Anti-Drone System Market 2026 — Strategic Intelligence Briefing

PW Consulting’s latest market intelligence on Anti-Drone Systems delivers a focused, executable perspective for executives making acquisition, investment, and technology decisions in 2026. This briefing summarizes the report’s strategic value, highlights the macro trajectory of the market, and outlines the operational tools and competitive insights that corporate and public-sector leaders need to navigate an environment of accelerating demand, heightened regulation, and rapid technological change.

Anti Drone System Market

Executive snapshot: why 2026 is an inflection year

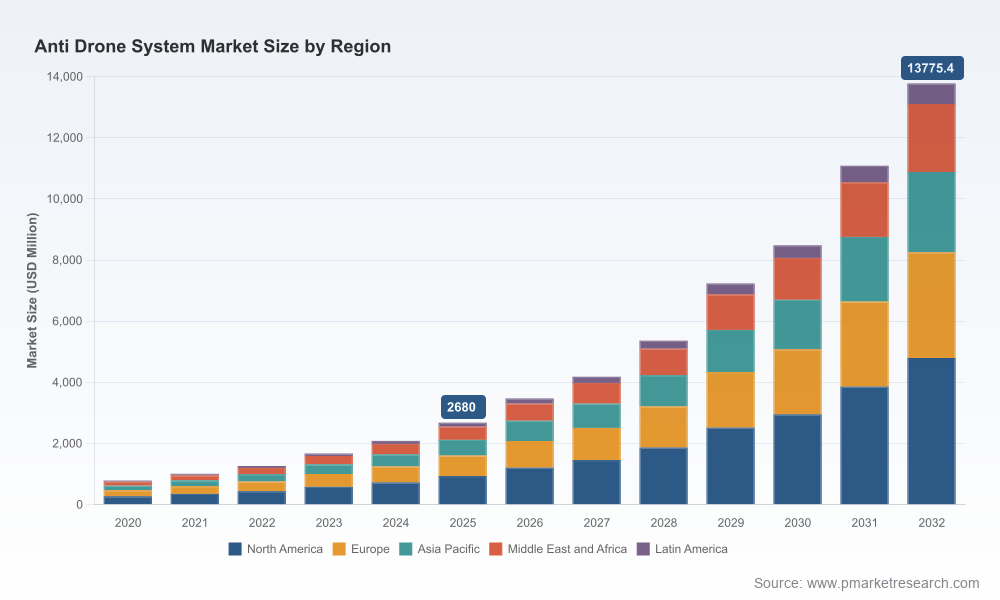

The anti-drone sector has moved from niche force-protection applications to a cross‑domain, high-priority capability set for defense, homeland security, and critical infrastructure operators. PW Consulting’s analysis shows the market expanding from roughly USD 2.68 billion in 2025 to an expected USD 13.78 billion by 2032, reflecting a compound annual growth rate of 26.35% across the 2026–2032 forecast window. This trajectory is driven by three converging forces: proliferation of low-cost unmanned aerial systems (UAS) in conflict and criminal activity, accelerated procurement and operationalization by government agencies, and rapid maturation of sensor-fusion, electronic warfare, and directed-energy solutions.

Anti Drone System Market

What this means for buyers, operators, and investors

- Risk-to-reward calculus is time-sensitive. Organizations that finalize validated requirements and phased procurement plans in 2026 will capture outsized value: early deployments reduce exposure and create data that informs future capability upgrades in a market growing at >25% annualized rates.

- Layered architectures are the durable default. Single-mode solutions are increasingly ineffective against blended threat sets. Buyers should budget for sensor fusion (radar, RF, EO/IR), classification pipelines (AI/ML), and multiple defeat options (soft-kill, nets, directed energy, and kinetic) within a unified command and control construct.

- Standards and testing will shape winners. NATO’s new testing capability and the Pentagon’s standardized test guidelines are reducing technical ambiguity; suppliers who demonstrate compliance and repeatable performance across test regimes will unlock larger, multi-domain procurements.

Report contents — practical, procurement-ready intelligence

PW Consulting’s full report is designed as an operational playbook for decision-makers. It distills primary research, proprietary model outputs, and practitioner interviews into a set of deliverables you can apply immediately:

Anti Drone System Market

- Market sizing and validated forecasting model (historical 2020–2025, base year 2025, forecast 2026–2032) with scenario toggles for procurement volume, technology adoption rates, and geopolitical escalation.

- Vendor scorecards and capability maps that evaluate detection, classification, attribution, and defeat across performance, integration risk, sustainment cost, and export-control profile.

- Technical reference: sensor-fusion patterns, EW risk matrices, directed-energy readiness timelines, and cost drivers for kinetic vs. non-kinetic effectors.

- Procurement playbook: statement of requirements templates, sample RFP language, test and evaluation (T&E) checklists aligned to emerging NATO/JIATF standards, and contracting strategies for layered procurements.

- Operational playbooks: force-protection deployment patterns, airspace integration guidance with civil aviation authorities, privacy and lawful-interception compliance frameworks, and incident-response runbooks for urban and remote sites.

- Investment and M&A framework: valuation drivers, integration risk checklists, and diligence templates tailored to software‑heavy platforms and hardware‑heavy systems.

To respect the “trailer” principle of this release, the report showcases the analysis and the tools above while withholding the granular segment tables and region-by-application breakouts that subscribers access on the report page. This ensures prospective buyers can validate fit against their mission before unlocking the detailed datasets.

Competitive landscape — what to watch in 2026

The anti-drone market exhibits moderate concentration: the top-three suppliers account for a meaningful minority of market revenues, and the top-five push toward a majority share. This structure creates room for both incumbent defense primes and specialized entrants to capture share through differentiated offerings and partnerships.

- Prime defense integrators (e.g., RTX, Lockheed Martin, Northrop Grumman). These firms leverage scale, battle-tested radar and effector portfolios, and prime-contractor relationships to win large system-level procurements. Their advantage is systems integration at platform and force-protection scale, and their roadmaps increasingly include high-energy laser components and AI-enabled C2 layers.

- Tiered international integrators (e.g., Thales, Leonardo, Saab). Strong in multi-sensor fusion and international export markets, these vendors win governmental modernization programs where interoperability, NATO compliance, and modularity matter.

- Specialist technology firms (e.g., Dedrone, DroneShield, D‑Fend, Fortem). These companies drive innovation in software-defined detection, RF-cyber mitigation, and autonomy-enabled capture systems. Their speed of iteration and software-first models make them attractive for critical infrastructure and event security integrators.

- Systems and sensing innovators (e.g., IAI, Rafael, Liteye, Blighter, SRC). Suppliers with operational combat heritage or unique radar/IP portfolios can displace incumbents in theater-specific procurements and in markets preferring localized production or technology transfer.

Partnerships and coalition-focused offerings will be decisive. Expect to see more prime-specialist alliances where large contractors wrap sustainment and compliance guarantees around niche detection and mitigation modules.

Regulatory and standardization tailwinds

Regulation and test‑and‑evaluation developments in early 2026 create a clearer operating environment for procurement and deployment:

- Updated enforcement policy from civil aviation authorities raises the cost of non-compliant drone operations and tightens the legal context for defense-in-depth measures near critical airspace.

- U.S. federal agencies have clarified acquisition pathways and authorities for counter‑UAS, and new program offices are aligning funding toward high-visibility events and national infrastructure protection.

- NATO’s testing ranges and the Pentagon’s standardized test guidance are beginning to harmonize performance baselines, which shortens procurement cycles for vendors who can demonstrate compliance.

These developments reduce acquisition risk for buyers who require demonstrable, standards-aligned performance, and they increase barriers to entry for suppliers who cannot meet the emerging T&E bar.

Strategic playbook for 2026 decisions

PW Consulting recommends practitioners adopt a three-track approach when making decisions this year:

- De-risk core operations: Rapidly field proven layered solutions to protect high-value assets and events. Use modular procurements that allow capability inserts as technologies mature.

- Experiment in constrained pilots: Run two to four controlled pilots focused on interoperability and sustainment economics. Use NATO/JIATF test protocols to validate real-world performance and to collect evidence for scaling.

- Capture optionality through partnerships: Negotiate supply agreements that include technology refresh windows, data‑sharing clauses, and export/transfer flexibility to adapt to geopolitical shifts.

For investors and M&A teams: prioritize firms with defensible IP in AI-driven detection/classification, proven T&E performance, and clear pathways to recurring revenue (software subscriptions, analytics, sustainment). For system integrators: prioritize relationships that close capability gaps in defeat options and reduce lifecycle sustainment risk.

Recent market signals to monitor

- NATO’s new counter-drone testing activities in Latvia mark the start of multi-national T&E regimes that will influence procurement specs across allied nations.

- U.S. federal action, including new program offices and directed funding for major events, is accelerating short-term demand cycles and day‑of-event deployments.

- Significant private funding rounds and large defense contract awards in 2025–2026 indicate capital flows into long-range radar, AI analytics, and effector platforms—signals of both supplier consolidation and technology specialization.

Next steps and how the report helps

PW Consulting’s full Anti-Drone System Market report provides the detailed data tables, regional and application segmentation, vendor financial and capability benchmarking, and the procurement templates referenced in this briefing. The public summary you are reading is intentionally selective—designed to demonstrate analytical depth and immediate applicability while directing decision-makers to the source report for the granular datasets and proprietary models required for contract-level or investment decisions.

If your organization needs a tailored briefing, a procurement-readiness assessment, or an investor diligence package aligned to the 2026 regulatory and testing landscape, PW Consulting’s advisory teams are available to convert the report’s findings into executable programs of record.

For detailed analysis of this topic, please visit the official page:Anti Drone System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com