Global Foam Facial Cleanser Market Growing at 5.8% CAGR Through 2034

Other |

2026-06-27 12:20:52

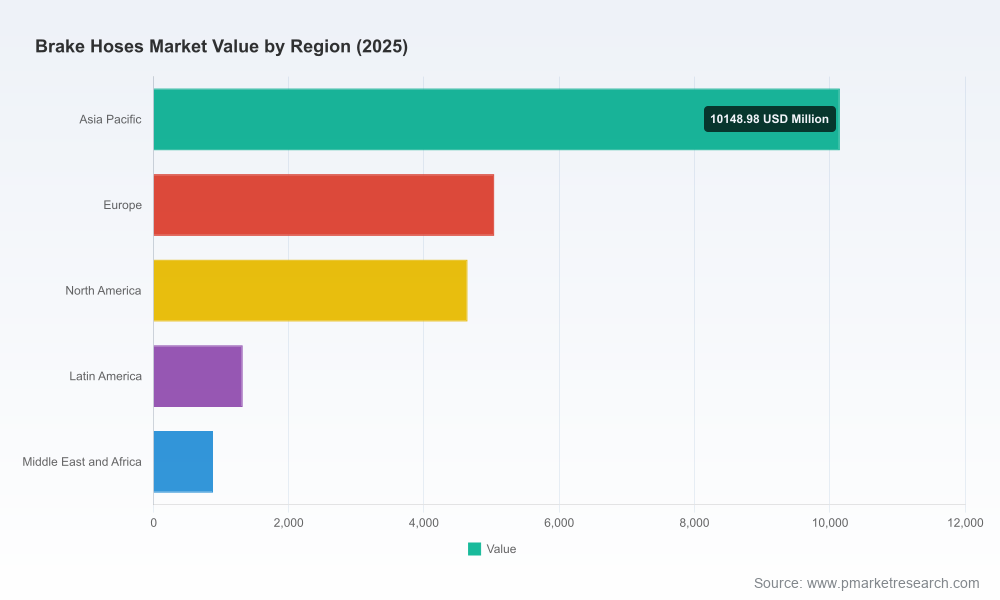

As the Brake Hoses market enters a period of measured growth and technical refinement, PW Consulting’s latest market research brief—anchored on a 2025 base year and a 2026–2032 forecast horizon—distills the actionable intelligence executives need to make high-conviction decisions in 2026. With a projected compound annual growth rate (CAGR) of 4.12% across the forecast window, and a global market size that surpasses USD 22 billion in 2025, the market is neither a niche nor a commodity; it is a strategically resilient component category that links OEM safety mandates, aftermarket reliability, and evolving vehicle architectures.

Brake Hoses Market

Timing: 2026 is a pivotal year for procurement cycles and regulatory recalibrations. Manufacturers and tier suppliers who align sourcing, testing, and certification strategies now will secure multi-year contracts and aftermarket share as fleets and replacement cycles roll forward.

Brake Hoses Market

Risk management: Brake hoses are both safety-critical and regulated. Our brief synthesizes compliance trajectories—FMVSS 106 and SAE J1401 remain the anchors—and translates them into procurement and design checklists that reduce recall and liability exposure.

Brake Hoses Market

Capital allocation: With the market expected to continue expanding toward the latter half of the forecast period, the report equips CFOs and strategy teams with scenario-based revenue and margin outlooks to prioritize investments in testing capacity, material substitution, and regional manufacturing footprints.

PW Consulting’s top-line view shows a steady expansion from the 2025 base toward the end of the forecast horizon. The market’s 4.12% CAGR reflects a blend of underlying demand growth—driven by rising vehicle production in several regions and stricter braking performance requirements—and replacement dynamics in mature markets. Importantly, market concentration is moderate: the top three global players account for just over a third of market share, while the top five approach roughly half the market. This structure supports both scale economics for global suppliers and differentiated niches for specialized players.

OEMs and Tier-1s: Prioritize validated suppliers that combine certified test protocols with traceable raw-material sourcing. The intersection of regulatory rigor and performance expectations favors partners who can demonstrate routine compliance to FMVSS 106 and adherence to SAE J1401 testing regimes.

Tier-2 material suppliers: Synthetic rubber remains the volume backbone of the category. However, suppliers of stainless steel braids, PTFE liners and advanced polymer compounds will see margin uplift as performance and corrosion-resistance demands increase. Diversified material portfolios and just-in-time supply can be competitive differentiators.

Aftermarket players and distributors: Certification and DOT registration are table stakes. Competitive advantage will accrue to aftermarket brands that can combine nationwide supply coverage with documented testing and fitment validation for diverse platforms.

Private equity and investors: The moderate concentration and steady growth create an attractive environment for buy-and-build strategies—particularly in specialty manufacturers with OEM approvals and strong testing capabilities.

The sector’s competitive architecture combines global OEM-oriented groups, specialized hydraulic specialists, and regional players that leverage cost or regulatory first-mover advantages. Our brief includes structured company portraits and strategic diagnostics for the leading names shaping the market:

Nichirin Co., Ltd. — A near-monopoly in its domestic market, Nichirin’s strength is its deep engineering heritage in automotive hoses and its global reach across passenger and two‑wheeler segments. For OEMs requiring high domestic certification and localized engineering, Nichirin’s model informs partnership selection.

Gates Corporation — A diversified industrial player with fluid power competence, Gates integrates brake hose products into a broader portfolio; its scale and cross-application know-how are valuable for platforms that seek standardized supplier interfaces across fluid systems.

Continental AG (including ATE) — Continental’s technology-led approach and high-volume throughput under the ATE brand provide a strong value proposition for OEMs focused on performance margins and thermal/chemical resistance that exceed minimum standards.

Proterial Cable America, Flexitech, COHLINE, and other specialists — These companies exemplify tiered differentiation: custom engineering, regional manufacturing footprints, and certification discipline. They are attractive strategic partners for bespoke systems and complex assemblies.

Sunsong and selected Asian manufacturers — Vertical integration and aggressive aftermarket strategies have yielded regulatory milestones (including DOT certifications) and broad OEM pipelines. Their playbook is instructive for scale entrants aiming to convert aftermarket leadership into OEM wins.

Global hydraulics players (Parker Hannifin, Eaton, Manuli) and component suppliers (Tubes International, LML) — These firms provide breadth in product range and geographic coverage, valuable in multi-system sourcing strategies where single-supplier consolidation is preferred.

PW Consulting’s competitive analysis goes beyond logos. For each firm we map product-technology fit, certification capabilities, manufacturing footprint resilience, and aftermarket distribution strength—enabling sourcing teams to calibrate supplier tiers for safety, cost, and responsiveness.

Regulatory frameworks continue to shape product design and supply-chain decisions. FMVSS 106’s labeling and performance mandates, along with SAE J1401’s test protocols for expansion, burst strength and environmental resistance, create an operational baseline. In practice, many specifications used by OEMs and leading suppliers exceed these standards; therefore, suppliers that proactively test to higher thresholds and maintain transparent DOT registrations will outcompete peers on both OEM and aftermarket platforms.

Our brief includes a compliance playbook: a prioritized checklist of certification steps, sample test matrixes mapped to cost-impact estimates, and recommended audit cadences for manufacturing sites and contract assemblers. For senior managers this translates into a clear roadmap to reduce time-to-qualification for new programs.

Material mix: Synthetic rubber remains the dominant solution due to cost and flexibility. At the same time, stainless-steel braided and PTFE-lined assemblies are gaining share in high-performance, heavy-duty and corrosive environments. Suppliers and OEMs must balance lifecycle costs against performance gains.

Testing and traceability: Digital test records, serialized assemblies and enhanced batch traceability are rising expectations from OEM quality teams and regulators. Investments in automated testing rigs and LIMS (Laboratory Information Management Systems) can shorten qualification cycles and improve warranty outcomes.

Design for EV and ADAS platforms: While brake hose fundamentals remain unchanged, packaging, pedal feel tuning and integration with regenerative braking and advanced driver-assistance systems influence hose routing, fitting types and material selection. Early involvement of hose suppliers in vehicle architecture reviews yields better integration and lower change orders.

This research brief is designed for operationalization. Highlights include:

Top-line forecasts and scenario modeling across 2026–2032, enabling sensitivity analysis for price, volume and regional production shifts.

Supplier scoring frameworks that synthesize certification status, manufacturing resilience, technical capability and aftermarket penetration—presented as decision matrices to accelerate RFQ and supplier consolidation choices.

Regulatory and testing playbooks that map FMVSS 106 and SAE J1401 requirements to supplier audit checklists, sample test plans and expected lead times for certification.

Capital and operational case studies illustrating cost-to-qualify, testing investments and ROI timelines for capacity expansion or material substitution programs.

Sector intelligence on M&A and partnership opportunities, including playbook recommendations for buy-in and bolt-on acquisition targets that accelerate access to OEM approvals or aftermarket channels.

To preserve the strategic edge for our clients, the report follows a “teaser” approach in public summaries: we demonstrate methodology, capability and directional market sizing while reserving detailed segment-by-segment models, supplier scorecards, and actionable price curves for subscribing clients.

Immediate: Validate your supplier list against certified DOT registrants and request documented SAE J1401 test evidence for all shortlisted lines.

Near term (3–6 months): Run scenario modeling for two material mix strategies—baseline synthetic rubber dominance, and a premium variant mix incorporating braided stainless and PTFE—with clear TCO calculations for a three-year horizon.

Strategic (6–18 months): For OEMs and large tier suppliers, negotiate development agreements with at least two global providers to hedge supply risk; for private equity and acquirers, identify specialist manufacturers with strong OEM approvals and testing infrastructure as priority targets.

The Brake Hoses market is a classic industrial ecosystem where regulation, safety-critical performance and incremental technology improvements interact to create steady, high-conviction opportunities. With a market base exceeding USD 22 billion in 2025, a moderate level of concentration among established players, and a forecast trajectory that supports disciplined investment, 2026 is a year for deliberate moves—securing certified suppliers, investing in test and trace capabilities, and aligning materials strategy with vehicle-architecture trends.

PW Consulting’s full brief provides the granular models, supplier scorecards and regulatory playbooks that translate this strategic thesis into operational plans. For executives preparing budgets, RFPs, or M&A strategies in 2026, the brief is built to be directly usable within procurement, engineering, and corporate development workflows.

To review the executive dashboard, scenario models and supplier-specific diagnostics, visit our report page or contact PW Consulting. The public summary is intentionally directional; the client version contains the full quantitative models and supplier benchmarking that enable immediate integration into corporate planning cycles.

For detailed analysis of this topic, please visit the official page:Brake Hoses Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com