Construction Site Dumper Market 2026: Strategic Imperatives from PW Consulting’s New Industry Brief

PW Consulting today releases a strategic industry brief that distills the implications of our full Construction Site Dumper Market report for executive decision-making in 2026. Combining rigorous market-sizing with actionable playbooks, the brief is designed as an operational guide for OEMs, component suppliers, rental fleets, infrastructure contractors, and private equity investors who need to translate market signals into concrete commercial moves this year.

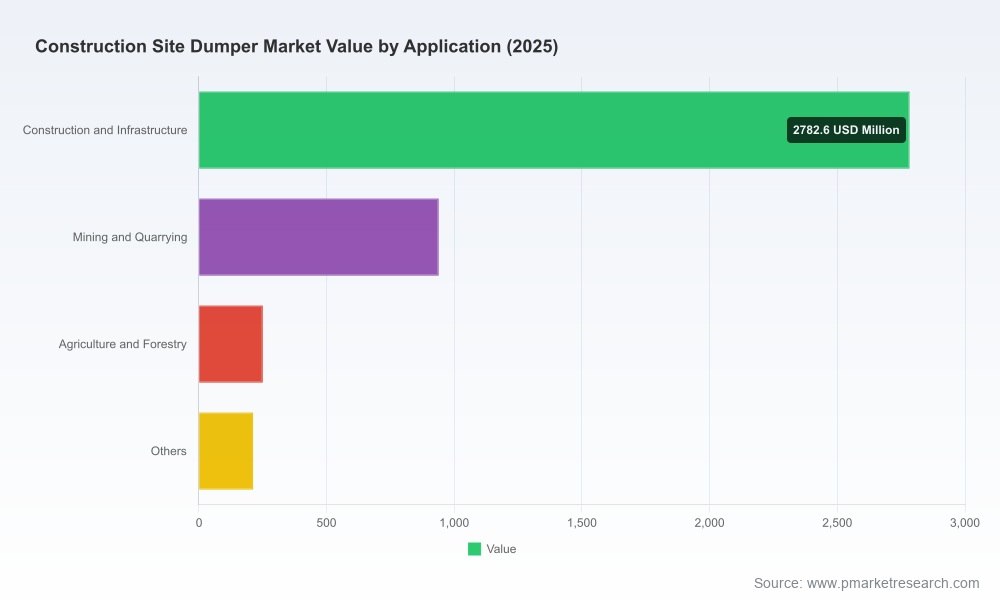

Construction Site Dumper Market

Market snapshot: growth trajectory and what it means for 2026 planning

After a period of steady expansion from 2020 to 2025, the global construction site dumper market reached an estimated USD 4,185.0 Million in 2025. Our forecast through 2032 projects continued expansion, reaching roughly USD 6,244.0 Million by 2032 — reflecting a compound annual growth rate (CAGR) of approximately 5.85% over the 2026–2032 horizon. That pace represents a structural recovery and modernization cycle in earthmoving and site logistics equipment: demand is reinforced by urban infill projects, a renewed push in infrastructure spending in several large markets, and growing adoption of electrified and compact machines for constrained sites.

Construction Site Dumper Market

For 2026 specifically, decision‑makers should treat the market at two levels: steady top‑line expansion that creates runway for new product investment, and near‑term cost pressures that compress margins unless actively managed. The report’s blended market scenarios translate these macro dynamics into financeable options for capital allocation, product timing, and supply-chain hedging.

Construction Site Dumper Market

Key dynamics shaping 2026 decisions

- Raw material and input-cost volatility: Recent swings in steel and aluminum prices have re-priced mid-sized dumpers, with observed producer-price effects pushing unit prices upward in 2026. The combination of commodity swings and tariff regimes in major markets has made single-source cost assumptions untenable.

- Policy and trade headwinds: Persistently high import tariffs on steel and aluminum in some jurisdictions have amplified the domestic-cost differential for OEMs that import key subassemblies or raw inputs — a factor that materially affects sourcing and regional manufacturing footprints.

- Product electrification and site electrics: OEMs continue to launch electric and hybrid site dumpers aimed at urban and constrained projects, while telematics and safety features climb the priority list for contractors who value uptime and site visibility.

- Fleet economics and rental demand: Rental houses and contractors are increasingly focused on total cost of ownership (TCO) and lifecycle uptime. This drives appetite for machines that are easier to service, that come with data-assisted maintenance, and that can be redeployed across multiple job types.

- Consolidation and competitive intensity: A mid-consolidation structure means there is space for niche specialists and large OEMs to coexist. Strategic partnerships, selective aftermarket expansion, and bolt-on M&A are the expected moves in 2026.

What the report contains — practical, transaction-ready guidance

PW Consulting’s full report is structured to be used, not merely read. Highlights include:

- Proven market-sizing methodology and scenario frameworks that model upside and downside demand through 2032.

- Supply‑chain stress tests and raw‑material sensitivity analyses to quantify margin exposure under alternative commodity and tariff outcomes.

- Product portfolio and go‑to‑market playbooks, including electrification roadmaps, modular‑platform strategies, and pricing levers for different fleet buyers.

- Operator and rental-fleet TCO templates that isolate service, parts, and downtime contributions to unit economics.

- Commercial due‑diligence checklists for M&A and JV discussions tailored to site dumper assets and component suppliers.

- A pragmatic five-year investment prioritization matrix — balancing R&D, capacity expansion, and aftermarket buildout for 2026 capital planning cycles.

These sections are designed to be actionable for CFOs, heads of product, VP sales, and private equity teams planning investments or divestitures in 2026.

Competitive landscape — strategic profiles and recent moves

The market is shaped by a mix of long‑standing family manufacturers, diversified OEMs, and global heavy-equipment players. Our analysis focuses on the competitive positioning, capability gaps, and near-term strategic levers of market-leading firms.

- Thwaites Limited (Leamington Spa, UK): A family-owned specialist with deep product breadth across site dumper sizes and an accelerating push into electric and rotator variants. Their late‑2025 factory expansion increases production capacity materially, an explicit bet on higher volume and faster product refresh cadence.

- Wacker Neuson (Munich, Germany): A technology-forward contender emphasizing visibility and operator ergonomics. The 2025 launch of a Dual View 12.5‑tonne model signals an attempt to stretch into higher payload segments while preserving site maneuverability advantages.

- JCB (Rocester, UK): A full‑line construction OEM that is applying its scale to safety, electrified urban models, and integrated service packages. JCB’s product strategy centers on modular features and branded safety systems to capture rental and contractor preference.

- Mecalac (Annecy, France): A niche specialist for compact, swivel‑chassis applications in confined urban sites, leveraging compactness and operator productivity as defensible differentiators.

- Bergmann Maschinenbau (Meppen, Germany): A focused supplier of wheeled and tracked compact dumpers, with increasing attention to electric drivetrains for mining and specialty sectors.

- Caterpillar Inc. (Irving, Texas, USA): The large-cap generalist that competes through large-capacity articulated solutions and an expansive aftermarket network — relevant to contractors prioritizing capacity and productivity on large civil works.

Recent company initiatives — factory expansions, new model introductions, and electrification previews — are not isolated product news; they reflect strategic responses to cost pressure, urban demand, and rental-fleet economics. For example, capacity increases should be read as a defensive move to secure lead times in a market where raw‑material volatility can quickly create supplier bottlenecks.

Immediate implications for 2026 strategies

Based on our scenarios and supplier interviews, PW Consulting recommends that decision-makers focus on the following priority actions in 2026:

- Hedge procurement exposure: Establish multi‑tier sourcing agreements and indexed pricing clauses for steel, aluminum and key electronic components to stabilize margins.

- Reconsider manufacturing geography: Run small-scope footprint simulations to determine whether regional assembly cells or expanded local content will offset tariff and logistics volatility.

- Accelerate product modularization: Prioritize architectures that permit rapid variants (electric, cabbed, swivel) from common platforms to reduce R&D cost per SKU.

- Monetize telematics and uptime: Introduce data‑driven uptime guarantees and service subscriptions for rental customers to capture aftermarket margin pools.

- Re‑price for component inflation: Avoid across‑the‑board rebates; design contract structures that share commodity swings with buyers while protecting margin floors.

- Targeted M&A and partnerships: Seek bolt-on acquisitions that add electrification capability, battery systems know‑how, or local assembly presence in tariff‑sensitive markets.

- Operational readiness: Build a 12–18 month parts‑availability roadmap and prioritized CAPEX plan aligned to forecasted fleet utilization scenarios.

Risk matrix — what to watch in 2026

- Commodity shocks: Larger-than-expected steel or aluminum price spikes will disproportionately affect mid-sized dumper margins unless contracts are hedged.

- Trade policy shifts: Tariff escalations or sudden relaxations can create abrupt swings in regional competitiveness for imported modules.

- Technology adoption lag: Slower customer acceptance of electric dumpers could leave early entrants with underutilized investments unless they secure rental-channel commitments.

- Aftermarket service gaps: Inadequate parts availability or telematics capabilities will constrain rental house uptake and extend payback periods.

Why PW Consulting’s brief is decision-ready for 2026

Clients tell us they need two things this year: (1) fast, defensible market sizing to allocate 2026 capital and (2) pragmatic execution tools to preserve margin while capturing growth. Our report combines a transparent forecasting methodology with templates and playbooks that translate market figures into procurement terms, product‑development priorities, and M&A screening criteria. It is intentionally structured as a “how‑to” companion for the boardroom and the planning team.

To preserve the competitive value of the full analysis we present this brief as a high‑signal trailer: it reveals the strategic direction and the scenarios executives must plan for, while the granular regional and application splits, detailed supplier profiles, and downloadable TCO models are reserved for the full report.

Next steps

- For OEMs and suppliers: use the supplier stress tests and TCO templates to re-run 2026 budgets with commodity- and tariff‑stress assumptions.

- For fleets and rental operators: request the operator-facing modules to calculate replacement and electrification ROI under your utilization profile.

- For investors: leverage the M&A due‑diligence checklist and the four prioritized buy-and-hold scenarios to size potential transactions and exit horizons.

Access to the full Construction Site Dumper Market report, including the proprietary regional and product split tables, supplier scorecards, and downloadable financial templates, is available through PW Consulting’s report page. For tailored briefings and scenario workshops to inform your 2026 strategy, PW Consulting’s industry practice is available to conduct bespoke sessions and model the outcomes under client-verified assumptions.

For detailed analysis of this topic, please visit the official page:Construction Site Dumper Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com