Audiobooks: Redefining Reading Habits Worldwide

Technology |

2026-04-06 07:40:57

As organizations finalize budgets and strategic plans for 2026, the oil fired water heater market presents a classic example of a mature, niche equipment market that demands focused, evidence-based decision making. PW Consulting’s latest market brief — built on a base year of 2025 with historical coverage from 2020–2025 and a seven-year forecast to 2032 — delivers the actionable intelligence executives need to convert modest growth into durable competitive advantage.

Oil Fired Water Heater Market

The headline is straightforward: the global oil fired water heater market is stable and slowly expanding. Our base-year estimate for 2025 places the market at approximately USD 420.0 Million, with a mid-single-digit trajectory across the forecast window that equates to a compound annual growth rate (CAGR) of 2.12% for 2026–2032. That profile — limited overall growth but resilient revenue streams — makes the segment strategically interesting for incumbents with established channel access, aftermarket advantages, or consolidation ambitions, and for new entrants seeking differentiated value propositions.

Oil Fired Water Heater Market

But beneath a benign headline CAGR lies a landscape shaped by four forces that will determine winners and losers in 2026 and beyond: regulatory pressure on efficiency, fuel-price volatility and alternative fuels, channel and aftermarket economics, and consolidation among specialist OEMs.

Oil Fired Water Heater Market

Regulatory tightening is real and targeted. North American and select international regulators are sharpening rules that govern energy factors and input rates for oil-fired storage water heaters. For example, recent U.S. federal criteria and Canadian input-rate regulations impose minimum energy performance metrics for smaller household units. There is also an absence of ENERGY STAR criteria for oil-fired storage heaters in the U.S., creating an uneven policy landscape that both constrains and creates opportunity: manufacturers can innovate to exceed regulatory baselines and use efficiency leadership as a commercial differentiator.

Fuel economics and alternatives shape total cost of ownership. Heating oil price volatility continues to matter materially for end users. Historical winter pricing projections have shown meaningful year-on-year swings; while the market has seen periods of price relief, longer-term volatility increases the value of higher-efficiency products and fuels compatibility (e.g., blends, biofuels). For owners and specifiers, modest capex increases for higher-efficiency models can deliver measurable lifecycle savings in some scenarios — an insight we model extensively in the report.

Market scale supports specialization and aftermarket models. Despite being a small share of broader water-heating shipments, oil-fired heaters command stable replacement cycles and aftermarket service economics. That makes service contracts, distribution exclusives, and retrofit solutions important levers for margin expansion — especially in legacy installations where conversion to gas or electric is impractical or cost-prohibitive.

Consolidation and OEM strategies are accelerating. The competitive landscape is concentrated: the top three and top five players control a meaningful share of the market, creating advantages for scale in manufacturing, burner sourcing, and channel relationships. Recent M&A and product showcase activity illustrates clear instrumentality: incumbents are reinforcing portfolios while signaling their strategic intentions to end users and dealers.

The report’s competitive chapter combines company-level profiling with capability mapping to show where firms are investing and where gaps remain. Notable movements include an acquisition that reshapes North American leadership and visible trade-floor activity that signals the lines of strategic investment.

Platform consolidators are bulking up product portfolios. A leading example is the 2025 acquisition that brought a historically dominant oil-fired heater brand under the umbrella of a larger manufacturer. This transaction strengthens channel reach and creates cross-sell opportunities into commercial and specialty segments. Subsequent trade-show participation in 2026 underscored the acquirer’s intent to leverage existing burner partnerships and to promote proven product platforms to broader customer segments.

Legacy specialists are defending niche leadership. Longstanding manufacturers with commercial-grade offerings remain important suppliers for high-BTU and large-capacity applications. Their installed base and specification relationships continue to be competitive moats, especially in regions and asset classes where conversion cycles are long.

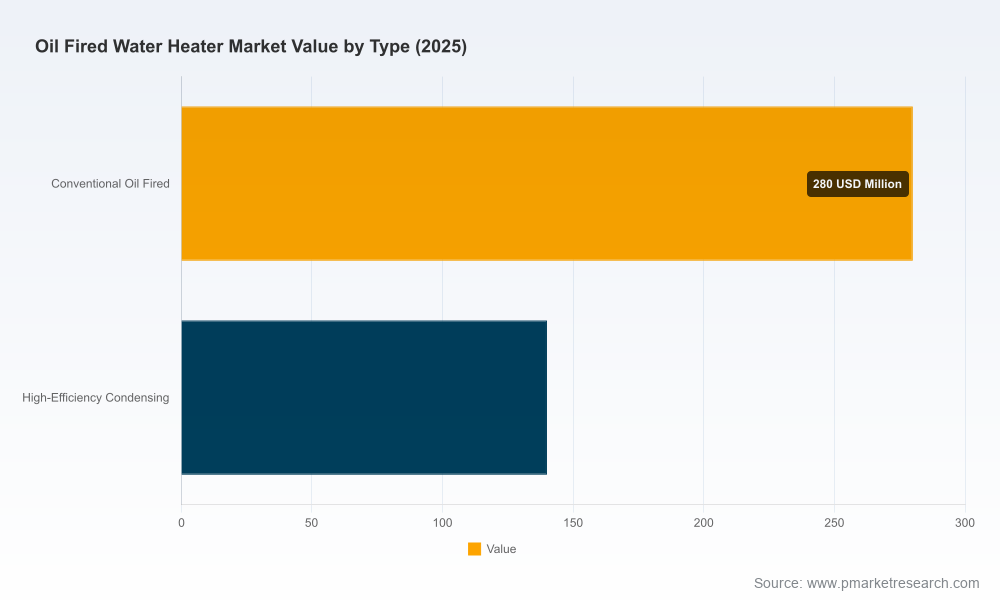

Technology differentials are modest but decisive. The split between conventional oil-fired designs and higher-efficiency condensing units defines most product-level competition. While the condensing segment is technically superior on fuel use and lifecycle cost in many scenarios, it carries different installation constraints and capital requirements. Successful vendors are those that pair product innovation with retrofit-friendly installation solutions and financing or service bundles.

To guide 2026 strategy-setting, PW Consulting’s brief combines market sizing with pragmatic toolkits. Key deliverables include:

For executives preparing plans for the coming fiscal year, our analysis crystallizes into five recommended imperatives:

Companies that will outperform the 2.12% CAGR are those that combine three elements: operational excellence in aftermarket delivery, product differentiation that meaningfully reduces total cost of ownership, and the strategic appetite to capture adjacent opportunity through targeted M&A or partnerships. Firms that ignore channel economics or defer compliance-driven product changes risk margin compression as specifiers increasingly prioritize efficiency and lifecycle transparency.

Our market sizing is expressed in USD (Million) and is anchored on a robust bottom-up approach that reconciles manufacturer shipment data, trade registrations, and end-user expenditure models across a five-year historical window (2020–2025) and a 2026–2032 forecast horizon. Market concentration is noteworthy: the top three and top five suppliers together represent a meaningful share of market revenues, a fact that shapes competitive dynamics and the relative ease of value-pool capture for larger players.

This note is a strategic “trailer” intended to surface the most consequential trends and recommendations to inform 2026 decision-making. The full PW Consulting Oil Fired Water Heater Market report contains the granular segment modeling, regional and application breakdowns, eight detailed supplier profiles, and downloadable scenario models that senior leaders use to build budgets and investment cases.

For clients and decision-makers preparing their 2026 strategic reviews, the full report supplies the data and tools you will need to: quantify upside from aftermarket monetization, model ROI on product platform upgrades tied to efficiency standards, and prioritize acquisition targets or partnership opportunities by expected value creation.

Contact PW Consulting for access to the complete report and our customizable modeling templates. Our team stands ready to translate these insights into a bespoke strategy workshop and an executable 12–18 month roadmap for your organization.

For detailed analysis of this topic, please visit the official page:Oil Fired Water Heater Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com