هيدرا فيشل لتجديد البشرة في الرياض

Health |

2026-06-27 08:52:13

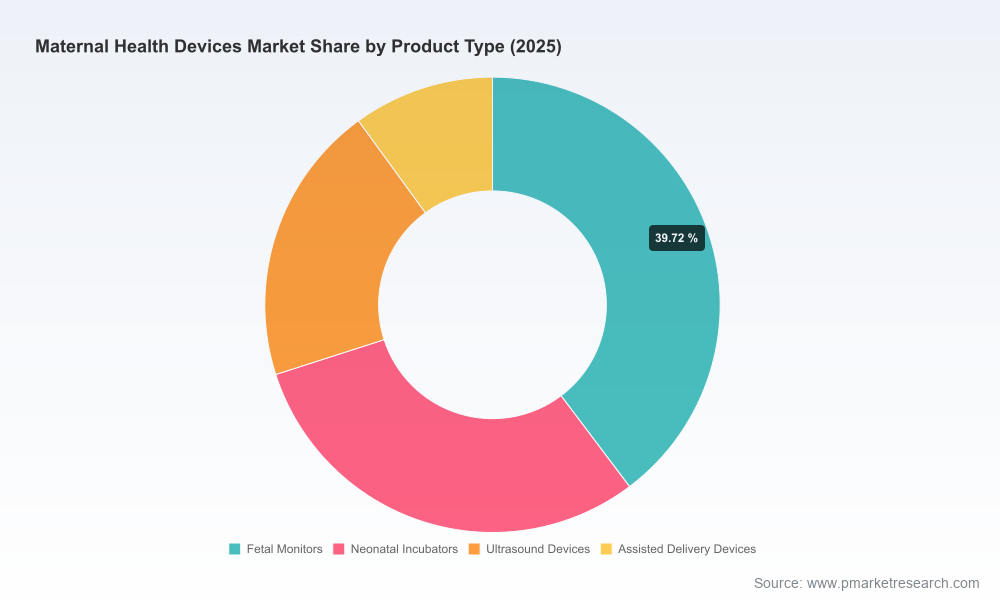

PW Consulting today releases its latest Maternal Health Devices Market report, a practitioner-focused strategic resource designed for executive teams, corporate development groups, and product leaders preparing 2026 roadmaps. Built on a 2025 base year and a detailed forecast through 2032, the study quantifies a market that reached approximately USD 4.5 billion in 2025 and is expected to grow at a compound annual growth rate (CAGR) of 7.15% across the 2026–2032 horizon. The research couples rigorous market-sizing with actionable playbooks—enabling decisions grounded in data without disclosing the proprietary micro-segmentation models that underpin our recommendations.

Maternal Health Devices Market

Regulatory and reimbursement inflection points. New CPT codes for digital health and remote patient monitoring became effective on January 1, 2026, materially improving the commercial case for connected maternal-fetal monitoring solutions. At the same time, regulatory momentum—exemplified by recent 510(k) clearances for wireless, beltless maternal-fetal platforms—has lowered technical and market-entry barriers for next-generation devices.

Maternal Health Devices Market

Clinical practice and standards are tightening. National initiatives, such as recognition programs that standardize maternal levels of care and federal models to transform maternal health, are shifting procurement toward risk-appropriate, integrated perinatal solutions—creating selective demand for advanced monitoring, telehealth-enabled follow-up, and data-driven care coordination.

Maternal Health Devices Market

Capital constraints in provider systems. Hospitals are confronting rising capital and operating costs; for example, investments in ICU-capable beds and advanced monitoring infrastructure are increasingly scrutinized. This creates pressure for flexible acquisition models (leasing, managed services) and for vendors to demonstrate rapid return on investment through reduced length-of-stay, fewer adverse events, and reimbursement capture.

Technology transition to wearables and data services. The clinical community’s growing acceptance of wearable, wireless maternal-fetal monitoring, and the emergence of fully integrated maternal monitoring platforms are accelerating a shift from device-centric sales to platform and services business models.

Robust market-sizing and forecasting: A transparent methodology anchored to a 2025 base and projecting through 2032 (CAGR 7.15%), with scenario analyses that stress-test adoption rates, reimbursement uptake, and regulatory timing.

Competitive intelligence and capability maps: An assessment of incumbent and emerging vendors—covering product portfolios, regulatory status, go-to-market strategies, and likely M&A targets—designed to inform partnership and competitive responses.

Commercial playbooks: Ready-to-deploy go-to-market and pricing playbooks for enterprise sales, leasing models, and payor engagement—tailored to hospitals, clinics, and home-health channel economics.

Reimbursement and regulatory navigation: Tactical guidance on leveraging new CPT codes, structuring evidence-generation programs, and sequencing regulatory filings to optimize time-to-market and payer acceptance.

Procurement and contracting templates: Practical negotiation levers and contracting language that reflect hospital CapEx pressures and service-oriented procurement preferences.

M&A and partnership screening: A prioritized list of capability adjacencies and technology clusters that buyers should evaluate (wearables, analytics, interoperability layers, and remote monitoring platforms), supplemented with valuation heuristics and integration risk checklists.

The maternal health device market today blends major systems providers with specialized innovators. Market concentration is meaningful but not prohibitive: the top three firms account for roughly 42.5% of the market, while the top five capture about 58.8%, signaling a field where scale matters but opportunities remain for focused challengers and fast-followers.

Koninklijke Philips N.V. continues to position its Avalon line as a leader in integrated fetal and maternal monitoring with wireless options that emphasize clinical workflow and interoperability—appealing to large perinatal centers and systems standardizing on single-vendor environments.

GE HealthCare leverages enterprise reach and portfolio breadth, expanding indications for patch-based monitoring to encompass broader obstetric populations and integrating peripartum data into hospital monitoring architectures.

Sibel Health represents the archetypal challenger: a software-hardware native, wearable-first platform that has just reached a regulatory milestone for fully wireless continuous maternal and fetal monitoring—precisely the technology archetype that shifts competitive dynamics toward outpatient and hybrid models of care.

Medtronic, Siemens Healthineers, Natus, CooperSurgical, and Becton Dickinson (BD) each bring differentiated strengths—ranging from broad patient monitoring portfolios and service ecosystems to specialized obstetric diagnostics and consumables—making them potential strategic partners or acquirers for focused innovators.

Recent product clearances and expanded indications (notably wireless and beltless monitoring platforms cleared in 2024–2026) are already reshaping customer procurement questions: “Can this device integrate with our EHR? Will it reduce in-hospital monitoring time? How will it be reimbursed in a bundled care model?” Our analysis shows that answers to these questions will determine winners in the next three years.

Prioritize platform and data-led propositions. Convert one-off device sales into platform subscriptions or managed service contracts. Clinical evidence that links monitoring to outcomes—and to reimbursement—will be a decisive commercial differentiator.

Accelerate regulatory and reimbursement sequencing. Align 510(k)/CE strategies with payer coverage milestones. Leverage the new CPT codes and targeted evidence generation (registries, pragmatic trials) to secure faster commercial uptake.

Design flexible acquisition models. Given provider CapEx scrutiny, build leasing and outcome-linked pricing into commercial offers. Vendors that can reduce near-term budget impact for hospitals will win procurement conversations.

Target Medicaid and state programs. With federal models and state-level investments in maternal health, companies should pilot programs in high-need regions to both demonstrate public-sector impact and establish long-term contracts.

Prepare for consolidation and partnership plays. The moderate concentration means strategic M&A and partnerships will be primary routes to scale for innovators; conversely, incumbents should selectively acquire niche capabilities (wearables, analytics) to defend share.

Board and investor briefings: Use the report’s executive dashboards and scenario models to stress-test revenue forecasts and capital allocation decisions against alternative regulatory and reimbursement pathways.

Portfolio and R&D prioritization: Apply the product/market fit matrices and clinical adoption timelines to decide which device upgrades, software integrations, or clinical studies to fund in 2026.

Commercial strategy and field execution: Deploy our go-to-market playbooks to reconfigure sales compensation, create bundled service offerings, and structure hospital pilot programs that build reference cases.

M&A diligence and partnership scouting: Leverage our screening criteria and integration risk framework to evaluate targets in wearables, data analytics, and home-monitoring services.

PW Consulting’s Maternal Health Devices Market report is grounded in a multi-source research approach—triangulating vendor disclosures, regulatory filings, primary interviews with clinical and procurement leaders, and quantitative modeling. While this release highlights the strategic contours and operational implications we expect to shape 2026 decision-making, the full report contains the proprietary segmentation models, detailed market-size worksheets, playbook templates, and vendor benchmarking matrices that corporate teams will need to act decisively.

For senior leaders preparing budgets, refining product roadmaps, or evaluating transactions in 2026, this report is designed to shorten the path from insight to implementation—balancing rigorous analysis with immediately deployable commercial tactics. To access the complete report, including the downloadable financial models and customizable slide decks for executive briefings, please consult the PW Consulting resource page.

Contact PW Consulting’s Maternal Health Devices team to schedule a briefing and obtain the full set of appendices and templates that support the 2026 strategic planning cycle.

For detailed analysis of this topic, please visit the official page:Maternal Health Devices Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com