Used Golf Cart Market — Strategic Insights for 2026 Decision-Making

Executive summary

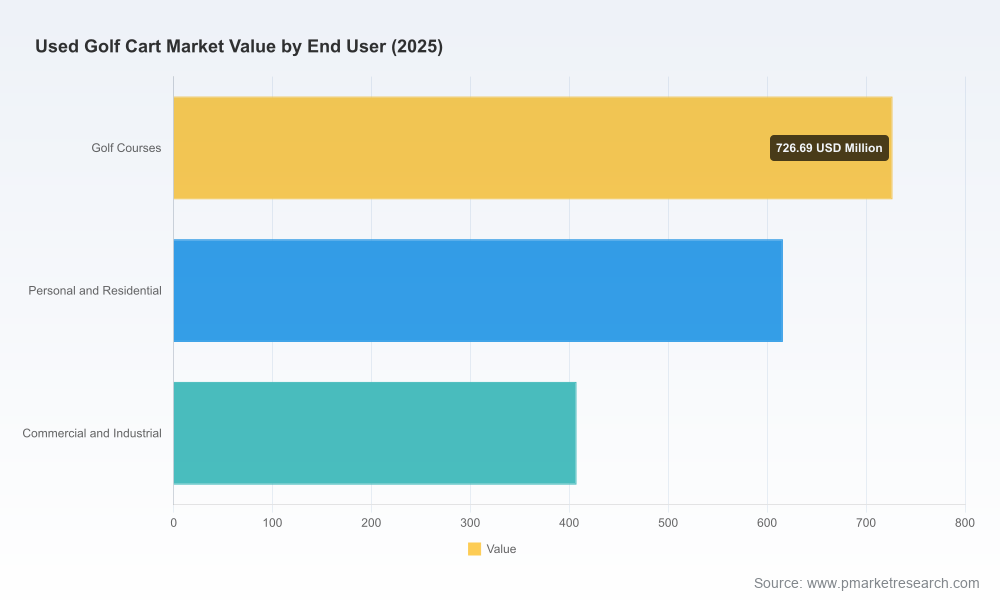

The global used golf cart market is in the middle innings of a structural transformation. After expanding from a multi‑hundred million USD base in 2020, total market revenues reached approximately USD 1,750 million in the report base year (2025) and are forecast to approach USD 2,675 million by 2032 — a compound annual growth rate of 6.25% across the 2026–2032 forecast window. This growth masks important transitions in powertrains, warranty economics, certification programs, and cross‑channel distribution that will determine winners and losers in the next 18–36 months.

Used Golf Cart Market

Why this report matters for 2026 strategy

For executives preparing budgets, capital allocation, M&A pipelines or dealer network strategies in 2026, the used market is no longer a secondary afterthought — it is a value pool that affects new‑vehicle pricing, parts & service margins, fleet replacement cadence and customer lifetime value. Our report translates macro momentum into decision‑grade intelligence, enabling leaders to:

Used Golf Cart Market

- Prioritize investments in certification, refurbishment and battery upgrades that materially improve resale and service margins;

- Design trade‑in and fleet refresh programs that protect gross margins on new sales while capturing aftermarket service revenue;

- Identify acquisition targets and partnership models that accelerate scale in high‑margin refurbishing and last‑mile distribution;

- Mitigate regulatory and logistics risks associated with lithium battery handling and cross‑border trade.

What’s inside — practical, executable deliverables

The report is structured for practitioners. Beyond headline market sizing and a 2026–2032 forecast, the deliverables include operational tools and templates you can deploy immediately:

Used Golf Cart Market

- Proven sizing methodology and reconciliation to public OEM volumes and trade flows so you can reproduce estimates for internal planning;

- Refurbishment playbook with bill‑of‑materials templates, labor time standards, and refurbishment quality tiers (including warranty and certification alignment);

- Total Cost of Ownership (TCO) and payback models for lithium retrofit vs. lead‑acid replacement under multiple utilization profiles; downloadable spreadsheets accompany the report;

- Dealer & fleet operating model benchmarks with KPI targets (turn times, margin per unit, inventory days) and a diagnostic toolkit to prioritize process improvements;

- Regulatory matrix and compliance checklist for cross‑border sales, air transport of lithium batteries and EU battery labelling requirements;

- Competitive dossiers on market leaders and high‑growth independents, including program economics, channel strategies and service capabilities;

- Scenario planning and stress‑test dashboards for raw‑material shocks, transport constraints, and accelerated electrification.

Key market dynamics shaping 2026 choices

Three interlocking dynamics will define the strategic landscape in 2026:

- Battery economics and technology adoption. Lithium battery systems continue to decline in cost — industry observations point to annual declines in the 5–10% range as manufacturing scales. Practically, this is enabling OEM and independent refurbishers to standardize lithium upgrades as a value‑creating service. A 48V lithium battery full set is now commonly available in a price band that materially changes retrofit ROI calculations for high‑use units.

- Safety and regulatory pressure. UL 2271 is the de facto safety benchmark for vehicle lithium packs in light electric vehicles, and new European battery regulations are tightening market access — including CE marking and mandatory battery management and health monitoring. Logistics rules (for example, air transport state‑of‑charge limits effective in 2026) are already constraining cross‑border options and adding operational complexity to resale channels.

- OEMs leaning into certified pre‑owned (CPO). Leading manufacturers are scaling factory‑backed CPO programs with multi‑tiered refurbishment, new‑parts replacement, and defined warranty packages. These programs are elevating buyer expectations and setting a higher bar for independent refurbishers that do not offer comparable certification or documented refurb outcomes.

Competitive landscape — where incumbents and disruptors are positioning

The used golf cart market is moderately concentrated. The top three players account for a material share of market influence, and the top five extend that reach further — a concentration profile that rewards scale in parts inventory, certified refurbishment capabilities, and dealer distribution.

Across the competitive set, we observe two dominant strategic archetypes:

- OEM certification & trade‑in leaders. Established OEMs are converting new‑vehicle sales ecosystems into controlled used channels via certified pre‑owned programs, structured trade‑ins and standardized refurbishment flows. Recent product and program updates demonstrate this push — examples include expanded lithium options, new street‑legal low‑speed vehicle (LSV) models with digital dashboards, and refreshed CPO offerings that bundle multi‑year battery and vehicle warranties.

- Volume electrification & affordability players. Newer electric‑first manufacturers and independent refurbishers are growing inventory rapidly by focusing on high‑volume urban and residential segments; their advantage is speed to market and aggressive pricing on lithium retrofits, but they must invest in quality assurance to compete against OEM certification trust marks.

Specific competitive moves to monitor in 2026 include expanded lithium offerings, upgraded digital service records for certified units, and dealer franchising models that incorporate refurbishment revenue sharing. These shifts are compressing the arbitrage window for non‑certified secondary sellers and increasing the strategic value of logistics and parts availability.

Strategic recommendations — prioritized actions for 2026

Below are high‑impact moves we recommend, sequenced by implementation horizon:

- Immediate (0–3 months): Implement a refurbishment quality tier and standardized warranty language across channels; begin pilot lithium retrofit programs for high‑utilization fleets with a monitored telematics rollout to validate cycle and charging assumptions.

- Near term (3–12 months): Negotiate battery supply agreements with capacity and price protection clauses; operationalize a CPO channel (dealer training, inspection checklists, digital proof‑of‑service) and set inventory turn KPIs to avoid value decay.

- Medium term (12–24 months): Pursue targeted acquisitions of regional refurbishers or logistics specialists to secure last‑mile distribution and parts pools; design bundled service contracts that convert one‑time refurbishment revenue into recurring service income.

- Governance & risk controls: Embed regulatory compliance (UL 2271, EU battery requirements, air transport SOC rules) into standard operating procedures and insurance coverage templates for refurbished units.

Three scenarios to incorporate into 2026 planning

- Base case (planning baseline): Growth consistent with the market CAGR; steady but disciplined adoption of lithium upgrades; OEM CPO programs scale at moderate pace. Focus: operationalize certification and defend resale margins.

- Electrification acceleration: Faster battery cost declines and favorable financing lift demand for lithium‑upgraded used units. Focus: secure battery supply, scale refurbishment lines, and monetize service data.

- Regulatory & logistics constraint: Tighter transport rules or regional labelling bottlenecks slow cross‑border trade and depress near‑term resale volumes. Focus: localize refurbishment capacity and prioritize compliance‑ready inventory.

How to use the report in executive decision processes

Procurement, strategic planning and M&A teams should treat this report as both an intelligence source and an execution kit. Use the market sizing and KPI benchmarks to stress test new trade‑in programs; deploy the refurbishment playbook and TCO models to price certified units; and apply the scenario dashboards in board‑level capital allocation discussions. Importantly, the report’s models are designed to be forked into your internal systems so forecasts and sensitivities can reflect your cost base and utilization profiles.

Closing — the value proposition for 2026

The used golf cart market is evolving from fragmented, price‑driven transactions to a structured, warranty‑backed secondary channel that competes on safety, service and verified performance. For companies that act decisively in 2026 — securing battery supply, standardizing refurbishment, and investing in certification and telemetry — the upside includes higher resale realizations, expanded service revenue, and defensible margins. For those that delay, competition from OEM CPO programs and fast‑moving electrification players will compress opportunities.

Our full report contains the underlying datasets, regional and end‑use segmentation, detailed company profiles and downloadable operational models you will need to convert insight into action. For access to the complete datasets, segmented forecasts, and the Excel toolset referenced in this press summary, please visit the report landing page to obtain the full research package and proprietary dashboards.

For detailed analysis of this topic, please visit the official page:Used Golf Cart Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com