Commercial Food Dehydrators Market — Strategic Outlook for 2026: PW Consulting Insights

PW Consulting’s latest market research on the Commercial Food Dehydrators sector (base year 2025; historical window 2020–2025; forecast 2026–2032) distills the evidence-based intelligence that senior executives and investors need to make decisive 2026 moves. The global market expanded from USD 612.45 Million in 2020 to USD 792.7 Million in 2025 and is forecast to grow at a steady compound annual growth rate (CAGR) of 5.8% through the 2026–2032 window. Our revenue projections indicate continued expansion into the near term, with the market expected to cross key thresholds in 2026 and beyond—outcomes that demand concrete operational planning rather than reactive procurement.

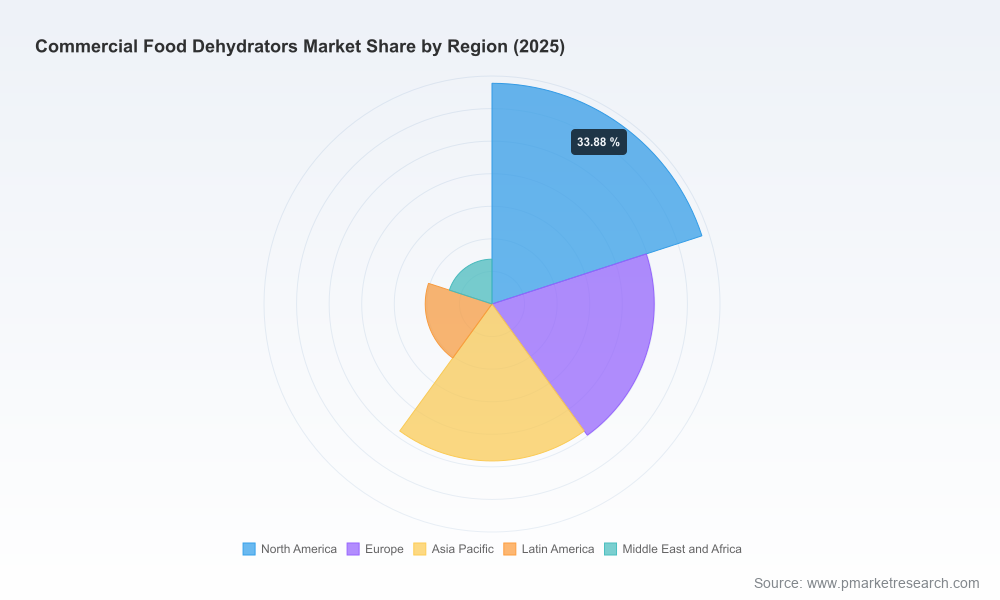

Commercial Food Dehydrators Market

Why this report matters for decisions made in 2026

Across food processing, specialty ingredient supply, and value-added pet/ingredient segments, dehydration technologies are shifting from commoditized appliances to strategically differentiated production assets. Macro pressures—rising energy costs, stainless steel commodity volatility, and tightening food-safety requirements—are compressing margins for manufacturers and operators. At the same time, OEM product innovation (airflow architectures, heat-pump systems, and process-control software) is creating room for premium positioning and aftermarket revenue. For leadership teams weighing CAPEX in 2026, understanding the interplay of these forces is essential to protect returns and accelerate payback.

Commercial Food Dehydrators Market

What PW Consulting’s report delivers (practical, operational, and proprietary)

- Rigorous market sizing and projection models (2020–2032) with scenario-based sensitivity testing calibrated to energy-cost and raw-material shocks.

- Benchmarked CAPEX and OPEX templates expressed in USD Million and per-unit energy consumption models to estimate total cost of ownership (TCO) across deployment types.

- Technology evaluation matrix covering airflow architectures, heat-pump adoption, batch versus continuous systems, and digital process control—mapped to production use-cases and throughput tiers.

- Regulatory compliance playbook addressing FDA and USDA operational constraints (including moisture control, lethality cooking requirements, and traceability workflows) with templates for quality documentation.

- Supply-chain stress tests and procurement playbook: supplier scorecards, hedging strategies for stainless steel, and sourcing pathways to mitigate lead-time risk.

- Commercialization and aftermarket strategies: service-as-product models, retrofit upgrades, and sensor-based predictive maintenance programs to increase lifetime value.

- Competitor intelligence dossiers and a pragmatic M&A checklist that aligns integration risk with value-creation levers.

Note: This release intentionally previews the scope and strategic utility of the report while withholding detailed subsegment-level tables and regional/application splits. Access to the proprietary breakdowns, vendor-level share analytics, and the interactive TCO calculators is provided only in the full report.

Commercial Food Dehydrators Market

Key market dynamics shaping 2026 strategy

- Energy-intensity is now a first-order economic variable. Commercial dehydration processes typically consume in the range of 15–30 kWh per batch; electricity price inflation of roughly 22% in major markets since 2020 has meaningfully altered operating economics and payback horizons. Buyers must evaluate energy-efficient architectures (e.g., heat-pump systems, staged recuperation) not as optional features but as primary decision criteria.

- Food-safety obligations elevate equipment specification. USDA guidance that certain meats and poultry be preheated to lethality temperatures before dehydration, together with FDA quality-control regulations, means factories must integrate validated thermal cycles and moisture-monitoring systems into both process design and supplier specifications.

- Raw-material cost volatility (notably stainless steel pricing swings observed between 2022–2025) materially impacts cost structures for premium stainless-steel models. Manufacturers should pursue modular designs and multi-sourcing strategies to preserve margin during commodity price cycles.

- Market structure remains moderately fragmented: the top three providers do not yet command a majority share, and the top five comprise a meaningful but not dominant portion of industry revenue—an environment that supports both consolidation and differentiated niche playbooks.

Competitive landscape — capability-focused analysis

We evaluated leading OEMs and solution providers across product breadth, technology differentiation, after-sales capability, and go-to-market positioning. Below are distilled strategic observations for market participants and buyers.

- Excalibur Dehydrator (Sacramento, CA): Known for patented air-movement innovations and a focus on process efficiency. Strengths lie in differentiated airflow architectures and an expanding digital/product line that supports process visibility. Strategic advice: leverage patented features to package service and consumables and to create higher-margin retrofit offerings for legacy fleets.

- NESCO (Metal Ware Corporation, Two Rivers, WI): Strong entry-to-mid-range commercial portfolio with emphasis on reliability and adjustable control systems. Strengths include broad channel relationships. Strategic advice: deepen vertical partnerships with co-packers and ingredient suppliers to secure recurring revenue and long-term supply contracts.

- Tribest Corporation (California): Offers advanced two-stage sequential temperature technology and premium tray systems. Recent launches underscore the market appetite for high-capacity, process-controlled units. Strategic advice: convert product sophistication into validated food-safety claims and training services to justify premium pricing.

- Commercial Dehydrators America (Alvarado, TX): Focus on high-tray-count units and long commercial warranties. Strategic advice: exploit warranty-to-service conversions and establish national maintenance footprints to capitalize on installed base economics.

- Advanced Food Dehydrators (Methuen, MA): Specializes in batch systems with integrated lethality cycles for jerky and meat producers. Strategic advice: partner with food-safety consultants to make verification and documentation a bundled differentiator.

- Nyle Systems, LLC (Brewer, ME) and IKE Group (Foshan, Guangdong): Both are leaders in heat pump and energy-efficient architectures—one with a US manufacturing base and the other with scale manufacturing in China. Strategic advice: buyers should weigh lifecycle energy savings against supply-chain and service considerations; OEMs should validate in-region service capabilities when selling energy-efficient systems abroad.

- LEM Products (Ohio): Pays attention to meat-processing applications with robust stainless-steel construction. Strategic advice: pursue specification-level wins with jerky and meat processors where hygienic design is a procurement driver.

While the market shows pockets of specialization and clear product-technology differentiation, we intentionally withhold vendor share tables and region-by-application revenue splits in this summary to preserve the exclusivity of the complete competitive dataset provided in the full PW Consulting report.

Actionable recommendations for executives planning 2026 investments

- Prioritize energy-first procurement. Use payback modeling that factors in current electricity price trajectories and batch energy consumption. Small percentage improvements in energy efficiency can shorten payback materially given today’s cost base.

- Mandate validated lethality and moisture-control cycles for meat and poultry applications within RFPs. This reduces downstream compliance risk and improves product consistency.

- Shift from one-time equipment sales to product-plus-service models. Warranty conversions, consumable contracts, and predictive-maintenance subscriptions materially increase customer lifetime value and reduce churn.

- Design modular, upgradable systems. Modular trays, sensor kits, and retrofittable controls protect customers against obsolescence and create aftermarket revenue streams.

- Hedge stainless-steel exposure and build dual-sourcing for critical components. Margin protection requires supplier segmentation and procurement playbooks that include price-adjustment clauses.

- Invest in digital process controls and data collection. Operators that can prove repeatable process conditions and traceability will win more institutional buyers.

- Use M&A selectively to acquire service networks or specialized IP—particularly in energy-efficient heat-pump technologies or validated lethality processes—not merely to add capacity.

- Run scenario planning with 3–5 year horizon stress tests (energy shock, raw-material spike, regulatory tightening) to understand capital and working-capital needs under adverse conditions.

How PW Consulting supports execution

Beyond strategic direction, our full report includes executable tools: TCO calculators, procurement RFP templates, vendor evaluation scorecards, regulatory compliance checklists (aligned to 21 CFR Part 110 and USDA operational guidance), and an annex of retrofit case studies showing realized energy savings and payback timelines. We also provide a tailored workshop offering to adapt the models to your production profile and capital constraints.

Conclusion — what to do next

The commercial food dehydrators market in 2026 is neither a high-volume commodity market nor an exclusive boutique niche—it is an operational lever that can materially affect margins and product quality across multiple food and ingredient value chains. With the market growing at a CAGR of 5.8% from the 2026 forecast base and rising energy and regulatory pressures, the right equipment choices, supplier arrangements, and service models will be defining competitive advantages.

For boards, CFOs, and plant managers contemplating CAPEX or M&A in 2026, PW Consulting’s full Commercial Food Dehydrators Market report offers the detailed, scenario-tested intelligence necessary to make those choices with confidence. Request the complete dataset and proprietary calculators to access segmented revenue breakdowns, vendor share matrices, and the step-by-step procurement playbook reserved for report subscribers.

For detailed analysis of this topic, please visit the official page:Commercial Food Dehydrators Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com