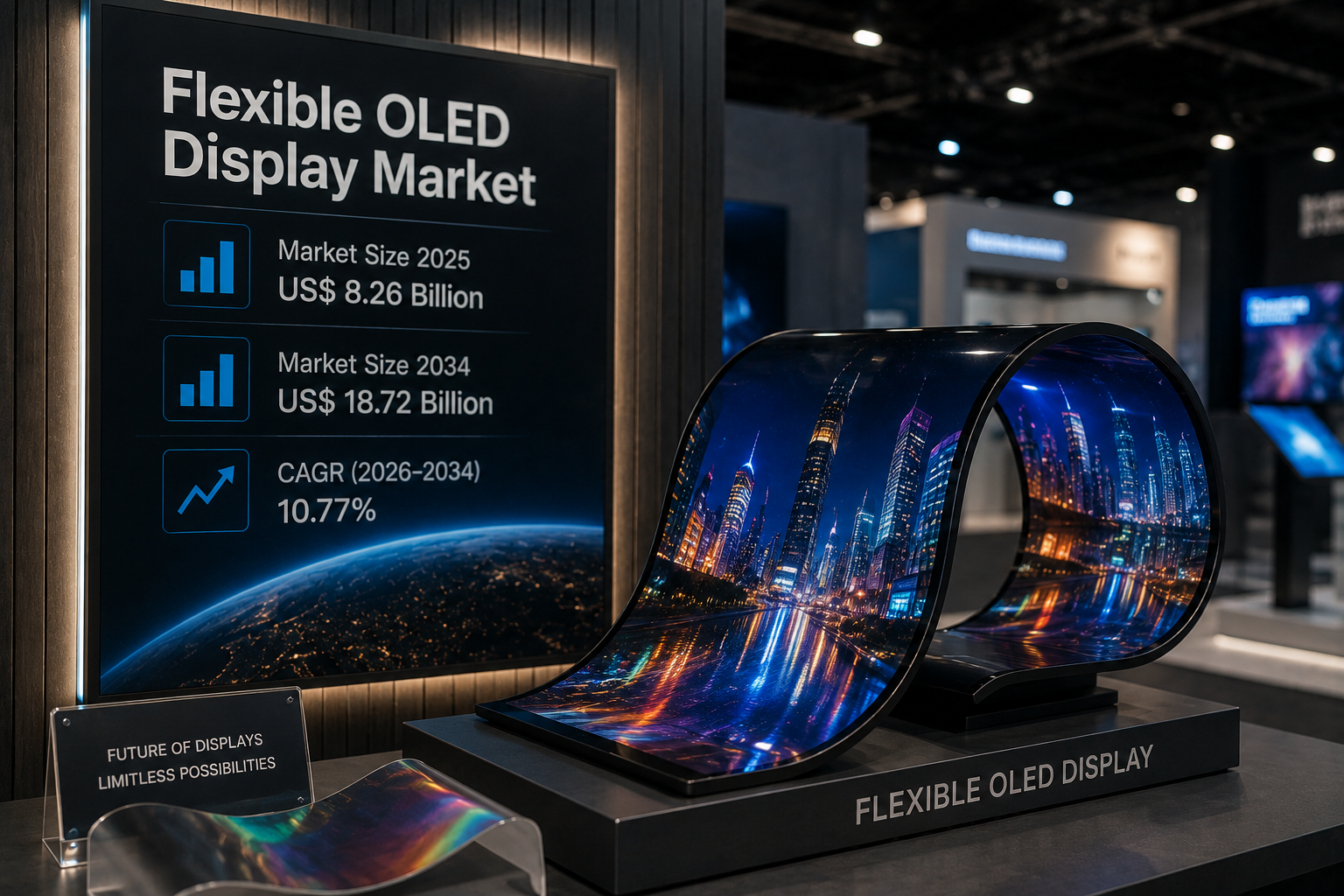

North America Flexible OLED Display Market Size, Share, and Future Growth Opportunities

Technology |

2026-06-24 13:02:13

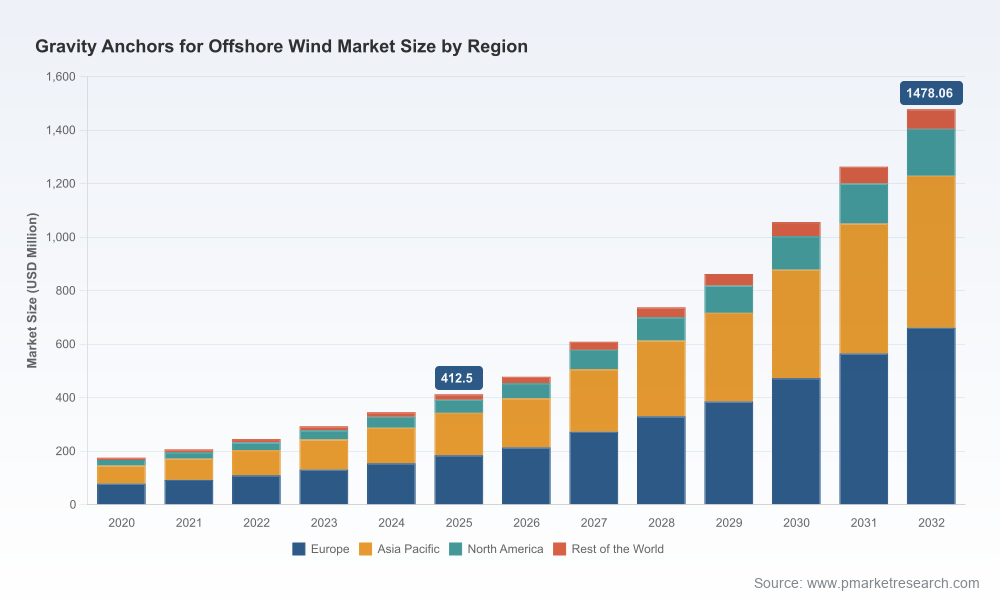

PW Consulting’s new market study, Gravity Anchors For Offshore Wind Market, provides the decision-grade intelligence senior executives need as the industry moves from demonstration to scale. With a base year of 2025 and a seven‑year forecast window running through 2032, our modelling shows the market expanding from an estimated USD 412.5 Million in 2025 to roughly USD 1.48 Billion by 2032 — representing a compound annual growth rate (CAGR) of approximately 20% across the forecast period. Market concentration sits at a moderate level (CR3 ~42%; CR5 ~58%), indicating established lead players alongside substantive space for specialists, new entrants and vertical integrators.

Gravity Anchors For Offshore Wind Market

Policy and procurement calendars are compressing. Projects moving from FID to execution in 2026–2028 will set supply chain footprints for the next decade.

Gravity Anchors For Offshore Wind Market

Raw material and trade dynamics are reconfiguring cost and sourcing strategies — with concrete-centric approaches gaining traction on both cost and emissions metrics, while tariff regimes force localization decisions.

Gravity Anchors For Offshore Wind Market

Technological inflection points (on‑site 3D printing, pumped high‑density ballast, and hybrid designs) are now demonstrably deployable; early adopters will capture unit cost and schedule advantages.

Capital allocation choices made in 2026 — manufacturing CAPEX vs. contract manufacturing, JV vs. licensing, greenfield vs. retrofit — will materially affect LCOE contribution from anchors and moorings.

End‑to‑end market sizing and demand scenarios (base 2025; historical 2020–2025) with sensitivity testing across price, demand cadence and policy scenarios for 2026–2032.

Supply chain mapping and cost build‑ups for mainstream gravity anchor architectures, including breakouts for manufacturing steps, transport logistics and installation economies of scale.

Technology assessment and maturity roadmap, covering traditional slip‑formed concrete, cast iron density strategies, steel‑concrete hybrids, 3D printed concrete and variable‑density pumped solutions.

Competitive due diligence on incumbent and emerging suppliers, with vendor capability matrices, manufacturing footprints, recent deployment case studies and partner fit assessments.

Regulatory and trade risk tracing, including domestic content exposure, tariff impact modelling and recommended de‑risking structures for procurement contracts.

Procurement playbooks, tender readiness checklists and an M&A/partnership evaluation framework targeting value capture levers in manufacturing, logistics and engineering services.

Project‑level anchor selection matrix and decision aids for engineering teams that map seabed type, vessel availability, schedule and cost to optimal anchoring architectures.

Material substitution and emissions pressure: Independent analyses and industry experience show a strategic pivot toward concrete‑dominant designs in many value chains, driven by material cost advantages and lower greenhouse gas intensity compared to steel‑dominant alternatives. This is not universal — technical site constraints and lifecycle maintenance remain decisive — but the net effect is visible in procurement specifications and project bids.

Trade policy and localization: Changes in tariff regimes in early 2025 meaningfully increased duties on imported concrete and steel components, prompting anchor suppliers to pursue dual‑track manufacturing strategies. For 2026 planning, firms must weigh the economics of localized production versus tariff‑protected imports and incorporate these scenarios into supplier selection and brownfield/greenfield manufacturing investments.

Seabed and system engineering constraints: Anchor choice remains fundamentally dependent on seabed characteristics. Gravity anchors retain clear technical advantages in particular geologies and depths, but they are one option among suction, driven piles and drag‑embedment systems. The practical implication for project teams is tighter integration required between site survey, mooring design and commercial proposals.

Scale effects and logistics: Gravity solutions are material‑intensive. Large projects require industrialized manufacturing, proximate quayside capacity and specialized heavy‑lift operations. Early investment in port facilities or long‑term manufacturing partnerships can yield meaningful schedule and cost benefits as annual installed capacity grows.

The market is populated by specialized engineering houses, material specialists and innovative technology startups. Our competitive mapping highlights five representative firms and their strategic trajectories:

Offshore Wind Design AS (Norway) — Focuses on standardized gravity anchor solutions for TLP and semi‑submersible floating foundations, often delivered as full EPC packages. Their integrated offering — encompassing system engineering, geotechnical evaluation and on‑site delivery — targets large‑scale projects where single‑vendor accountability reduces interface risk.

FMGC (Farinia Group, France) — Specialist in high‑density cast iron gravity anchors and clump weights. Their differentiation is material density optimization to reduce transported mass and installation cost per unit holding capacity — an attractive value proposition where marine transportation costs dominate.

Sperra (RCAM Technologies, USA) — Brings 3D concrete printing to gravity anchors, enabling near‑site manufacturing and reduced concrete volumes. Notably, Sperra achieved a full‑scale deployment milestone in March 2026 at a Portuguese floating renewables test site — a practical proof point for on‑site fabrication strategies that can compress logistics chains and localize jobs.

Aubin Oceanatics (UK) — Offers variable‑density, pumpable ballast systems enclosed in pyramid‑shaped steel shells. This modular, adaptable approach promises versatility across seabed types and depths, reducing the need for bespoke castings.

Triton Anchor (USA) — Provides innovative helical and non‑penetrative anchoring systems suited to a range of mooring configurations. Their low‑noise, rapid‑install designs appeal to projects with strict environmental and schedule constraints.

Complementary industry reporting (e.g., a November 2025 Geostrata feature) underscores anchoring as a core technical and economic challenge for floating wind projects, positioning gravity anchors as a mature, widely considered option among several viable approaches.

Adopt a dual‑track manufacturing strategy: Preserve optionality by qualifying both localized and centralized manufacturing routes. Use tariff and sensitivity modelling to determine the breakeven for brownfield investments versus contract manufacturing. This reduces regulatory and supply disruption risk while enabling competitive tender responses.

Run early pilots with high‑potential technologies: Prioritise one or two pilots for 3D‑printed concrete or variable‑density pumped ballast to validate cost, schedule and environmental claims under live conditions. Demonstrations de‑risk downstream procurement and create IP capture opportunities.

Negotiate outcome‑based contracts with suppliers: Shift from pure CAPEX bids to cost‑per‑installed‑unit or cost‑per‑tonne‑of‑holding‑capacity frameworks to align incentives on weight reduction, install time and life‑cycle performance.

Integrate seabed intelligence into commercial bids: Tie site survey outputs directly to tender pricing models to avoid scope creep and late change orders. Where uncertainty exists, embed contingency tranches and decision gates linked to geotechnical milestones.

Hedge feedstock exposure: For projects where concrete volumes dominate, secure long‑term aggregates and cement supply contracts while exploring low‑carbon cement alternatives to meet ESG targets without sacrificing cost competitiveness.

Use M&A and JV selectively: Acquire or partner with niche technology providers to accelerate time‑to‑market for advanced anchor systems; alternatively, pursue joint ventures with local fabricators to meet domestic content requirements efficiently.

Embed regulatory engagement in project timelines: Early dialogue with authorities on domestic content rules and environmental constraints will reduce permit risk and enable preferential procurement outcomes.

PW Consulting supports clients across strategic planning, supplier selection, and program execution for gravity anchors and broader mooring systems. Our services include: bespoke cost models and LCOE sensitivity analyses; supplier due diligence and commercial negotiation support; port and logistics feasibility studies; on‑site manufacturing feasibility and site selection; and transaction support for M&A and joint ventures. The report is complemented by a downloadable dataset and vendor dossiers that provide the granular segmentation and regional breakdowns necessary to execute procurement and investment decisions — intentionally gated so that public summaries build confidence while the full intelligence remains within the report package.

2026 will be the year of execution choices. With a rapidly growing market trajectory and multiple technology pathways maturing simultaneously, companies that align procurement, manufacturing and technology strategies now will secure outsized advantages in cost, schedule and environmental performance. PW Consulting’s Gravity Anchors For Offshore Wind Market equips leaders with the scenario‑tested, commercially actionable insights required to convert market growth into sustainable enterprise value.

For detailed analysis of this topic, please visit the official page:Gravity Anchors For Offshore Wind Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com