Hydrogen Truck Market Growth Trends, Opportunities and Forecast to 2035

Other |

2026-06-04 13:49:57

As corporate sustainability commitments mature from aspirational statements to procurement KPIs and regulatory obligations, seaweed-based packaging has moved from niche innovation to an investible industrial opportunity. PW Consulting’s latest Seaweed Based Packaging Market report — covering historical performance (2020–2025) and a forward-looking forecast to 2032 — provides decision-grade intelligence for executives preparing capital allocation, supply-chain transformation, and product-portfolio strategies in 2026.

Seaweed Based Packaging Market

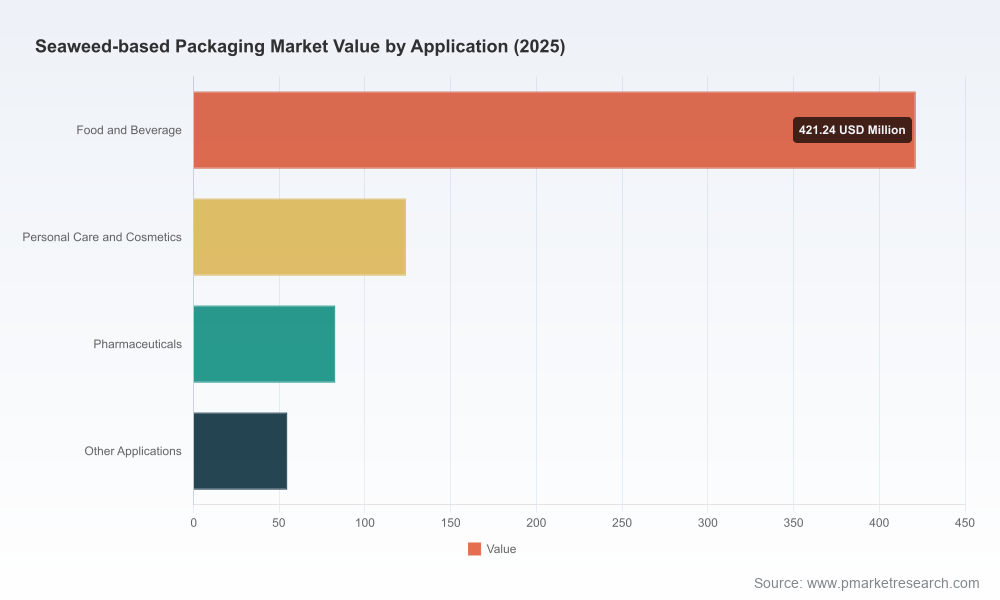

Our analysis shows the market has more than doubled in size over the past five years, rising from the low hundreds of millions (USD, Million) in 2020 to an estimated USD 682.5 Million in 2025, and is forecast to continue expanding at a compound annual growth rate (CAGR) of approximately 14.85% through the 2026–2032 window. By 2032 the addressable market is modeled to approach USD 1.8 Billion. That trajectory reflects accelerating commercial adoption driven by regulation, procurement pressure, and rapid technology maturation — but it is uneven, fragile to raw-material price swings, and sensitive to scaling choices.

Seaweed Based Packaging Market

The market remains structurally fragmented: no single incumbent commands dominant share, and the top players collectively account for less than one-third of global activity — a dynamic that creates opportunity for well-capitalized entrants and fast followers. Key archetypes to watch include mission-driven start-ups focused on single-use foodservice, vertically integrated manufacturers aiming for industrial scale, and technology-focused vendors targeting formulation and barrier performance.

Seaweed Based Packaging Market

Regulation is the single most consequential demand accelerant for seaweed-based packaging in 2026. The EU’s Packaging and Packaging Waste Regulation (PPWR) introduces stringent limits on PFAS in food-contact packaging beginning August 2026 — effectively advantaging PFAS-free bio-based barrier solutions. Concurrently, extended producer responsibility (EPR) schemes — including the UK’s recyclability-modulated fee structure and several U.S. state-level EPR laws — are re-pricing end-of-life liabilities and shifting economics toward recyclable, compostable, and demonstrably low-toxicity alternatives.

For buyers and converters this creates a compressed window to validate alternatives against compliance criteria and to negotiate sourcing structures that anticipate fee modulations. The report provides timing matrices aligning procurement milestones with regulatory deadlines to minimize stranded inventory and compliance shocks.

Feedstock price dynamics are a real and present constraint on margin expansion. During Q4 2025 sodium alginate exhibited meaningful price dispersion across markets; refined carrageenan prices also climbed materially amid constrained seaweed availability. These dynamics translate into two operational implications: upward pressure on unit costs for seaweed-based resins and the need for diversified sourcing or vertical integration. Our modeling demonstrates how raw-material price spikes can compress EBITDA by double-digit percentages unless procurement hedges, blend strategies, or contractual pass-throughs are implemented.

Our methodology combines primary interviews across the value chain, plant-level engineering cost modeling, regulatory timelines, and live-price inputs for feedstocks to produce actionable scenarios rather than static forecasts. The report is structured to support four immediate use cases for 2026:

To preserve the report’s commercial value and to encourage direct engagement, this press brief highlights strategic insights while intentionally omitting detailed segment-level allocations, regional share breakdowns, and provider-specific revenue figures. Those granular datasets — including split-level demand by format, application-performance matrices, and supplier revenue benchmarking — are available exclusively through the full PW Consulting Seaweed Based Packaging Market report and accompanying data workbook.

Executives who need to act in 2026 should secure detailed scenario outputs and the supplier database to move from intent to implementation. PW Consulting offers bespoke briefings, scenario workshops for procurement and R&D teams, and confidential advisory engagements to accelerate pilot-to-scale transitions while protecting margin and compliance. Contact our strategy desk to schedule a tailored executive workshop and obtain the full report and data workbook.

PW Consulting — Helping industry leaders convert sustainability ambition into resilient, profitable strategies for the age of bio-based packaging.

For detailed analysis of this topic, please visit the official page:Seaweed Based Packaging Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com