US Distilled Water Market Report: Industry Insights, Growth Drivers & Opportunities

Other |

2026-07-01 11:30:04

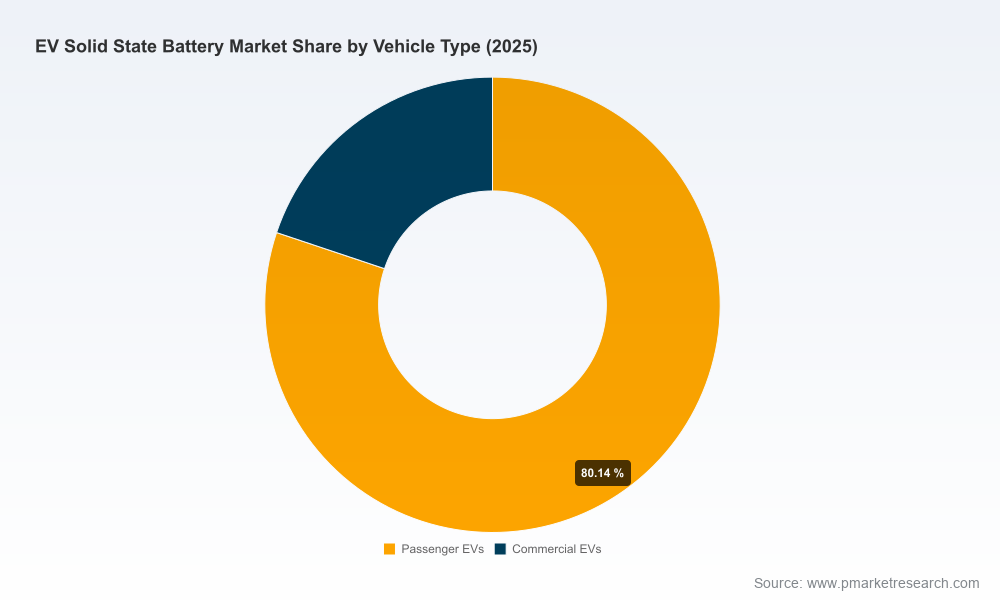

PW Consulting today publishes a focused industry brief derived from our forthcoming Ev Solid State Battery Market research report. As capital allocation, product roadmaps and policy responses converge in 2026, solid-state batteries (SSBs) move from laboratory promise to near-commercial reality. Our analysis shows an industry-scale expansion: global market value rising from roughly USD 125 million in 2020 to over USD 1.05 billion in 2025, and with a modeled compound annual growth rate of 67.35% through the forecast horizon. By 2032 our baseline scenario projects market value in the tens of billions (USD 38.7 billion), underscoring the urgency for corporate leaders to translate exploratory programs into executable strategies this year.

Ev Solid State Battery Market

Technology-commercialization alignment: 2024–2026 saw multiple vendors move from lab validation to prototype shipments and pilot production lines. These transitions create tangible decision windows for OEMs, tier suppliers and material producers to lock in partnerships and scale-up roadmaps before volume economics solidify.

Ev Solid State Battery Market

Regulatory deadlines and incentives: Regulatory regimes are tightening technical expectations for battery energy density and recyclability, and several jurisdictions now embed direct manufacturing incentives. Executives must reconcile compliance timelines with product launch and investment plans in 2026 to capture subsidies and avoid retrofit risk.

Ev Solid State Battery Market

Supply chain normalization and cost inflection: Raw material and component prices have shown early stabilization. For example, lithium metal foil and sulfide electrolyte costs experienced notable moves in early 2026 — dynamics that materially influence unit economics for SSBs and therefore influence near-term sourcing and capex choices.

Competitive concentration and ecosystem formation: Market concentration metrics indicate a race shaped by a handful of dominant players, while the remainder of the ecosystem is populated by specialized entrants and regional champions. The next 12–18 months will determine whether partnerships or vertical integration become the dominant route to scale.

PW Consulting’s Ev Solid State Battery Market report is designed as a practical playbook for corporate leaders and investors. Contents include:

Robust market-sizing and forecast model (historical series 2020–2025; forecast 2026–2032) with scenario variants and sensitivity testing to stress-test assumptions around material costs, production learning rates and policy interventions.

Technology maturity and roadmaps — comparison of electrolyte chemistries, anode approaches and manufacturability constraints mapped to commercialization timing and likely cost trajectories.

Supply-chain heatmaps highlighting critical materials, single-source risks and actionable mitigation strategies (contract structures, geographic diversification, collateralized offtakes).

Unit-cost build-ups and break-even analyses that translate material and component price inputs into cell- and pack-level economics under multiple production scale scenarios.

Competitive landscape module with vendor capability assessments, likely go-to-market plays, and partner fit matrices for OEMs, suppliers and pure-play battery firms.

Regulatory impact dashboard — mapping major rules, target dates, and compliance levers (including recyclability and energy-density standards), plus a playbook for policy engagement.

M&A and partnership scouting framework — valuation heuristics, diligence checklists and integration pathways tuned to the SSB value chain.

To preserve strategic advantage for our clients, the public brief intentionally summarizes themes and implications while detailed segment-level tables, regional and application splits, and our downloadable financial model remain accessible only via the full report.

The competitive field combines legacy automotive OEMs, major battery manufacturers, and agile pure-play specialists. Our report evaluates each participant for technology readiness, scale potential and strategic intent. Highlights below synthesize observable positions and recent developments.

Toyota Motor Corporation (Japan) — Toyota’s multi-generation prototyping and public roadmap keep it at the center of SSB narratives. With prototypes targeting extended range profiles and fast-charge ambitions, Toyota remains a pioneer among OEMs moving toward late-decade commercialization.

Samsung SDI (South Korea) — Samsung SDI’s lab-to-prototype throughput and automaker partnerships position it as a high-density candidate for integration in next-generation EV platforms. Collaboration scale with major OEMs is a key differentiator.

LG Energy Solution (South Korea) — Progress on sulfide-based chemistry and early pilot lines signal strong industrial execution capability; LGES is positioned to convert pilot learnings into automotive-grade supply if production yields scale favorably.

CATL (China) — CATL’s playbook emphasizes rapid learning and mass-production readiness. Expect aggressive scale bets and technology aggregation to preserve manufacturing lead time.

QuantumScape (USA) — Focused on anode-free lithium-metal architectures, QuantumScape’s validated prototypes and sample shipments to OEMs illustrate an R&D-to-test pipeline that investors should monitor closely for manufacturability breakthroughs.

Solid Power (USA) — With sulfide electrolyte cells entering EV cell production and OEM validation programs, Solid Power represents an early mover into automotive-scale cell formats.

ProLogium (Taiwan) — Ceramic-based cells and operational gigafactory capacity highlight ProLogium’s commitment to supply-chain control and prototype supply to tier-one automakers.

Blue Solutions (France) — Commercial polymer SSB deployments in niche fleets show the route to early commercial use-cases and offer instructive lessons for fleet-first commercialization strategies.

Murata Manufacturing & Toshiba (Japan) — Both bring device-level reliability and incremental scaling approaches, useful where safety and longevity trump raw energy density.

Market structure analysis suggests a moderate level of concentration among the largest firms, implying that strategic alliances and selective vertical integration will be common pathways to secure capacity and technology control.

Raw material and component cost trajectories — lithium-metal foil prices and sulfide electrolyte bulk costs are material inputs that will influence supplier selection and long-term contracts.

Policy and incentives — domestic production credits and regional battery regulations materially change project NPV and time-to-market calculus; capturing tax credits and remaining compliant with recyclability standards will be central to financial planning.

Standards and validation — established electrochemical test standards create a baseline for safety and performance certification; design teams should incorporate these early to avoid downstream rework.

Manufacturing scale and yield improvement — early commercial winners will be those who can convert pilot yields into reliable high-yield lines while controlling capex intensity and working capital needs.

Recycling and second-life economics — regulatory pressure and material scarcity make circularity a strategic necessity rather than a compliance afterthought.

Prioritize staged investment: use scenario outputs to define trigger points for moving from pilot to committed capacity.

Hedge supply risk: structure multi-year material contracts with indexed pricing and offtake clauses tied to validated performance milestones.

Craft partnership mosaics: combine technology licensing, JV manufacturing and long-term supply agreements to balance speed-to-market versus capital exposure.

Embed regulatory roadmaps: align product specifications to known regulatory inflection dates to qualify for incentives and avoid compliance retrofits.

Design rigorous go-to-market pilots: prioritize fleet, commercial or limited regional launches that de-risk high-volume consumer deployments.

PW Consulting’s full Ev Solid State Battery Market report contains the complete dataset, granular segmentation models, company scorecards, and the Excel-based scenario engine referenced above. This public brief is purposefully selective — intended to orient executive teams and stimulate strategic conversations. For organizations planning capital allocation, strategic partnerships or M&A activity in 2026, the full report provides the operational detail and financial models necessary to move from strategy to execution.

Contact PW Consulting to schedule a briefing, obtain the full report and access the interactive model. Our advisory teams are available to translate the findings into bespoke roadmaps, diligence packages and negotiation playbooks tailored to your role in the evolving solid-state battery value chain.

For detailed analysis of this topic, please visit the official page:Ev Solid State Battery Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com