P-Series Glycol Ether Market Size, Share, Trends, Forecast 2024–2034

Networking |

2026-05-18 09:51:15

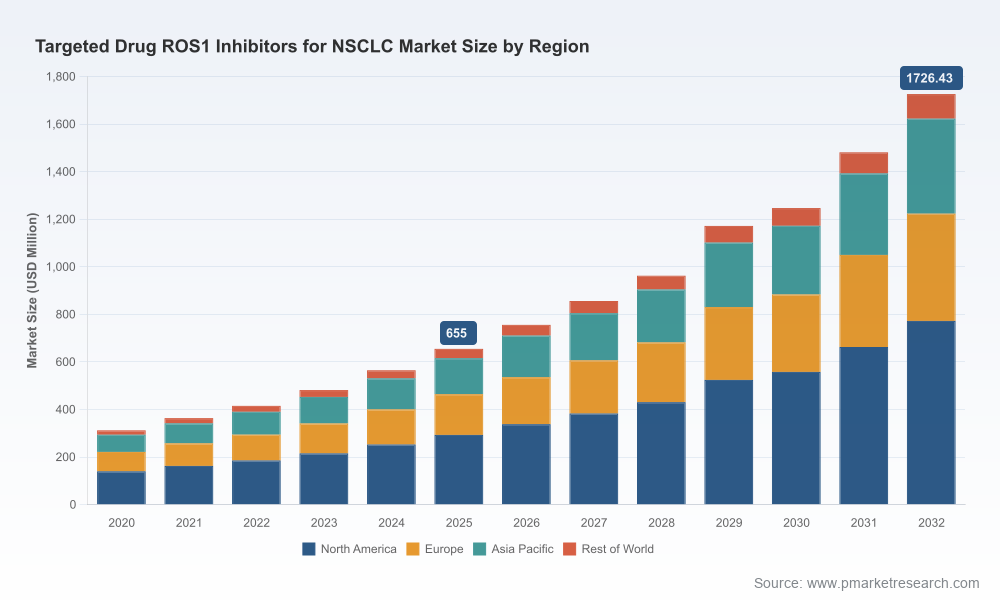

PW Consulting’s latest market intelligence uncovers a rapidly maturing, high-growth market for ROS1-targeted therapies in non-small cell lung cancer (NSCLC). Our new report — built on a robust historical series (2020–2025) and a detailed forecast (2026–2032) — shows the market accelerating from a strong 2025 base year into a multi-fold expansion by 2032 at a compound annual growth rate (CAGR) of 14.85%. For executives preparing strategic roadmaps in 2026, the implications are clear: this is not a maintenance exercise but a moment to reallocate resources, recalibrate commercial tactics, and pursue selective clinical and M&A plays that convert growth into durable value.

Targeted Drug Ros1 Inhibitors For Nsclc Market

The ROS1 inhibitor market is transitioning from a niche, clinically driven space into a commercially consequential oncology segment. The top-line trajectory is unmistakable: after consistent historical growth through 2025, our base forecast projects continued acceleration, with the market expanding materially through 2032. This trajectory is supported by three reinforcing dynamics: (1) regulatory momentum and label expansions, (2) the arrival of next‑generation inhibitors and life‑cycle events, and (3) growing diagnostic penetration that enlarges the identifiable patient pool.

Targeted Drug Ros1 Inhibitors For Nsclc Market

PW Consulting’s model quantifies the market from 2020 through a 2032 forecast horizon. After accelerated growth during 2020–2025, the market continues to expand meaningfully in our forecast window. For strategy teams, the takeaway is less about the absolute figures and more about the pace and predictability of that expansion: a near‑15% CAGR implies that a business model calibrated to 2025 revenues will likely be under-resourced by 2028 if it fails to anticipate demand, regulatory shifts, and competitive moves.

Targeted Drug Ros1 Inhibitors For Nsclc Market

Practically, a 14.85% CAGR implies that early investments in commercial scale, diagnostic partnerships, and post‑marketing evidence generation will deliver asymmetric returns versus later movers. It also means that supply‑side considerations—manufacturing scale, distribution agreements, and patient support programs—must be planned with multi‑year growth in mind rather than single‑year budgeting.

The ROS1 market is highly concentrated: the top three players control a dominant share of value, with the top five nearing full market coverage. This concentration creates both barriers and opportunities. Incumbents have scale advantages in commercialization, diagnostic co‑promotion, and payer relationships; challengers can still win through differentiated clinical profiles, targeted label expansions, or strategic alliances that unlock new patient cohorts.

Our competitive assessment reviews corporate positioning across clinical differentiation, regulatory trajectory, commercial reach, and RWE capacity. For each major player, the report includes a practical “competitive playbook” outlining tactical levers to defend or disrupt market share without disclosing proprietary segment-level revenue splits in this preview.

Several structural industry events frame strategic decision-making for 2026:

Our full report is designed as an executive decision toolkit. Key deliverables include:

Note: While the full report contains granular segmentation, regional splits, and channel-level forecasting, this release intentionally omits those proprietary tables to preserve the report’s role as a strategic subscription product.

Based on our analysis, PW Consulting recommends that corporate leadership and commercial teams prioritize the following in 2026:

Boards and C‑suite teams will find the report valuable for prioritizing capital allocation across R&D, commercialization, and M&A. We translate epidemiological and clinical trends into financial impact scenarios that show upside and downside outcomes tied to clear decision nodes (e.g., trial success, approval timing, patent expiries). Our scenario-driven approach equips boards to answer the central strategic question for 2026: where to place scarce capital to maximize long‑term enterprise value in a market growing at near‑double‑digit rates.

For teams preparing 2026 plans, immediate actions include:

Market growth, regulatory motion, and competitive concentration together create a high‑stakes environment for ROS1 inhibitors in NSCLC. With a forecast horizon extending through 2032 and a clear near‑term inflection in 2026, companies that move decisively on diagnostics, evidence generation, and targeted partnerships will capture disproportionate value. PW Consulting’s full report provides the granular inputs and scenario tools necessary to convert this market trajectory into strategic wins—without the guesswork. For teams building 2026 plans, this intelligence turns ambiguity into a sequence of actionable, prioritized steps.

To access the full dataset, regional and channel breakdowns, and the complete tactical playbooks referenced here, please refer to the official report page. This briefing is a strategic preview; the full report contains the proprietary segment tables and modelling detail that will inform executable 2026 plans.

For detailed analysis of this topic, please visit the official page:Targeted Drug Ros1 Inhibitors For Nsclc Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com