Preeclampsia Therapeutic Market 2026: Strategic Imperatives from PW Consulting’s New Market Report

PW Consulting’s latest Preeclampsia Therapeutic Market report—anchored on a 2025 base year and a 2026–2032 forecast horizon—arrives at a moment of inflection for developers, investors, payors and health systems. With a data-driven foundation and scenario-ready deliverables, the study translates a complex clinical and regulatory landscape into actionable choices that will determine which programs accelerate in 2026 and which face mounting commercial and access obstacles.

Preeclampsia Therapeutic Market

Why this report matters for 2026 decision-making

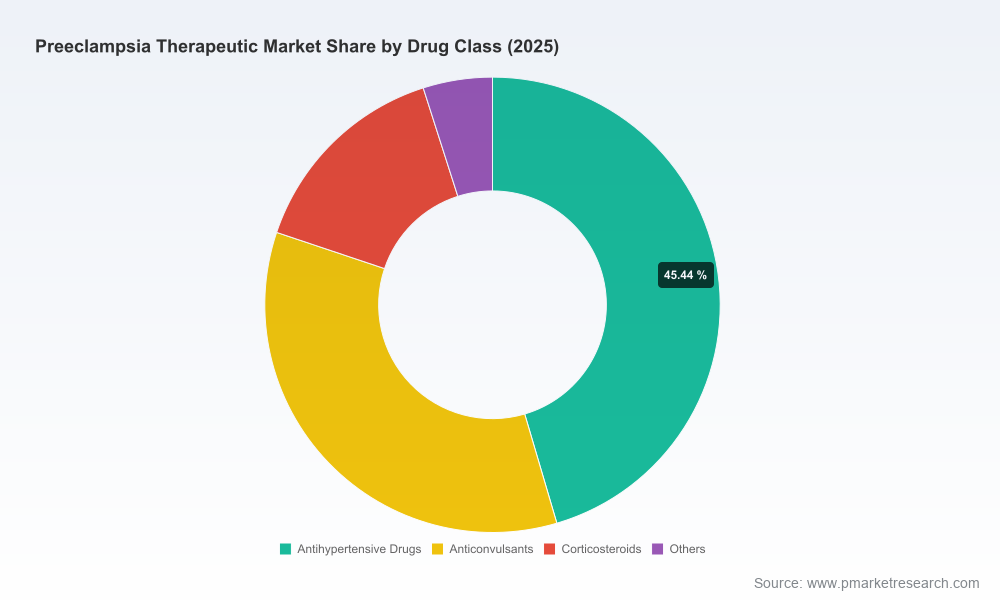

- The market for preeclampsia therapeutics has moved from fragmented clinical activity into measurable commercial potential: PW Consulting’s topline model projects steady expansion from a 2025 market size of USD 1,286.1 Million to an estimated USD 1,795.15 Million by 2032, reflecting a compound annual growth rate (CAGR) of approximately 4.88% over the forecast period.

- These headline numbers mask a fast-evolving therapeutic pool—novel biologics, RNA agents, targeted protein replacements, device-enabled apheresis and AI-derived small molecules—which are creating new value pools but also elevating development, regulatory and reimbursement complexity.

- Our report is engineered to convert that complexity into strategy: it gives executives the situational awareness and playbooks needed to prioritize assets, structure partnering terms, and design market-entry sequences in 2026 that align with regulatory windows and payer expectations.

Market trajectory and what the numbers imply

Historical modeling in the report spans 2020–2025, and documents recovery and renewed investment in the space following episodic volatility. PW Consulting’s aggregation shows an increase in total market throughput from the low thousands of USD (Million) at the start of the decade to a 2025 base of USD 1,286.1 Million. From this base, the forecast to 2032 quantifies the aggregate commercial opportunity and, critically, the timelines by which novel, disease-targeting therapeutics could shift standard-of-care economics.

Preeclampsia Therapeutic Market

For strategy teams, the 4.88% CAGR is actionable: it implies meaningful, but not runaway, expansion—favoring disciplined R&D spend, selective regional launches, and staged manufacturing scale-up rather than broad upfront commercialization investment. Our scenario modules translate topline growth into timing vectors that account for regulatory milestones, clinical readouts and payer adoption curves.

Preeclampsia Therapeutic Market

Competitive landscape: who to watch

The therapeutic pipeline is diverse. Our competitive assessment synthesizes corporate positioning, scientific differentiation, regulatory progress and likely partnership trajectories without disclosing sensitive, segment-level data reserved for report subscribers.

- DiaMedica Therapeutics (Minneapolis) is among the most advanced developers in the early-onset preeclampsia segment. Regulatory interactions in late 2025 and early 2026—culminating in a productive pre-IND meeting with the US FDA and Health Canada Phase 2 clearance—make its recombinant protein candidate a bellwether for how regulators will evaluate disease-modifying approaches for pregnant populations.

- RNA and oligonucleotide innovators such as Comanche Biopharma are pursuing siRNA strategies targeting pathogenic transcripts. These approaches carry differentiated safety and delivery considerations but—if clinical validation occurs—may re-shape how payors and maternity networks think about intervention timing.

- Biologics and protein-replacement programs (multiple entrants) are competing on target specificity and manufacturability. Programs advancing to mid-stage development will test commercial assumptions about dosing frequency, cold-chain requirements and outpatient versus inpatient administration.

- Device and platform approaches (including targeted apheresis technologies) present alternative commercialization pathways—often aligned to tertiary care centers and high-acuity referrals—where pathway economics differ from outpatient pharmaceutical launches.

- Regional and multinational pharma players are active, and the report profiles the likely partnership plays between small innovators and established manufacturers capable of scaling complex biologics or delivery systems.

PW Consulting’s competitive concentration assessment highlights a market that is neither atomized nor highly consolidated—aggregate concentration ratios reveal meaningful presence of a few leading players but leave ample room for disruptive entrants to capture share through differentiated clinical data or superior access strategies.

Recent milestones that reframe 2026 planning

- Regulatory momentum: DiaMedica’s December 2025 pre-IND engagement with the FDA and Health Canada’s Phase 2 clearance in early 2026 indicate that regulatory pathways are navigable—albeit requiring targeted non-clinical work and robust maternal-fetal safety data.

- Diagnostics enabling risk stratification: regulatory approvals for sFlt-1/PlGF ratio testing in certain jurisdictions are improving the ability of health systems to identify high-risk patients earlier, which in turn changes the addressable market for disease-modifying therapeutics.

- Academic and philanthropic activity: clinical trials funded through nontraditional sources (e.g., foundation grants) are accelerating translational studies of adjunctive agents aimed at vascular function—introducing new combination strategies that commercial teams must consider.

Dynamics and risk factors that will determine winners

Four dynamics dominate the risk–reward calculus and are modeled extensively in the report:

- Standard-of-care inertia: current management relies heavily on repurposed antihypertensives and magnesium sulfate for seizure prophylaxis; delivery remains the definitive intervention. Any new therapeutic must demonstrate clear maternal and fetal benefit or a markedly improved safety/tolerability profile to shift practice.

- Supply chain fragility: documented stock-outs of critical commodities and manufacturing constraints in low- and middle-income settings underscore the need for resilient supply strategies and flexible manufacturing footprints when planning global launches.

- Regulatory scrutiny of pregnancy therapeutics: regulators demand rigorous maternal–fetal safety data and, increasingly, post-approval evidence generation plans—raising the cost and time-to-market compared with non-pregnant indications.

- Reimbursement and access complexity: payors will demand outcome-linked evidence and will factor comparators (including low-cost, WHO-recommended agents) into coverage decisions. Early payer engagement and real-world evidence designs are indispensable in 2026.

What’s inside the report: operational modules for 2026

PW Consulting’s report is deliberately practice-oriented. Subscribers will receive:

- Topline market sizing (USD, Million) with historical context (2020–2025) and granular scenario forecasts through 2032, including sensitivity to regulatory and clinical readout timing.

- Regulatory pathway maps and a recommended pre-IND and Phase 2/3 engagement playbook tailored to maternal–fetal risk considerations.

- Partner and licensing matrix that aligns scientific differentiation with likely commercial partners and manufacturing capabilities—structured to support term negotiations in 2026.

- Go-to-market sequencing models that translate forecasted demand into launch prioritization, capacity ramp scenarios and pricing/reimbursement strategies across payer archetypes.

- Real-world evidence templates and post-approval study designs that anticipate payor requirements and mitigate uptake risk.

- Supply-chain resilience assessment and supplier due-diligence checklists emphasizing continuity for critical compounds and cold-chain-dependent biologics.

Strategic imperatives for executives planning in 2026

Drawing from our analysis, PW Consulting recommends five priorities for decision-makers preparing 2026 roadmaps:

- Align clinical portfolio risk with capital availability: prioritize programs with the clearest regulatory pathway and the most compelling maternal–fetal benefit–risk profiles for near-term investment.

- Design staged partnerships: use milestone-based partnerships and co-development terms to share clinical and commercialization risk while retaining upside for high-value indications.

- Invest in diagnostics-linked strategies: pair therapeutic development with diagnostic adoption plans to accelerate appropriate patient identification and create a differentiated commercial value proposition.

- Operationalize access early: develop differentiated LMIC access models that mitigate supply-chain fragility and recognize the role of low-cost standard agents in payer decisions.

- Prepare robust post-market evidence programs: embed real-world outcomes measurement into trial design to shorten payer negotiation cycles after approval.

Next steps and how the report can be used

PW Consulting’s Preeclampsia Therapeutic Market report is designed as both an intelligence brief and an execution playbook for 2026. It balances macro market sizing (in USD, Million) and concentration indicators with practical toolkits that translate insights into boardroom decisions. Importantly, while this press summary surfaces the critical trends and competitive narratives, the full report contains the segment-level models, regional go-to-market permutations and interactive financial outputs that strategy teams need to finalize investment and partnership decisions.

Executives seeking to operationalize their 2026 strategies should use the report to: run internal “launch/no-launch” decision workshops; calibrate capex and clinical budgets to forecasted commercial timelines; and design partnering term sheets that reflect regulatory and reimbursement realities in pregnancy therapeutics.

Conclusion

The preeclampsia therapeutics landscape in 2026 sits at a rare juncture: scientifically promising programs are converging with clearer regulatory touchpoints and improved diagnostic stratification, yet systemic hurdles—supply-chain fragility, payer skepticism and maternal–fetal safety expectations—remain pronounced. PW Consulting’s report does not prescribe a single path to leadership; rather, it arms strategy teams with the market sizing, risk frameworks and operational playbooks needed to make defensible choices. For teams that move with discipline and purpose in 2026, the next seven years offer tangible commercial and clinical upside.

To access the full set of models, interactive scenario tools, and the proprietary segmentation data that underpin these insights, please visit the report landing page and download the executive package.

For detailed analysis of this topic, please visit the official page:Preeclampsia Therapeutic Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com