands noticeably over the forecast window, reflecting steady demand across catalysts, wear-resistant coatings, brazing alloys and semiconductor-related applications.

Nickel Boride Alloy Market

Why this matters now: 2026 is a pivot year for strategic repositioning. The growth is broad-based but not uniform; supply-side constraints, raw material volatility, and regulatory dynamics are reshaping competitive advantage. Firms that translate macro momentum into resilient value chains and differentiated product offers will capture disproportionate share of the upside.

Nickel Boride Alloy Market

Raw-material volatility: Nickel pricing remains a leading cost driver. As of late April 2026, nickel prices hovered near USD 19,457 per tonne, reflecting a significant year-over-year rise. That level of volatility compresses margins for pure-play producers and elevates the importance of hedging, long-term contracts, and alternative sourcing strategies.

Policy and trade levers: Export restrictions and strategic controls in the nickel value chain — notably measures implemented by key producing jurisdictions — continue to affect the flow of upstream feedstock and intermediate alloys. These policy levers can materially alter lead times and the economics of cross-border supply networks.

Downstream demand diversification: Demand growth is being supported by catalysts and wear-resistant coating applications, while semiconductor and advanced brazing uses provide strategic adjacency opportunities. The end-market mix matters: product-form selection (powder, targets, ingots/granules) and specification capability determine who captures higher-margin segments.

Consolidation dynamics: The market exhibits moderate concentration among a handful of established suppliers, but fragmentation persists at the regional and specialty-product level. This structure enables targeted M&A and partnership plays that rapidly scale technical capability and geographic reach.

Our full report is built for operators and strategists who must translate market intelligence into executable plans. Highlights of practical deliverables include:

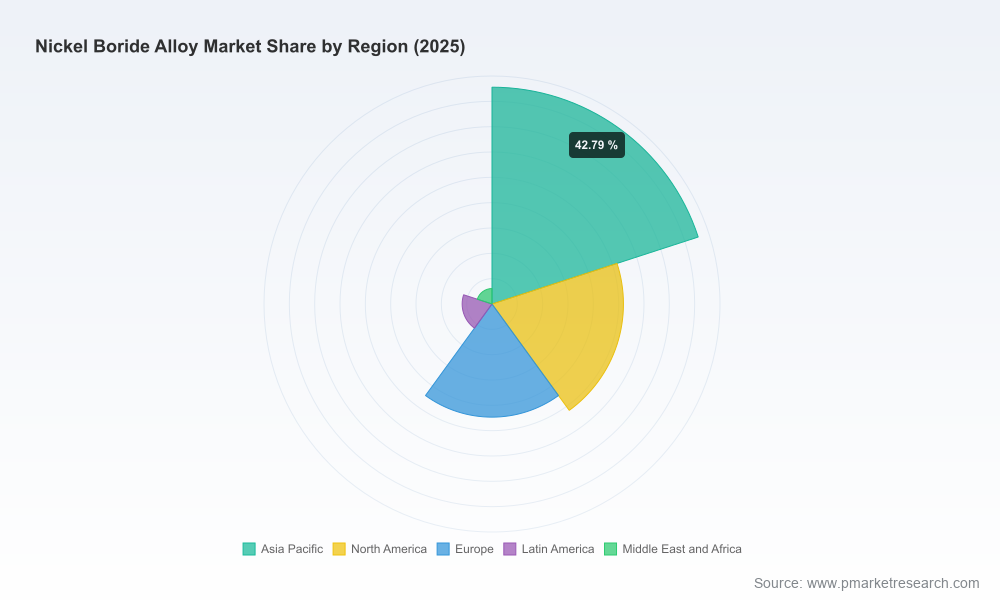

We deliberately stop short of publishing full segment allocations and precise regional revenue splits in this briefing; those elements are included in the report’s proprietary datasets and dashboards, which are essential for transaction-level work and operational planning.

The market is populated by a mix of global specialty materials firms, regional producers, and niche catalyst houses. Below we summarize the strategic positioning of the core players we profiled — the intention is to orient executives to possible partners, competitors, and acquisition targets rather than to replace the full competitive matrix in the report.

American Elements (US) — Strength: recognized capability in high-purity NiB chemistries across multiple stoichiometries and forms. Strategic relevance: premium research and advanced-materials applications; attractive partner for co-development where purity and specification control are priorities.

Stanford Advanced Materials (SAM, US) — Strength: broad product portfolio including evaporation materials and boride compounds. Strategic relevance: well-suited for customers needing rapid prototyping and small-batch speciality supplies; a potential bolt-on for firms expanding into R&D-focused offerings.

KBM Affilips (Netherlands) — Strength: master-alloy formulations for metallurgical applications. Strategic relevance: an important upstream supplier for superalloy and wear-resistant-steel manufacturers seeking controlled boron additions.

Westbrook Resources (UK) — Strength: niche expertise in NiB master alloys and hard-facing inputs. Strategic relevance: options for industrial-scale metallurgy partnerships and offtake agreements in heavy engineering sectors.

Luoyang Golden Egret & Huarui Metal & Xinglu Chemical (China) — Strengths: scale in powder manufacturing and thermal-spray applications, proximity to large regional demand pools. Strategic relevance: low-cost sourcing options, but require careful due diligence on quality consistency, export controls, and supply-chain resilience.

ESPI Metals (US) — Strength: supply of specific Ni2B grades for specialized requirements. Strategic relevance: supplier of choice for precision applications and small-batch specialty needs.

PTG Advanced Catalysts (China) — Strength: focus on catalyst-grade NiB for chemical processing and hydrogenation. Strategic relevance: candidate for co-development in catalyst optimization and scale-up for industrial chemical producers.

Collectively, this set of firms illustrates the spectrum from premium, specification-driven suppliers to higher-volume, cost-focused producers. The right partner depends on the buyer’s priorities — cost, specification, lead-time, or regulatory certainty.

Baseline (most probable): steady mid-single-digit CAGR, continued pressure on margins from raw-material cost inflation, but offset by rising demand in coatings and catalysts. Strategic action: selective price pass-throughs, tighter supplier SRM, and prioritization of higher-margin product forms.

Supply-constrained upside: tighter ore controls and concentrated upstream supply push premium pricing higher, creating pockets of outsized margin for vertically integrated players. Strategic action: pursue vertical integration or exclusive offtake contracts; accelerate capacity investments where ROI supports pricing power.

Policy shock downside: abrupt trade restrictions or dual-use controls amplify delivery risk and create compliance burdens. Strategic action: diversify sourcing by jurisdiction, increase onshore inventory buffers, and implement compliance playbooks to avoid disruptive supply interruptions.

Leading indicators to monitor in 2026: nickel spot and forward curves, policy announcements from resource-exporting nations, shipments to semiconductor fabs and catalyst converters, and announcement of new large-volume contracts or capacity expansions by key producers.

Producers: refine product mix towards higher-spec forms where technical barriers reduce commoditization risk; lock in supply via multi-year contracts indexed to appropriate benchmarks; and accelerate downstream offerings (coatings/catalysts) to climb the value chain.

Buyers / OEMs: establish dual-sourcing strategies segmented by application criticality; embed supply covenants in contracts; and run joint-development programs with specialist suppliers to reduce specification risk and shorten qualification cycles.

Private equity / strategic investors: prioritize targets that combine technical IP with scale advantages or route-to-market synergies; focus due diligence on feedstock security, regulatory exposure, and product traceability.

Procurement / risk teams: implement dynamic hedging and inventory optimization that reflect scenario thresholds; operationalize a supplier early-warning dashboard tied to price, lead-time, and policy signals.

The published report is more than a market narrative — it is a toolkit for immediate execution. Subscribers receive the complete datasets (including the segmented revenue matrices and regional demand models), interactive scenario workbooks, and supplier-ranking templates. These resources have been designed to plug directly into capital planning and procurement processes, shortening the decision cycle from insight to implementation.

If your 2026 plan includes capex decisions, supplier restructuring, M&A screening, or a procurement revamp related to nickel-containing alloys, this study contains the calibrated inputs and playbooks you need. For access to the full report, detailed segment-level models, and bespoke advisory support, please visit PW Consulting’s Nickel Boride Alloy Market page or contact our lead analysts directly. Our advisory teams are standing by to run customized scenario workshops and supplier due diligence for immediate strategic deployment.

PW Consulting — helping leaders turn material-market complexity into clear competitive advantage for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Nickel Boride Alloy Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com