オンラインカジノの時代 – 未来はすでにここに

Sports |

2026-05-01 13:03:39

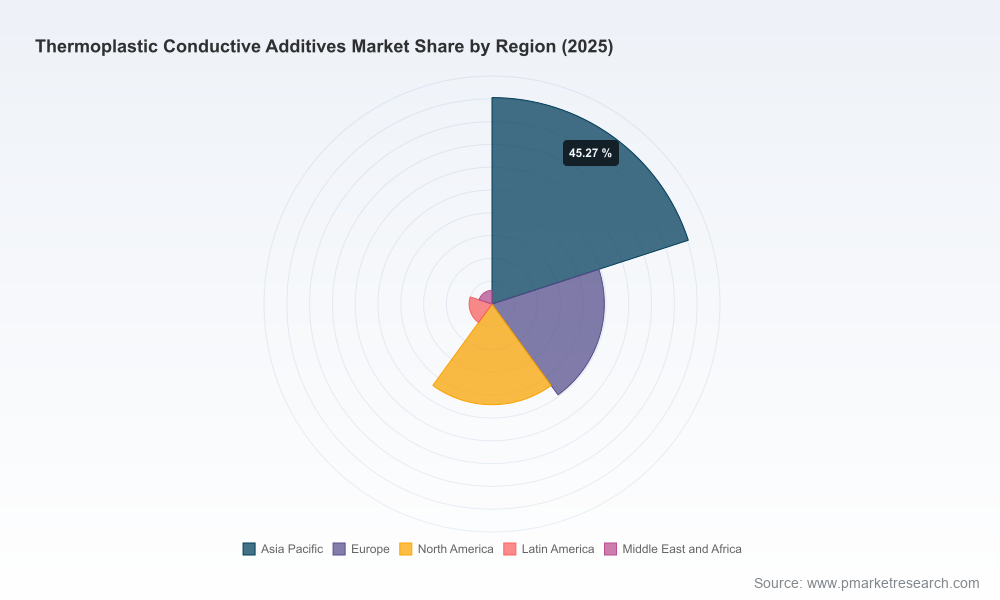

PW Consulting’s new Thermoplastic Conductive Additives Market report (base year 2025) is designed as an operational playbook for executives, product leaders and procurement teams planning for 2026 and beyond. The global market for conductive additives in thermoplastics has reached a meaningful scale — roughly USD 2.52 billion in 2025 — and is projected to expand at a compound annual growth rate (CAGR) of 9.42% through our 2026–2032 forecast window. By 2032, modeled market value approaches USD 4.73 billion under our base scenario. These headline metrics underline why conductive additives are becoming a strategic input across electrification, miniaturized electronics, advanced packaging and thermal management agendas.

Thermoplastic Conductive Additives Market

Actionable sizing and trajectory: We translate the headline CAGR into pragmatic roll‑up scenarios (conservative / base / aggressive) that quantify addressable volumes for materials, compounds and finished‑part suppliers across strategic timelines.

Thermoplastic Conductive Additives Market

Decisions, not dashboards: The analysis is oriented toward decision points — vendor selection, capex timing, qualification roadmaps, and partnership models — rather than academic segmentation alone.

Thermoplastic Conductive Additives Market

Risk‑adjusted procurement: The report connects raw‑material dynamics and concentration risks to procurement levers, enabling teams to move from reactive buying to strategic contracting in 2026.

Electrification and EMI/ESD needs: Continued growth in electric vehicles, industrial electrification and higher‑frequency consumer electronics is driving demand for both electrically and thermally conductive thermoplastic solutions. Manufacturers seek materials that are processable at commercial throughputs while meeting conductivity and mechanical targets.

Thermal management as a product differentiator: As power densities rise, thermally conductive additives are being specified earlier in the design cycle. This shifts value capture upstream toward compounders and additive formulators who can balance conductivity with weight and appearance requirements.

Feedstock and pricing pressure: Carbon black — a dominant feedstock for many conductive masterbatches and compounds — is experiencing upward pricing pressure in North America (price observations in early 2026 indicate levels around USD 2.03/kg), a factor that tightens margins and forces formulation innovation or rebadging strategies.

Supply and capacity evolution for advanced additives: Carbon nanotubes and graphene are moving from pilot to incrementally larger commercial capacity; industry estimates place the near‑term carbon nanotube market entry value around the low‑billion USD region, prompting compounders to evaluate low‑loading, high‑performance formulations.

Regulatory watch: Chemical evaluations scheduled in some jurisdictions (e.g., a 2027 European review of carbon black classification) create program risk for players dependent on single additive chemistries — an input to sourcing and R&D planning for 2026.

Topline market sizing and three scenario forecasts to 2032, calibrated to raw‑material and end‑market demand drivers.

Supplier capability matrix and qualitative scorecards covering formulation breadth, scale, geographic footprint, and qualification lead times.

Technology readiness assessment that ranks additive families by cost‑to‑benefit for common thermoplastic matrices, and pathways to low‑loading/low‑impact integration.

Procurement playbook: tender language, specification checklists, phased qualification milestones and sample contract clauses to manage supply risk and IP exposure.

Commercial use‑cases and case studies: injection molded, extruded and compounder‑scale examples that link material choice to manufacturability and lifecycle cost.

Financial impact models: scenario tools to stress test margin sensitivity against feedstock price moves, capacity constraints and demand shocks.

The market is moderately concentrated: the top three players account for a meaningful portion of supply while the top five broaden control further, leaving room for specialized players and targeted entrants. This structure favors focused differentiation — e.g., proprietary low‑loading nanotube concentrates, high‑throughput graphite powders, or stainless steel fiber fillers for niche EMI shielding — over undifferentiated scale plays alone.

Cabot Corporation (Boston, MA) — deep carbon black and masterbatch capability, strong in static dissipation and cable/electronics channels. Strategic clients will continue to lean on Cabot’s scale and application labs for qualification speed.

Avient Corporation (Avon Lake, OH) — compounder strength with thermally and electrically conductive branded formulations; advantage lies in engineered resin systems and close OEM partnerships for thermal management in complex assemblies.

RTP Company (Winona, MN) — custom compounding expertise enabling tailored conductivity ranges; an attractive partner for OEMs seeking narrow spec windows and rapid iteration.

SGL Carbon (Wiesbaden, Germany) — graphite and expanded graphite powders targeting thermal conductivity with processability; relevant where heat transfer trumps electrical continuity.

LATI S.p.A. (Vedano Olona, Italy) — portfolio approach across fillers and matrix polymers, well positioned for European industrial and automotive supply chains.

Americhem (Cuyahoga Falls, OH) — thermally conductive compound development for EV and medical segments where regulatory documentation and traceability matter.

SABIC (Riyadh) — global resin and compound capability; beneficial where system‑level integration and long‑term supply commitments are required.

Imerys (Paris) — mineral and graphite filler specialist, useful in cases prioritizing cost‑effective conductivity with minimal process change.

OCSiAl (Luxembourg) — nanotube concentrates (TUBALL) that enable conductivity at low loadings; a technical differentiator for lightweight or high‑performance applications.

LEHVOSS Group (Hamburg) — high thermal conductivity solutions and specialty additive engineering, providing options for demanding thermal path designs.

Teknor Apex (Pawtucket, RI) — flexible compound formulations that combine reinforcement and conductivity; attractive for cross‑functional parts.

Bekaert (Zwevegem, Belgium) — metallic fiber solutions for robust electrical pathways and grounding in durable applications.

Capacity moves matter: announcements of expanded graphene and nanotube production capacity, as well as new compounding plants in North America, suggest increasing availability of advanced additives. This reduces time‑to‑market risk for OEMs willing to invest in pilot programs — but also creates a narrower window to secure preferential pricing and exclusivity on new‑generation concentrates.

Program partnerships are proliferating: company programs that qualify compounding partners for graphene‑enhanced products accelerate commercialization but shift the burden of qualification to ecosystems of compounders and processors. OEMs should define acceptance criteria and test protocols up front.

Raw‑material price volatility is persistent: recent upward moves in carbon black pricing and the broader raw‑material landscape require procurement teams to embed price‑pass‑through and hedging options into multi‑year supply agreements.

Diversify additive chemistry: avoid single‑track reliance on one conductive chemistry. Pair carbon black and graphite options with pilot programs for low‑loading CNT/graphene concentrates to secure both cost control and performance upside.

Qualify multiple suppliers early: given moderate market concentration, build at least two qualified sources per additive family and geography to mitigate capacity shocks and regulatory shifts.

Design for manufacturability: bring compounders into design reviews to align conductivity targets with injection/extrusion constraints and to avoid late‑stage rework.

Lock in conditional supply: consider staged offtake and volume‑option contracts with new capacity entrants in exchange for early technical collaboration or exclusivity in defined applications.

Price‑sensitivity modeling: incorporate feedstock price scenarios into product costing and margin plans; assign a short list of hedging and pass‑through mechanisms to procurement teams.

Regulatory contingency planning: map formulations containing carbon black and related materials against upcoming regional chemical evaluations and plan substitute pathways ahead of potential restrictions.

This release highlights the strategic conclusions and operational framework in our Thermoplastic Conductive Additives Market report while intentionally withholding granular regional, additive‑type and application split tables to preserve the action‑oriented value of the full deliverable. The comprehensive report includes proprietary segmentation models, an editable financial model, supplier scorecards and procurement templates — the precise tools teams need to convert insight into 2026 action plans.

For procurement directors, product leads and corporate strategists preparing budgets and qualification programs for 2026, the report is structured to facilitate immediate next steps: prioritize pilot investments, align supply contracts with forecast scenarios, and accelerate supplier qualification where advanced NANOCOMPOSITE additives will affect product performance and cost. Visit PW Consulting’s report page to access the full dataset, downloadable models and an executive briefing package tailored to your sector‑specific needs.

For detailed analysis of this topic, please visit the official page:Thermoplastic Conductive Additives Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com