Aircraft Positioning Systems Market News and Recent Developments

Music |

2026-06-10 13:49:07

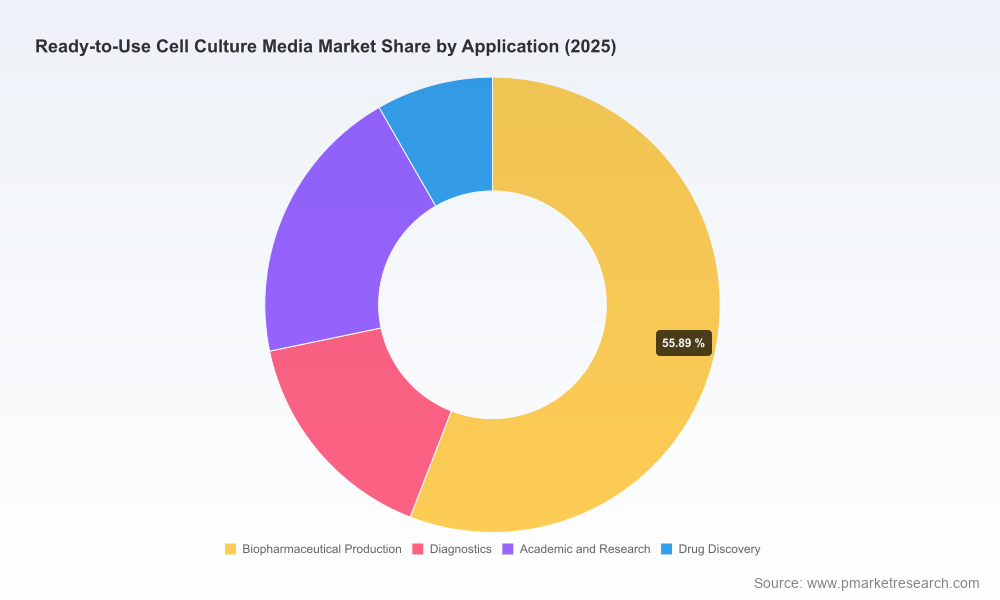

As organizations position for growth and resilience in 2026, ready to use (RTU) cell culture media have become a strategic linchpin across biopharma, advanced therapeutics, diagnostics, and academic research. PW Consulting’s latest market study — covering historical performance through 2025 and providing a 2026–2032 forecast — frames the landscape with hard macro metrics and an actionable playbook for executive decision-making. The global RTU cell culture media market, which reached approximately USD 2.42 billion in 2025, is forecast to continue expanding at a compound annual growth rate (CAGR) of 7.3% through the 2026–2032 horizon; by 2032, total market value is projected to approach the USD 4.0 billion threshold. These headline figures anchor a set of strategic implications that every senior leader in life sciences must weigh before committing capital in 2026.

Ready To Use Cell Culture Media Market

Macro clarity to de-risk capital allocation: The reported growth trajectory provides finance teams with an evidence-based baseline for scenario modeling, capital expenditure prioritization, and ROI thresholds for new product introductions or capacity expansions.

Ready To Use Cell Culture Media Market

Regulatory and supply continuity as competitive differentiators: The market is increasingly governed by stringent quality certifications and cold-chain requirements. Firms that secure high-bar certifications and optimize temperature-controlled distribution will obtain outsized share gains.

Ready To Use Cell Culture Media Market

Product and channel strategies need recalibration: The shift toward chemically defined, serum-free, and animal component–free formulations compels manufacturers and distributors to re-evaluate product roadmaps, channel partnerships, and value-added services that reduce end-user workflow variability.

PW Consulting’s synthesis of historical data (2020–2025) and forward projections (2026–2032) reveals a market advancing on multiple vectors: steady demand growth from biologics manufacturing and cell- and gene-therapy supply chains; accelerating adoption of serum-free and chemically defined media to improve reproducibility and regulatory compliance; and an expanding set of specialty media for stem cells, immune cells, and primary cell culture. The market’s expansion is balanced by two offsetting tensions: (1) rising demand for higher-specification media and associated logistics complexity; and (2) opportunities to lower cost and risk through formulation innovation, room-temperature stable products, and supply-chain consolidation.

From a structure standpoint, the market exhibits moderate concentration: the top three players command a meaningful share of the market, and the five largest vendors together control a majority position. This concentration underscores both the benefits of scale in manufacturing, quality assurance, and distribution, and the opening for focused innovators to capture high-margin niches.

Strategic market model — an integrated forecast framework (2026–2032) with scenario levers for demand shocks, pricing dynamics, and regulatory shifts to stress-test investment choices.

Commercial playbooks — go-to-market templates for launching RTU media across research, diagnostics, and biomanufacturing end-markets, including channel strategies, bundling approaches (e.g., media + kits), and OEM partnerships.

Regulatory and quality roadmap — compliance checklists mapped to FDA/EMA expectations and third-party certifications; an assessment of how recent industry certifications affect entry barriers and supplier selection.

Supply-chain and logistics toolkit — a practical checklist for cold-chain optimization, packaging innovation, shelf-life extension tactics, and alternative distribution models to reduce wastage.

Competitive benchmarking and M&A scouting — qualitative and quantitative vendor profiles, capability heatmaps, and a prioritized shortlist of potential acquisition or partnership targets for both scale players and specialists.

Commercial sensitivity analyses — pricing elasticity models, tender-response templates, and channel margin tables that support contract negotiation and tender management.

The competitive field includes long-standing life-science conglomerates, specialized media houses, and distributors that combine product breadth with global logistics. Our analysis highlights a handful of capability clusters that correlate with success:

Product breadth and formulation depth — Thermo Fisher Scientific, Merck KGaA, and Sartorius exemplify firms with wide portfolios spanning classical media, serum-free, and chemically defined formulations. Their ability to serve research and process-scale needs reduces procurement complexity for large customers.

GMP and certification leadership — recent industry milestones (for example, the adoption of EXCiPACT cGMP certification by a major supplier across multiple production sites) demonstrate how certification can become a procurement gate and a differentiator for suppliers targeting therapeutic manufacturing.

Specialist differentiation — companies such as PromoCell, STEMCELL Technologies, and FUJIFILM Biosciences carve defensible positions with primary-cell or stem-cell–focused media and bundled solutions (e.g., Cell KITs that pair media with cells). These specialized offers increase customer stickiness in translational workflows.

Channel and distribution reach — distributors and channel players (e.g., Avantor, Corning, and Danaher/Cytiva) provide scale and high-touch customer support for labs and manufacturing sites globally, enabling rapid fulfillment and integrated service models.

R&D pipeline and manufacturing flexibility — firms investing in chemically defined, non-animal origin media and in flexible GMP production capacity (including custom media services) will capture higher-margin, regulated demand segments.

Recent vendor activity reinforces these trends: a prominent certification by a major life-science supplier elevated the baseline for pharma-grade media; several specialist vendors launched integrated product-service bundles and entered GMP services for cell therapies; and room-temperature stable or BenchStable products are being positioned to relieve cold-chain burden.

Prioritize regulatory alignment before capacity expansions. Obtain or partner for required certifications early in the investment cycle—this reduces time-to-revenue for therapeutic and CDMO customers.

Invest in formulation innovation that reduces logistical frictions. Room-temperature stable formulations and packaging that extend in-use stability create pricing power and reduce supply-chain costs for buyers.

Build modular manufacturing and supply options. Flexible manufacturing cells and multi-site redundancy mitigate raw material volatility and allow rapid scaling in response to bioprocessing demand surges.

Differentiate through bundled solutions and services. Combining media with application-specific kits, technical support, and QC analytics increases customer lifetime value—especially in primary cell and stem-cell niches.

Adopt an acquisition-as-accelerator mindset selectively. M&A can quickly add niche formulations, GMP capability, or route-to-market advantages. Use our vendor heatmaps to identify targets that move the needle on capabilities rather than only on volume.

Embed sustainability and ethical sourcing into product stories. Non-animal-origin formulations reduce regulatory friction and resonate with end customers and institutional buyers focused on ESG metrics.

Month 0–3: Run a regulatory gap analysis vs. targeted customer segments and begin credentialing pathways or partner selection.

Month 3–6: Pilot a room-temperature stable product or a bundled kit in one strategic geography to validate logistics savings and margin uplift.

Month 6–12: Scale GMP-compliant production lines and integrate predictive inventory algorithms for cold-chain inventory optimization.

Ongoing: Maintain a two-track innovation pipeline—one delivering incremental cost/stability improvements and the other focused on high-value specialty media for cell therapy and vaccine production.

Boards and executive teams should treat the report as both a strategy and an execution manual. Use the macro forecast to validate growth assumptions in the corporate plan; use the scenario models to stress-test capex and M&A; and deploy the vendor matrices and operational toolkits to accelerate commercial launches and supply-chain improvements. Where the report provides teaser-level competitive insights and capability mappings, it also points executives to the detailed segment matrices, vendor scorecards, and proprietary pricing models that underpin our conclusions — these supporting datasets are essential for investment committees and procurement teams when finalizing vendor shortlist and term sheets.

As the RTU cell culture media market matures, the winners in 2026 will be those that combine formulation leadership, quality and certification credentials, logistics excellence, and customer-centric service models. PW Consulting’s market study synthesizes the data-driven trajectory—with clear macro baselines and growth expectations—to help executives make disciplined, timely choices. For leadership teams weighing expansion, partnership, or M&A decisions, the right mix of technical, regulatory, and commercial actions this year can materially improve market position throughout the forecast window.

To access the full report — including detailed segment analyses, vendor scorecards, and the executable toolkits referenced above — visit our report page or contact PW Consulting’s Life Sciences Practice for a tailored briefing that connects these insights to your 2026 strategic plan.

For detailed analysis of this topic, please visit the official page:Ready To Use Cell Culture Media Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com