Double Fed Wind Turbine Market: Strategic Imperatives for 2026 — PW Consulting Market Report Preview

PW Consulting today releases an executive preview of our forthcoming Double Fed Wind Turbine Market report — an operationally focused intelligence product designed to shape capital, procurement and technology decisions across 2026. Built on a 2020–2025 historical baseline and incorporating forward-looking scenarios across a 2026–2032 forecast horizon, the study quantifies the macro trajectory of the double-fed (DFIG / Type III) ecosystem and translates that trajectory into pragmatic, prioritised actions for operators, OEMs, investors and utilities.

Double Fed Wind Turbine Market

Market Trajectory: What the Macros Say

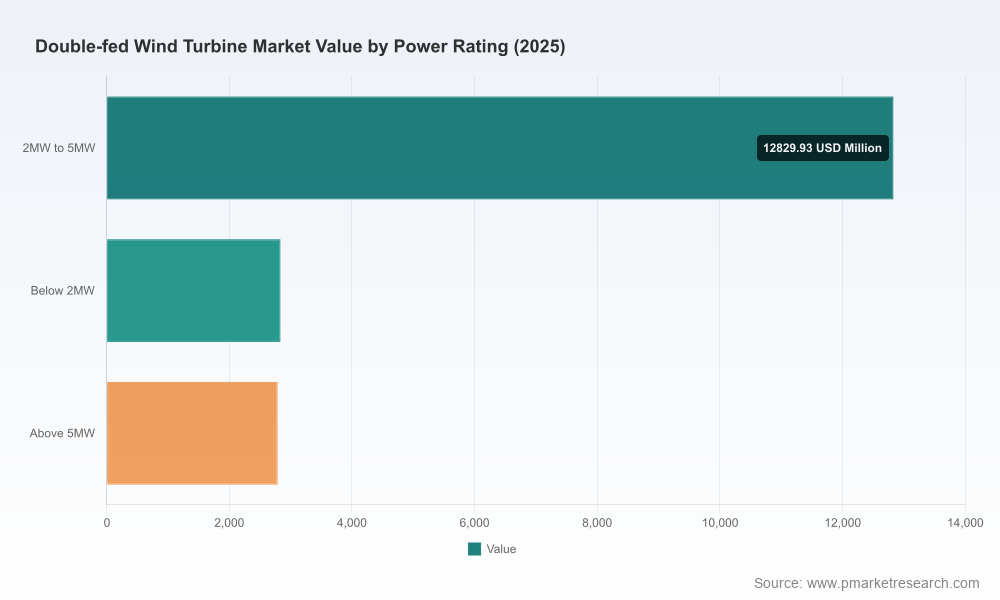

The global double-fed wind turbine market has demonstrated steady expansion through the mid-2020s and, in our base-case scenario, continues to grow at a compound annual growth rate (CAGR) of 5.25% across the 2026–2032 forecast period. Measured on a revenue basis (Million USD), the market size reached approximately 18,450 in the base year (2025) and our modelling points to a market approaching the mid-20 billions by the end of the forecast window. These aggregates capture both new-build demand and, crucially, an uptick in repowering activity where mature fleets are being replaced with higher-capacity DFIG-capable units.

Double Fed Wind Turbine Market

Why This Report Matters for 2026 Decisions

- Timing: 2026 is a pivot year — policy tightness on grid codes, intensified repowering initiatives in established markets, and raw-material volatility together change investment-return profiles for drivetrain choices.

- Risk-to-Reward Precision: Operators must quantify the trade-offs between upfront capital, ongoing service costs, and grid compliance investments; this report translates aggregate market dynamics into deployable decision tools for 2026 procurement cycles.

- Competitive Positioning: The DFIG landscape remains technically mature but strategically fragmented. The report identifies where scale, service footprint and technology stacks will determine winners and losers across onshore repowering and greenfield builds.

Core Findings (High-Level)

- DFIG technology remains a durable commercial option for onshore and transitional offshore contexts, supported by a mature manufacturing and service ecosystem.

- Repowering programs in established markets are a significant near-term demand driver, changing the nature of procurement (faster cycles, service-heavy contracts).

- Supply-side pressures — notably rare-earth price dynamics and component lead times — are reshaping techno-economic comparisons between DFIG and alternative generator concepts.

- Grid-code tightening and evolving system needs are making enhanced power-electronics and control features (including grid-forming capabilities) a differentiator rather than a discretionary upgrade.

What the Report Contains — Practical, Actionable Modules

PW Consulting’s full report is structured to be a playbook, not an academic exercise. Key operational modules include:

Double Fed Wind Turbine Market

- Market sizing and revenue forecasts (base year 2025, revenue unit: Million USD) with scenario banding for conservative, base and accelerated demand paths through 2032.

- Investment decision templates and Total Cost of Ownership (TCO) calculators that let you stress-test CAPEX/OPEX assumptions and grid-compliance costs at the project level.

- Repowering playbook: site screening checklists, retrofit vs replace decision trees, and shortlists of OEMs and suppliers suited to different repowering archetypes.

- Supply-chain resilience maps and a procurement risk matrix focused on critical inputs and production bottlenecks.

- Supplier benchmarking framework built from public filings, product portfolios, service footprints and aftermarket contracts — designed for RFP shortlists and M&A diligence.

- Regulatory and grid integration intelligence, including implications of tighter ride-through and voltage-control obligations and early demonstrations of grid-forming DFIG capability.

- Strategic playbook for investors and utilities covering JV structures, industrial partnerships and service-led revenue models.

To protect the commercial value of the dataset and to drive direct engagement, the report preview intentionally omits granular sub-segment tables and high-resolution regional/application splits — those detailed tables are available in the full report and accompanying datasets.

Competitive Landscape — How the Major Players Stack Up

The DFIG market is populated by legacy OEMs with deep installed bases and a new generation of challengers; competitive advantage is being driven less by raw turbine specification and more by service capability, repowering experience and supply-chain integration. Notable providers profiled in the report include:

- Goldwind Science & Technology — A heavyweight with scale advantages and a broad DFIG offering in geared, high-speed configurations, supported by significant domestic demand and integrated manufacturing.

- Vestas Wind Systems — Global reach and established onshore platforms; competitive in the sub-4 MW band with strong lifecycle service capability.

- Siemens Gamesa Renewable Energy — Broad product portfolio and legacy geared DFIG platforms that remain relevant in repowering programmes across Europe.

- GE Vernova (GE Renewable Energy) — Strong global service network and engineered solutions for operators pursuing higher factory-to-grid integration.

- Envision Energy & MingYang Smart Energy — Chinese OEMs with aggressive scale and cost-integration plays; increasingly active in export markets and repowering bids.

- Nordex SE, Suzlon Energy, Shanghai Electric, Dongfang Electric, CSSC Haizhuang — Each brings regional strengths, competitive priced solutions and specialist service propositions that matter in local procurements.

Market concentration metrics indicate a moderately consolidated landscape: the top three vendors control a substantial share of market value while the top five capture a clear majority of commercial supply — a structure that supports both competitive tendering and strategic partnerships for aftermarket services.

Dynamics and Short-Term Risks

- Raw-material volatility: Rare-earth and magnet material price shocks materially change PMSG economics; DFIG retains an attractiveness where rare-earth exposure is a procurement risk.

- Regulatory tightening: Modern grid codes demand more from generator control systems; operators must budget for control-system upgrades and validation testing.

- Technology shifts: Demonstrations of grid-forming DFIGs change the optionality of DFIG in systems requiring enhanced stability contributions from turbines.

- Repowering wave: In several mature markets, operators prioritise units that deliver higher energy yield per site — this alters warranty, service and retrofit requirements.

- Aftermarket importance: Service revenues and availability guarantees are increasingly decisive in supplier selection and valuation.

Recommendations — A 2026 Playbook

- Prioritise repowering screening now: Identify near-term repowering candidates with the highest yield uplift and lowest grid-integration cost.

- Lock long-term supply contracts for critical components or diversify suppliers to mitigate rare-earth exposure.

- Include grid-compliance stress-tests in every project investment model — assume tighter ride-through and ancillary service obligations by default.

- Negotiate service-led contracts: Shift risk to OEMs where possible and secure performance-based O&M terms for new and repowered assets.

- Invest in technology pilots: Validate grid-forming DFIG capabilities on a pilot asset to reduce technical risk and create a template for scalable deployment.

- Consider portfolio-level mixes: Maintain optionality between DFIG and alternative drivetrains depending on site-level constraints and material-price scenarios.

- Prepare M&A and industrial partnership playbooks: service platforms and aftermarkets are where near-term consolidation will drive premium valuations.

Concluding Note — Strategic Value of the Full Report

PW Consulting’s Double Fed Wind Turbine Market report is intentionally practical: it translates macro forecasts into checklists, models and vendor analytics that can be executed in procurement cycles and board deliberations in 2026. The preview you are reading is a curated summary of the market direction, competitive dynamics and risk levers. For commercial teams and C-suite decision makers who need the granular inputs (detailed regional and application splits, vendor-level scoring matrices and downloadable TCO models), the full dataset and appendices are available through the PW Consulting portal. Engage with the full report to convert strategic intent into executable plans for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Double Fed Wind Turbine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com