Protein Expression Market 2026: Strategic Imperatives from PW Consulting’s Latest Industry Brief

As the biomanufacturing landscape accelerates toward higher-throughput discovery and commercial-scale biologics production, the global protein expression market commands renewed executive attention. PW Consulting’s newest market research—anchored on a 2025 base year and a 2026–2032 forecast horizon—translates complex technical trends into actionable strategic direction for CEOs, venture investors, and R&D leaders preparing 2026 budgets and M&A roadmaps.

Protein Expression Market

Executive snapshot: growth trajectory and what it means for 2026 strategy

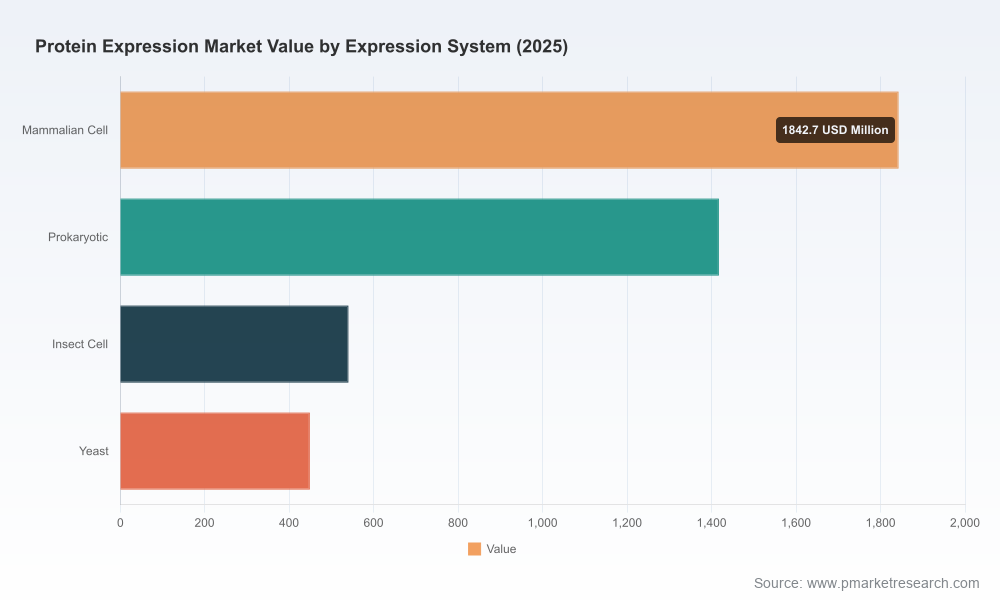

The protein expression market reached an inflection point in 2025, with total industry revenues of approximately USD 4.25 billion. Our modeling shows continued expansion at a compound annual growth rate (CAGR) of 9.2% over the 2026–2032 forecast window, taking the market to roughly USD 7.9 billion by 2032. This pace reflects a blended uplift driven by therapeutic biologics scale-up, accelerating research demand, and increasing adoption of higher-yield expression platforms.

Protein Expression Market

For decision-makers, the headline is simple: steady, above-market growth creates room for value capture—but only for players who translate scientific differentiation into operational scale, cost advantage, and regulatory readiness in 2026.

Protein Expression Market

What the report delivers — practical, transaction-ready intelligence

- Market sizing and forward-looking scenarios: base, upside and downside pathways that stress-test revenue and margin sensitivity to yield improvements, reagent price volatility, and GMP conversion rates.

- Serviceable addressable market (SAM) frameworks tailored to therapeutics, research reagents, and industrial proteins, with go-to-market implications for each channel.

- Playbooks for scaling: operational checklists for tech transfer, CMC handoffs, and automated expression scale-up—including recommended equipment, staffing profiles, and validation timelines.

- Regulatory impact mapping: how ICH Q5A and Q5D requirements reshape host cell selection, viral safety strategies, and supplier qualification in commercial workflows.

- M&A and partnership scorecards: quantitative and qualitative filters to prioritize targets that de-risk time-to-market or deliver margin accretion through vertical integration.

We designed the report as a working document—suitable for internal strategy sessions, investment committees, and commercial diligence—so that leaders can move from insight to decision in weeks rather than months.

Competitive landscape: reading strategic motions, not just capabilities

The market concentration is moderate: the top three firms account for a meaningful share of revenues while the top five further consolidate industry influence. PW Consulting’s analysis places the three-firm concentration (CR3) at 42.5% and the five-firm concentration (CR5) at 58.75%. These metrics underscore a dual structure: large platform incumbents driving scale and innovation, and a highly active long tail of specialist service providers capturing niche, high-margin segments.

Key strategic behaviors observed among leading players:

- Platform optimization for high-titer production. Major suppliers are competing on transient and stable mammalian systems engineered for multi-gram-per-liter titers—shifting the battleground from basic reagents to integrated reagent–cell–process bundles that customers can deploy quickly.

- Verticalization through services. Several incumbents are layering end-to-end expression services atop product offerings to accelerate commercialization timelines for therapeutics customers and secure recurring service revenue.

- Partnerships and automation. Strategic alliances that marry consumables with automated scale-up platforms are shortening process development cycles and favoring suppliers with plug-and-play integrations.

Representative examples from our market scan:

- Thermo Fisher Scientific continues to push reagent-process innovation, most recently launching a transfection reagent optimized for high-density CHO transient expression (October 2025), signaling an emphasis on productized, high-yield workflows.

- Merck KGaA is iterating on its transient mammalian platforms to deliver higher titers for therapeutic manufacturing (mid‑2025 system updates), demonstrating the premium placed on improved productivity per liter.

- Lonza’s collaboration with Cytiva on integrated automated scale-up platforms (March 2025) highlights the strategic move toward systems-level solutions that reduce scale-up risk for customers.

- Regional catalog and capacity plays—illustrated by Sino Biological’s rapid catalog expansion—are enabling faster target screening and time-to-data for preclinical programs.

PW Consulting’s competitive profiles in the full report provide granular capability maps, strategic positioning matrices, and acquisition candidate shortlists—intentionally withheld here to preserve the report’s unique commercial value.

Operational economics: inputs that matter for 2026 planning

Three operational levers will dominate supplier and buyer economics in 2026:

- Raw-material supply and quality. Plasmid DNA remains a bottleneck in many workflows; research-grade pricing sits at lower tiers while GMP-grade plasmid commands a premium—companies should forecast and contract accordingly to avoid CMC delays.

- Labor and skills. Skilled bioprocess technicians represent a material line item—often 15–20% of operating costs. Talent investments in 2026 should prioritize cross-functional process development and automation skills to compress timelines and reduce variability.

- Regulatory preparedness. Compliance with ICH Q5A and Q5D is non-negotiable for GMP pipelines; early investment in analytics for host cell protein characterization and viral clearance strategies yields outsized downstream value.

Operational stress-testing scenarios in the report quantify the P&L impact of yield improvements, plasmid pricing shocks, and labor-rate variance—tools that CFOs and manufacturing leads can plug into 2026 budgeting.

Strategic opportunities and risk vectors for 2026

- Invest in productivity, not just capacity. Targets that improve volumetric productivity (g/L) or reduce downstream complexity are more accretive than raw bioreactor volume expansion.

- Monetize integration. Bundling reagents, cell lines, and scale-up services creates sticky revenue pools and reduces customer churn in a market with rising reimbursement scrutiny for therapeutics.

- De-risk with partnerships. Strategic partnerships with automation and analytics providers can compress tech transfer timelines and lower validation costs—an attractive alternative to capital‑intensive greenfield capacity builds.

- Regional agility. Emerging-market demand will accelerate, but regulatory heterogeneity requires a localized compliance strategy; adopt a hub-and-spoke model to combine centralized process development with regional GMP execution.

- Selective M&A. Targets that fill capability gaps in high‑value therapeutic workflows—such as GMP plasmid manufacturing, high‑titer CHO platforms, or end-to-end scale-up automation—offer rapid route-to-value.

What PW Consulting recommends for executives planning 2026 moves

- Short term (0–12 months): initiate supply-chain hedging for critical reagents, set aside capital for automation pilots, and begin cross-functional training programs to shore up process development capacity.

- Medium term (12–24 months): prioritize partnerships that integrate consumables with automation, pursue tactical acquisitions to secure GMP inputs, and align product roadmaps to high-titer platform opportunities.

- Long term (24+ months): build differentiated, validated process platforms that can be licensed or white-labeled—turning technical leadership into recurring, high-margin revenue streams.

Each recommendation in the report is accompanied by implementation timelines, resource estimates, and risk mitigation checklists to make it immediately operational for teams starting 2026 initiatives.

Why this matters now

The combination of robust near-term growth (projected at a 9.2% CAGR through 2032), rising demand for therapeutic-grade proteins, and an evolving competitive topology creates a narrow window of advantage for firms that align R&D, operations, and commercial strategy in 2026. The choices made this year—about platform investments, partnerships, and talent—will determine who captures the high-return slice of the market as it approaches an estimated USD 7.9 billion by 2032.

Next steps — where to get the full intelligence

PW Consulting’s full Protein Expression Market report contains the detailed segmentation, supplier scorecards, scenario models, and financial templates that senior teams need to operationalize the strategies outlined here. This article serves as a strategic preview; the report itself includes proprietary data tables and dashboards that are intentionally withheld in this release to preserve client value.

For executives preparing 2026 budgets, RFP teams drafting vendor requirements, or investors performing commercial due diligence, the full report is the indispensable playbook to convert market momentum into measurable outcomes.

For detailed analysis of this topic, please visit the official page:Protein Expression Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com