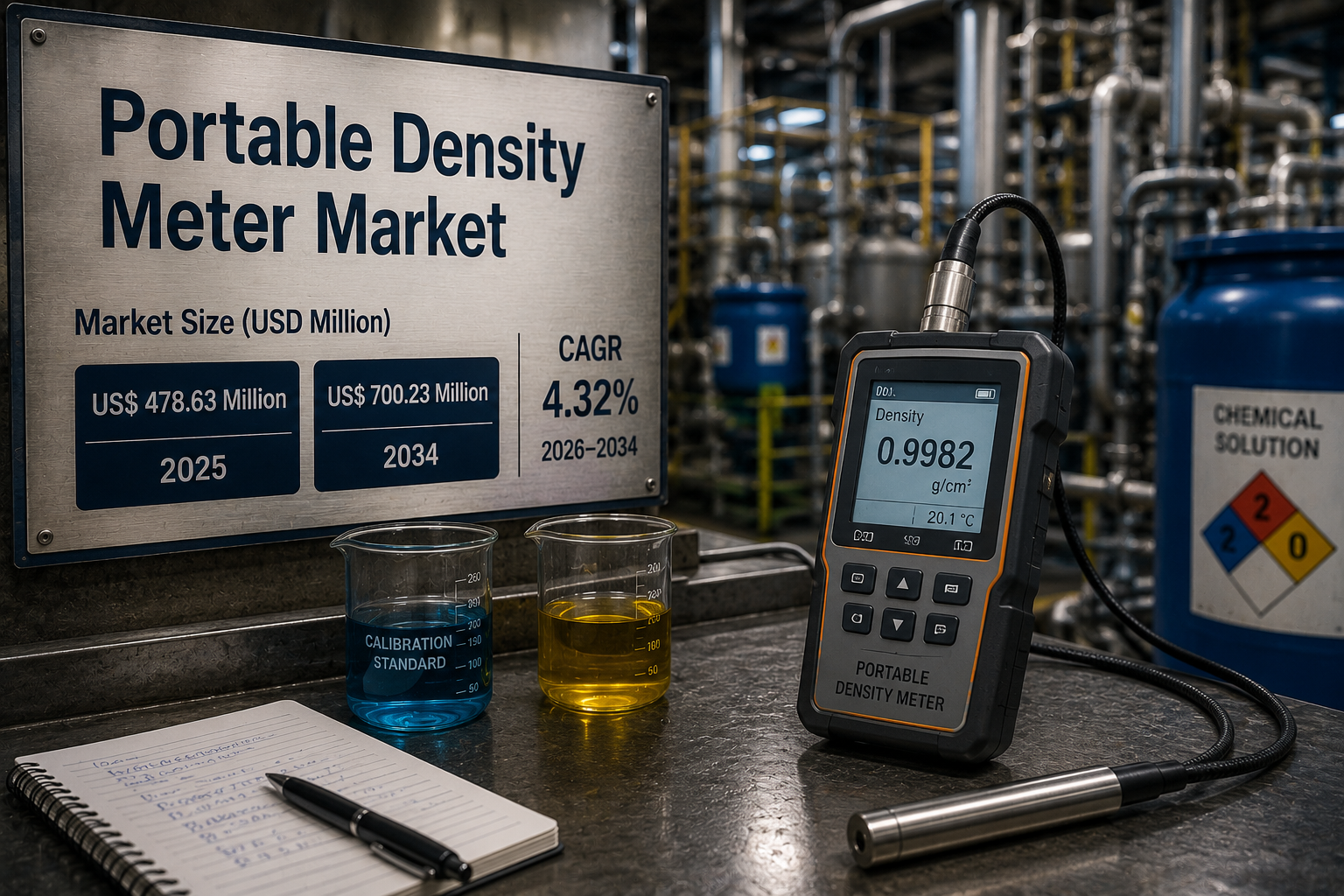

Portable Density Meter Market Competitive Analysis and Industry Developments

Other |

2026-05-12 13:16:30

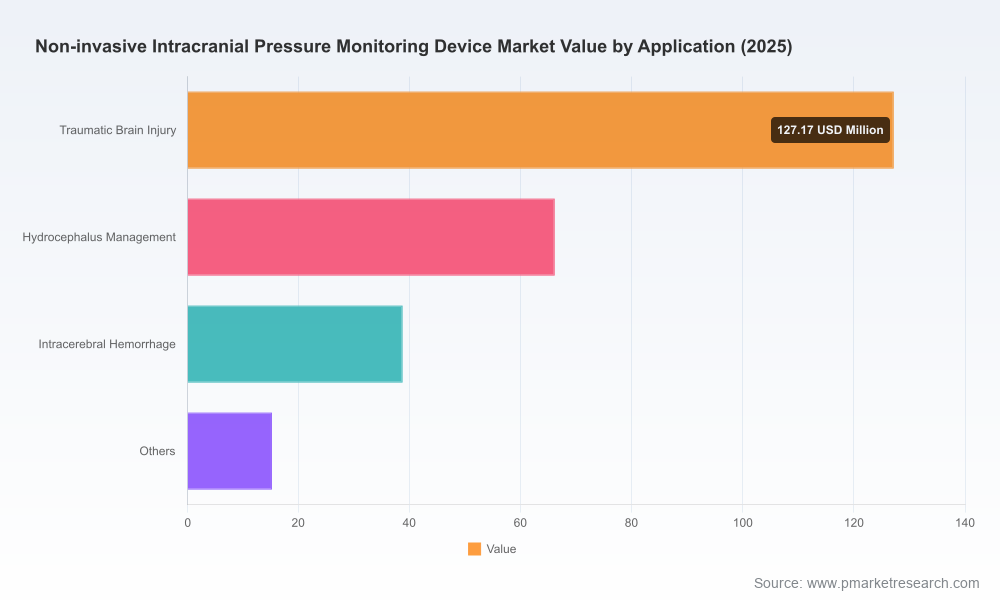

As healthcare systems accelerate adoption of minimally invasive diagnostics and digital-enabled critical care, non-invasive intracranial pressure (ICP) monitoring has emerged from research curiosity to a pragmatic market opportunity. PW Consulting’s latest market research — spanning historical performance (2020–2025) and a forward-looking forecast (2026–2032) — frames that transition with quantitative rigor and operational clarity. The global market is sizeable and growing: from a market base of USD 247.26 Million in 2025 the model projects a compound annual growth rate (CAGR) of 7.85% through the 2026–2032 forecast window, with the market trajectory continuing to accelerate into the end of the period. This briefing highlights why our report is strategic for 2026 planning while following a “trailer” posture: we demonstrate methodological depth and directional findings, while reserving granular segment numbers for the full report.

Non Invasive Intracranial Pressure Monitoring Device Market

Validation-to-Commercialization Convergence: Clinical validation and regulatory milestones achieved in 2024–2025 have moved several technologies to commercialization inflection points. This creates a narrow window in 2026 for product launches, channel commitments, and early-adopter deployment strategies that can define market share for the next five years.

Non Invasive Intracranial Pressure Monitoring Device Market

Shift in Clinical Guidance and Practice Patterns: Consensus statements and multimodal recommendations published in 2025 are changing how neurocritical teams think about non-invasive ICP tools—particularly in environments where invasive monitoring is impractical. Organizations that align evidence generation with these shifting guidelines will accelerate clinical uptake.

Non Invasive Intracranial Pressure Monitoring Device Market

Reimbursement and Regulatory Tailwinds: Supportive reimbursement signals and select breakthrough device designations lower commercialization friction. Companies that translate regulatory wins into payer and health-system value narratives in 2026 will command premium access.

Our model documents expansion from a mid‑hundreds million dollar base in 2025 to a materially larger market by the end of the forecast period. The projected CAGR of 7.85% embeds conservative assumptions on clinical conversion rates and measured adoption curves, accounting for differential uptake across hospital tiers and care pathways. Importantly, the path is non-linear: accelerating adoption of multimodal non-invasive protocols and integration into tele‑ICU architectures produces compound effects on equipment and services revenue in later years.

The competitive set combines specialist device pioneers, ultrasound and neuromonitoring incumbents, and platform companies bringing machine learning and telemetrics to critical care. PW Consulting’s qualitative and quantitative review focuses on technological differentiation, regulatory posture, evidence base, channel capabilities, and partnership ecosystems.

brain4care (Brazil) — A high-visibility innovator whose wearable cranial expansion sensor has secured FDA 510(k) clearance and published the largest patient study to date demonstrating improved accuracy in absolute ICP estimation versus several competing non‑invasive approaches. The company’s strengths are regulatory validation and a clear clinical narrative around continuous, wearable monitoring. Areas to watch: broader external validation and reproducibility across heterogeneous ICU populations.

Crainio (UK) — Early-stage entrant developing a forehead PPG-based probe combined with machine learning for real-time estimation. Clinical studies point toward a 2027 commercial timing. Strategic relevance for acquirers or distribution partners: Crainio offers a low-cost, low-power form factor that could scale in pre-hospital and emergency contexts.

Nisonic (Norway) — Ultrasound-focused team leveraging transorbital imaging and optic nerve sheath analytics. Their approach aligns with a diagnostic, point-in-time assessment model and is complementary to continuous wearable strategies. Opportunities center on bundled imaging platforms and emergency department deployment.

Viasonix and NovaSignal — TCD (transcranial Doppler) specialists whose systems provide cerebral hemodynamic context useful for non-invasive ICP inference. Their installed bases in vascular and neuro settings make them attractive partners for integration of ICP algorithms and multimodal monitoring solutions.

Natus Medical, Integra LifeSciences, Medtronic — Larger neurocritical care incumbents with established channels, device portfolios, and hospital-level relationships. Their strategic options include inorganic expansion via targeted acquisitions, OEM partnerships, or bundling of non-invasive features with legacy invasive monitoring suites.

Market concentration is moderate: the leading three to five vendors account for a meaningful share of reported revenues, which implies both an opening for challengers and significant bargaining power for early market leaders. Competitive advantage will accrue to firms that combine clinical evidence, regulatory clearance, and scale-enabled aftercare and integration services.

Regulatory Benchmarks and Validation Expectations — Established device accuracy standards and recent regulatory decisions set a high bar for clinical validation. For example, standards specify narrow accuracy windows for ICP estimation at clinically critical ranges, and recent studies show variability in method performance. Companies must design prospective, multicenter trials that address these standards and demonstrate robustness across patient phenotypes.

Consensus and Clinical Pathway Integration — The 2025 B-ICONIC consensus advocates multimodal non-invasive approaches when invasive monitoring is unavailable, creating a pathway for combined solutions. Vendors should pursue interoperability and joint-evidence strategies—pairing waveform-based devices with TCD or optic nerve sheath assessments to align with guideline recommendations.

Reimbursement Signals — Positive payer sentiment for novel neurocritical diagnostics exists, but reimbursement remains tied to demonstrable impact on care decisions, length of stay, and resource utilization. Value dossiers that quantify downstream savings—avoided transfers, reduced imaging, or earlier intervention—will be decisive in 2026 procurement cycles.

Segmented Launch Strategies — Prioritize tiered rollouts: focused adoption in neurotrauma centers, followed by emergency medicine and step-down units, then expansion into pre-hospital and remote monitoring. Tailor clinical training and integration support to each segment to shorten sales cycles.

Evidence Generation Roadmap — Invest in head-to-head and real-world evidence (RWE) studies that map device output to therapeutic decision points. Generate health-economic models contemporaneously to support payer conversations and hospital value committees.

Partnerships and Channel Strategies — Strategic alliances with TCD vendors, tele-ICU platforms, and EMR integrators accelerate adoption. For smaller innovators, distribution partnerships with large neuro device companies can provide rapid market access while preserving R&D focus.

Service and Software Monetization — Beyond hardware, recurring revenue opportunities lie in analytics subscriptions, cloud storage of waveform libraries, and decision-support modules. Early movers who design regulatory-compliant SaaS offerings for continuous monitoring will capture sticky revenue streams.

Investors and corporate development teams should watch for three near-term archetypes: (1) tuck-in acquisitions by major neuro device incumbents seeking non-invasive complements, (2) growth-stage financings for clinical validation and market scaling, and (3) platform plays combining sensor hardware with analytics and service delivery. Valuation premia will favor technologies with robust, multicenter evidence and clear pathways to reimbursement.

Proprietary market model with annualized revenues and sensitivity analyses across adoption scenarios for 2026–2032, enabling scenario planning and target-setting for product launches and investments.

Commercial playbooks for nine distinct hospital archetypes, including tailored value propositions, pricing levers, and anticipated sales cycle durations.

Regulatory and clinical evidence templates: trial designs, endpoint recommendations, and payer dossiers mapped to region-specific expectations.

Vendor benchmarking matrix covering technology maturity, regulatory status, evidence footprint, channel reach, and potential partnership fits—formatted to support M&A screening and partnership prioritization.

Operational checklists for integration with tele‑ICU and EMR systems, and a phased go‑to‑market roadmap aligned to 2026 procurement calendars.

Note: while this briefing summarizes directional insights and macro market sizing, the full report includes granular segmentation, regional and application-level forecasts, and vendor-level revenue estimates. These detailed models are intentionally withheld here to preserve our subscription value and to encourage direct engagement for bespoke queries.

Prioritize a small, high‑impact clinical validation program that aligns with the B-ICONIC multimodal guidance and targeted payer metrics.

Engage one or two strategic distribution or OEM partners to accelerate market entry in prioritized hospital archetypes.

Build a health‑economic model that links monitoring outputs to concrete operational levers (ICU days, imaging utilization, transfer avoidance) and test sensitivity assumptions against internal datasets.

Establish interoperability pilots with at least one tele‑ICU or EMR provider to demonstrate workflow integration and clinician acceptance.

Non-invasive ICP monitoring is transitioning from a niche diagnostic category to an integral component of modern neurocritical care. For executives weighing R&D priorities, partnerships, and commercial resource allocation in 2026, the critical questions are not if the market will grow, but how quickly individual technologies can demonstrate reliable clinical impact and integrate into decision workflows. PW Consulting’s market model—anchored by a 2025 base and a robust forecast through 2032—quantifies that growth and maps the practical levers companies must pull to lead. To convert strategy into advantage, stakeholders should combine targeted evidence generation, payer-focused value narratives, and scalable go‑to‑market partnerships within the coming 12 months.

For access to the full dataset, vendor-level analysis, and customizable scenario runs that inform deal and budget decisions for 2026, consult the full PW Consulting report and our advisory team.

For detailed analysis of this topic, please visit the official page:Non Invasive Intracranial Pressure Monitoring Device Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com