Can Oxygen Therapy Improve Skin Health and Glow?

Health |

2026-05-12 12:06:15

PW Consulting’s newest industry brief positions senior executives and market teams to make high-confidence decisions in 2026 and beyond. Anchored to a detailed base year analysis (2025) and a historical review spanning 2020–2025, our study projects the absorbable cranial clamp market to grow at a 5.8% CAGR over the 2026–2032 forecast period. The market, estimated at USD 385.0 Million (revenue unit: Million) in 2025, is expected to continue its steady climb into the second half of the decade. This preview summarizes why 2026 will be a pivotal year for players across medtech, hospital procurement, and private equity, and explains the practical, decision-grade content contained in the full report.

Absorbable Cranial Clamp Market

Measured, resilient growth: The market has expanded through 2020–2025 and enters 2026 from a position of validated demand and incremental innovation. Our forecast horizon (2026–2032) assumes technology adoption continues at a modestly accelerating clip, consistent with the observed 5.8% CAGR.

Absorbable Cranial Clamp Market

Clinical evidence is reshaping purchasing behavior: Recent multicenter trial data and device clearances have shifted the comparative conversation from mere fixation to long-term bone healing and resorption profiles. These clinical differentiators are now primary inputs to procurement decisions at major neurosurgical centers.

Absorbable Cranial Clamp Market

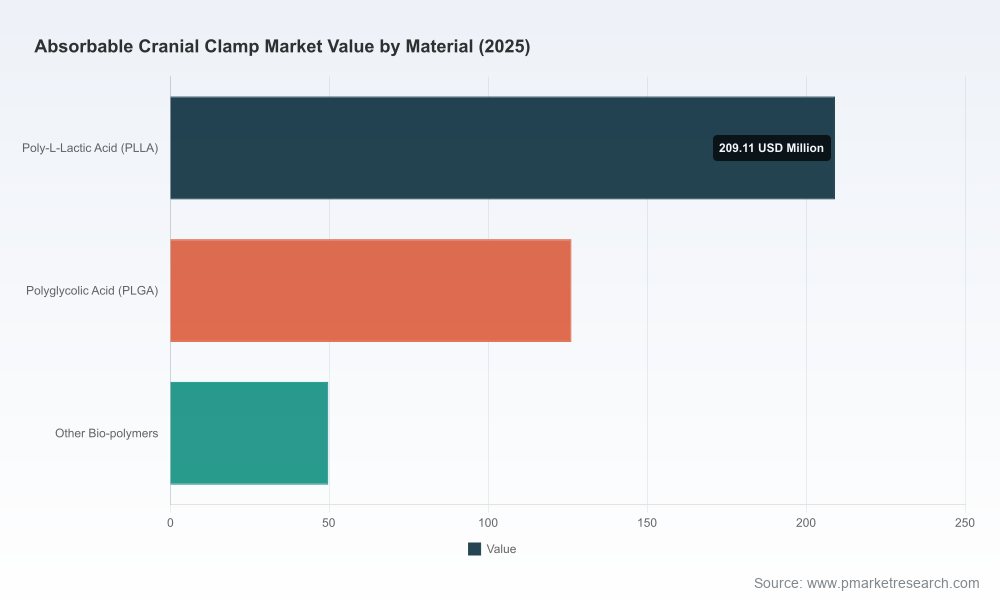

Material science matters operationally: Distinct polymer chemistries deliver different early mechanical retention and long-term resorption kinetics; these trade-offs drive surgeon preference, inventory management, and the case-mix economics of cranial surgery suites.

Consolidation and concentration create M&A windows: The market displays meaningful concentration at the top tiers, signaling both barriers for smaller entrants and attractive roll-up opportunities for investors seeking scale in manufacturing, regulatory expertise, and commercial coverage.

Executives must treat 2026 as a year for deliberate choices across five strategic vectors. Each vector is actionable and tied to measurable outcomes explored in the full report.

Evidence-first commercialization: Product teams should prioritize randomized or multicenter non-inferiority trials with endpoints aligned to bone healing and reoperation rates, not only short-term fixation. The commercial ROI of a trial that convincingly demonstrates superior osseous integration can be an order of magnitude greater than marketing spend alone.

Material and product portfolio strategy: Design roadmaps should clarify where to deploy slower-resorbing PLLA-type constructs versus faster-resorbing PLGA-type materials based on target clinical scenarios (e.g., elective craniotomy vs trauma). Manufacturing and inventory implications should be modeled alongside clinical value.

Market access and procurement playbooks: Health systems are increasingly asking for lifecycle cost and clinical-effectiveness evidence. Organizations that prepare ready-made HTA dossiers, hospital economic models, and surgeon training modules will reduce friction at the point of purchase.

Go-to-market and partnership models: Direct commercial presence remains valuable in core neurosurgical markets; distributorship or OEM partnerships are often optimal for adjacent or emerging markets. The proper mix depends on an organization’s cost-to-serve and regulatory footholds.

M&A and inorganic growth: Given the documented concentration among market leaders, buyers should target targets that offer surgical workflow integration, regulatory clearances in complementary geographies, or proprietary biomaterials that fill portfolio gaps.

Our competitive review in the full report synthesizes product archetypes, regulatory timelines, clinical evidence, and commercial performance for the market’s most consequential companies. Without divulging confidential subsegment figures in this preview, we highlight three archetypal strategic positions.

B. Braun Melsungen AG (Aesculap) — incumbent platform strength: Aesculap’s CranioFix absorbable system exemplifies instrument-free design and a longevity profile engineered for gradual resorption. Its established clinical adoption and product ergonomics create high switching costs for hospitals; incumbency advantages are rooted in OR familiarity and integrated surgical instruments.

Johnson & Johnson (DePuy Synthes) — scale and process integration: DePuy’s RAPIDSORB system typifies the large-cap approach: validated manufacturing processes, global distribution channels, and documented early fixation stability aligned to surgeon expectations. Such scale supports rapid supply continuity and comprehensive training programs.

MedArt Technology Co., Ltd. — evidence-driven challenger: MedArt has combined high-purity polymer formulation with multicenter trial evidence demonstrating competitive mechanical performance and accelerated bone healing. Regulatory milestones (including a recent 510(k) clearance) give MedArt a tactical foothold to expand beyond its initial geographies.

Each profile in the report includes a concise strategic playbook: strengths/opportunities, vulnerability analysis, and 12–36 month tactical moves their rivals must expect and counter.

Polymer performance and surgeon expectations: Different polymers retain strength on different timelines. For example, some product families are engineered to maintain a large portion of initial strength through the first three months before progressing through a controlled resorption window measured in years. Other chemistries are designed for faster mass loss but an earlier return to native bone mechanics. These differences have consequences for post-op protocols, infection risk management, and revision strategies.

Regulatory clarity reduces go-to-market uncertainty: Recent 510(k) clearances for absorbable cranial fixation products have lowered technical entry barriers into several regulated markets, but full commercial traction still depends on surgeon-level evidence and hospital purchasing workflows.

The study is purpose-built for market-facing leaders who need executable outputs for board-level decisions in 2026. Highlights include:

Consolidated market sizing and forecast model (2020–2032) with scenario toggles — base, upside (adoption acceleration), and downside (procurement compression).

Segment-level adoption curves and surgeon preference maps (presented in the full dataset; summary insights included here only in narrative form).

Company battlecards: go-to-market scorecards, regulatory timelines, recent clinical evidence, and a competitor response matrix.

Commercial playbooks for hospital systems and medtech suppliers — pricing sensitivity, inventory optimization, and surgical training rollout plans.

M&A screening tool and valuation comparators tailored to medtech private equity investors.

Operational levers for manufacturing scale-up and cost engineering for polymer-based implants.

To preserve competitive advantage for subscribers, the report omits certain granular subsegment tables in this press release; purchasers of the full report receive the complete dataset and a live model file to run bespoke scenarios.

New product launch: A midsize medtech firm prioritizes a multicenter non-inferiority trial focused on bone-healing endpoints and pairs that evidence with a targeted reimbursement dossier — shortening hospital adoption timelines by a quantifiable margin compared with traditional launch models.

Buy-side strategy: A health system aggregates neurosurgical purchasing across regional hospitals and negotiates bundled pricing tied to documented reductions in reoperations and faster rehabilitation — shifting supplier conversations from per-device price to per-patient episode economics.

Private equity play: An investor builds a roll-up thesis combining a polymer platform manufacturer with a clinical evidence specialist and an established distribution network to extract multiple operational synergies within 24 months post-close.

Key risks for 2026 include material supply volatility, regulatory reversals in key geographies, and surgeon preference inertia. The report contains a prioritized risk register with early-warning indicators and recommended mitigation actions — a one-page executive dashboard for boardrooms and deal teams.

For organizations planning capital allocation, product development, or go-to-market repositioning in 2026, the choices made this year will determine market share and margin trajectories through 2032. The market’s steady growth—anchored by a 5.8% CAGR across the forecast period and a 2025 base of USD 385.0 Million—rewards evidence-based entry, strategic partnerships, and operational discipline. Incumbents should defend with clinical and logistical depth; challengers should prioritize differentiated clinical outcomes and smart regulatory sequencing.

PW Consulting’s full Absorbable Cranial Clamp Market report (base year 2025; historical years 2020–2025; forecast period 2026–2032; currency USD; revenue unit: Million) provides the granular, model-ready intelligence that corporate development, commercial, and clinical affairs teams need to execute in 2026. For access to the complete dataset, company models, and our proprietary scenario toolset, please visit the PW Consulting report page or contact our industry practice.

For detailed analysis of this topic, please visit the official page:Absorbable Cranial Clamp Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com