Luxury SUV Market 2026: Strategic Imperatives from PW Consulting’s Forward-Looking Analysis

As global luxury automotive executives plan product roadmaps, capex cycles, and go-to-market strategies for 2026, they face a tight window to translate strategic intent into competitive advantage. PW Consulting’s latest Luxury SUV Market report — anchored on a 2025 base year and projecting through 2032 — distills the near-term inflection points and delivers an operationally focused playbook for decision-makers navigating electrification, regulation, and shifting consumer preferences.

Luxury Suv Market

Executive summary — headline trajectory

The luxury SUV segment has demonstrated resilient expansion through the early 2020s. Our topline modeling shows the market growing from roughly USD 125.1 Billion in 2020 to about USD 192.4 Billion in 2025, with the forecast pathway projecting continued expansion to approximately USD 329.8 Billion by 2032. The forecast period (2026–2032) carries a compound annual growth rate of 8.0%, underscoring sustained demand even as the competitive and regulatory environment accelerates transformation.

Luxury Suv Market

Two contextual takeaways matter for 2026 planning: first, growth is broad-based but not uniform — product, propulsion, and region mixes create vastly different margin and volume outcomes; second, market concentration is meaningful but not overwhelming (CR3 ~38.5%, CR5 ~56.2%), leaving space for both incumbent scale plays and well-executed challengers to win.

Luxury Suv Market

Why 2026 is a decisive year

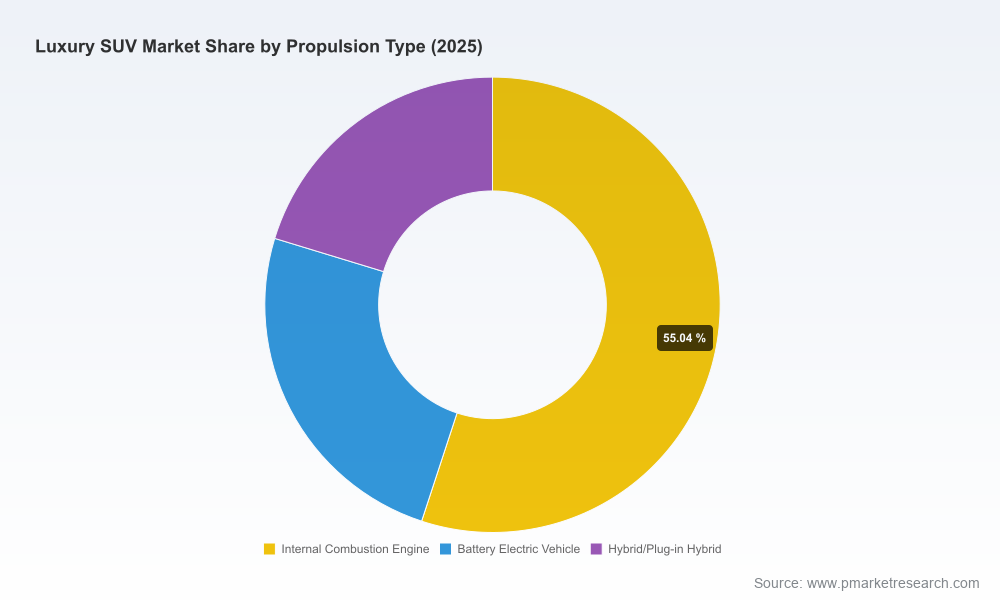

- Electrification inflection: Battery cost curves and regulatory pressure make 2026 the first year many luxury OEMs must materially shift portfolio allocations toward electrified SUVs to meet tightening CO2 and emissions standards across major markets.

- Supply-chain rebalancing: Raw material volatility and geopolitical concentration in critical mineral processing necessitate securing sourcing and recycling strategies now to shield 2027–2028 launches and planned capacity expansions.

- Consumer expectations crystallize: Luxury buyers are increasingly evaluating technology, sustainability credentials, and bespoke experiences as parity features (connectivity, ADAS, premium interiors) become table stakes.

Market dynamics shaping board-level choices

Several structural dynamics in our report directly inform which levers will drive durable advantage in 2026:

- Regulatory timelines accelerate product risk: New battery content and recycling requirements in key jurisdictions create compliance and cost implications for EV programs. Manufacturers that align design-for-recycling and supplier contracts ahead of enforcement will avoid retrofits that erode margins.

- Battery cost deflation is uneven but real: Downward pressure on pack prices opens profitable volume pathways for BEV luxury SUVs, but only for architectures optimized for weight, packaging, and premium features without cost inflation in adjacent subsystems.

- Concentration and incumbency advantages persist: The largest OEMs exhibit scale benefits in platform amortization and distribution; yet boutique and newer brands continue to exploit design differentiation, bespoke services, and targeted electrified offerings to capture niche high-margin segments.

- Supply risks demand strategic hedging: With critical mineral processing concentrated in a small set of geographies, multi-pronged mitigation — long-term offtake, localized recycling, and alternative chemistries — becomes an essential component of program risk models.

Competitive landscape — practical implications for 2026

Our competitive analysis synthesizes product portfolios, technology roadmaps, and strategic positioning across the luxury OEM spectrum. Key patterns to note:

- German premium incumbents (BMW Group, Mercedes‑Benz, Audi): Maintain leadership through broad model portfolios that balance ICE, hybrid, and BEV architectures. Their strength is platform flexibility, dealer reach, and engineering depth — enabling rapid iterations of luxury SUVs across powertrains.

- Performance luxury specialists (Porsche, Lamborghini, Aston Martin): Compete on high-performance differentiation and brand cachet, with electrified variants positioned to protect performance credentials while meeting regulatory thresholds.

- Heritage British ultra‑luxury players (Rolls‑Royce, Bentley): Lean into exclusivity and customization. Volume is limited, but margin per vehicle remains a strategic buffer against electrification capex when managed with bespoke, low-volume EV architectures.

- Asian challengers (Lexus, Genesis, Volvo): Emphasize reliability, value, and technology integration. Their hybrid-first or BEV strategies are optimized for premium buyer expectations in key markets and offer aggressive value propositions for 2026.

- North American luxury marques (Cadillac, Lincoln): Focus on domestic full‑size preferences and are rapidly electrifying marquee models. New launches and prototypes scheduled for market entry around 2026 signal intensified competition in the high-volume full-size luxury SUV subsegment.

Recent corporate moves highlight why 2026 will be active: new BEV luxury SUV launches and next‑gen platform introductions by both legacy OEMs and new entrants are converging on similar buyer segments. These developments increase product overlap and compress the timeframe to assess cannibalization, distribution readiness, and aftersales capabilities.

Strategic imperatives for 2026 decision-makers

For leadership teams considering 2026 budget cycles, PW Consulting identifies five priority initiatives to convert market growth into sustainable profit:

- Portfolio architecture consolidation: Rationalize platforms to maximize commonality across ICE, hybrid, and BEV variants while preserving brand-specific characteristics. This reduces capex leakage and accelerates time-to-market for electrified derivatives.

- Supply resilience as competitive moat: Transition from spot procurement to hybrid sourcing models (strategic long‑term contracts, equity in critical suppliers, and investment in localized recycling). Map critical-material exposures across programs and stress-test scenarios to 2030.

- Regulatory-forward product engineering: Embed recyclability, secondary-use battery strategies, and end-of-life logistics into early-stage design decisions to avoid late-stage cost overruns tied to emerging battery content mandates.

- Customer experience monetization: Differentiate through subscription services, bespoke customization, and integrated sustainability narratives. Luxury buyers are willing to pay for demonstrable provenance and personalized experiences — monetize those touchpoints without diluting brand exclusivity.

- M&A and partnership playbooks: Pursue targeted acquisitions for capabilities that are capital‑intensive to build (battery IP, software platforms, advanced materials) and structure partnerships that preserve margin and strategic optionality for 2027 launches.

What PW Consulting’s report delivers — operational tools and analytics

Our full report acts as a structured decision-support system for 2026 planning, not just a market narrative. Highlights include:

- Multi-scenario demand forecasts segmented by product family, propulsion architecture, and buyer cohort — with sensitivity ranges calibrated to raw-material and regulatory shocks.

- Competitive playbooks that map incumbent strengths and challenger attack vectors, including probable product overlaps and timing risks informed by announced launches and public roadmaps.

- Supplier-risk heatmaps and mitigation templates that integrate upstream concentration metrics, logistics exposure, and secondary-market recycling pathways.

- Product-to-profit P&L models that quantify margin trade-offs for electrification choices (architecture level), option content, and aftersales strategies.

- Regulatory readiness checklists aligned to imminent standards — including batteries content rules and regional CO2 trajectories — with recommended compliance timelines and cost-control levers.

To preserve competitive confidentiality for our clients and the strategic integrity of this public briefing, the report intentionally withholds granular region- and application-level splits, company unit sales, and other proprietary cell-level data — these are available in full to subscribers and clients who require transaction-ready analysis.

How to use the report in boardroom and planning cycles

- Board briefings: Use the market trajectory and concentration analysis to reset ambition and risk tolerance for electrified SUV programs across a five- to eight-year horizon.

- Product planning: Apply the portfolio optimization matrices to prioritize platforms and determine the fiscal year 2026 development budget re-allocation necessary to meet 2027–2028 launch windows.

- Procurement and supply-chain: Implement the supplier-risk framework immediately to inform contract renewals and capex commitments tied to battery supply and recycling capabilities.

- M&A diligence: Leverage our valuation and capability-mapping appendices to identify prime targets and structure earnouts that align with long-tail technology adoption risks.

Concluding perspective — positioning for profitable growth

The luxury SUV market offers compelling growth, but 2026 is the pivot year where strategic clarity translates to durable advantage. Organizations that synchronize product engineering, supply-chain commitments, and customer experience innovations now will capture outsized value as the market expands toward our 2032 baseline.

PW Consulting’s Luxury SUV Market report is designed as a decision accelerator — offering the macro context, competitor intelligence, and executable playbooks executives need this planning cycle. For access to the full dataset, detailed segment breakdowns, and tailored consulting engagements, please visit our report landing page or contact your PW Consulting advisor.

For detailed analysis of this topic, please visit the official page:Luxury Suv Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com