Attapulgite Market: Size, Share, and Future Growth

Other |

2026-04-23 02:07:19

PW Consulting’s new market research report on the Livestock Dermatology Drugs Market crystallizes the commercial and regulatory dynamics that will shape boardroom decisions in 2026 and beyond. Grounded in a rigorous historical review (2020–2025) and a forward-looking forecast (2026–2032), the study presents an evidence-based roadmap for investors, R&D leaders, manufacturing executives, and commercial strategists in animal health.

Livestock Dermatology Drugs Market

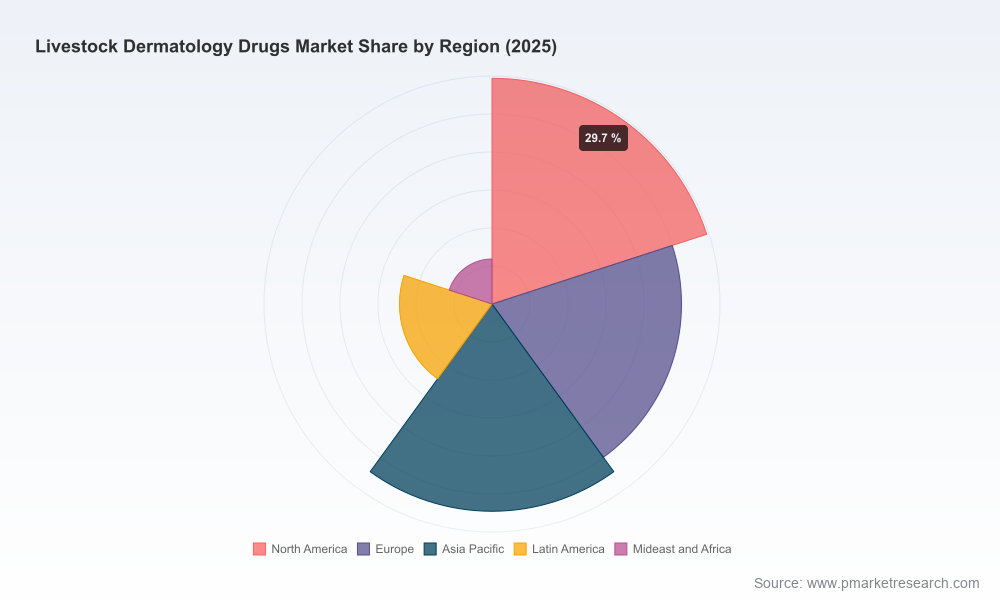

Management teams entering 2026 face a landscape defined by steady demand expansion, evolving regulatory constraints, and an intensifying race to secure manufacturing and distribution resiliency. The global market for livestock dermatology drugs expanded from roughly USD 1,180 million in 2020 to an estimated USD 1,543 million in 2025, and our base-case projection takes the market to about USD 2,244 million by 2032 — implying a compound annual growth rate of approximately 5.5% across the forecast window. These headline figures signal durable opportunity but mask important structural shifts that must be considered when prioritizing capital, R&D, and commercial initiatives.

Livestock Dermatology Drugs Market

Demand growth is broad-based and persistent. The mid-single-digit CAGR reflects the interplay of rising production-animal populations in several markets, improved access to veterinary care in emerging regions, and increased willingness to invest in preventive treatments and herd-level management.

Livestock Dermatology Drugs Market

Product mix is evolving. Therapeutic use remains critical for secondary infections and ectoparasite control, while prevention — including vaccination programs for certain viral dermatoses — increasingly shapes procurement and market dynamics.

Consolidation and scale matter. The market exhibits moderate concentration: the top three players account for roughly 42% of the market while the top five approach the high‑fifties percentile range. This concentration creates both barriers and partnership opportunities for mid‑tier firms.

Vaccination remains the primary control strategy for major viral skin diseases. Authoritative guidance emphasizes annual vaccination in endemic areas for conditions such as lumpy skin disease; there are no dedicated commercial antivirals for such viral dermatoses, which continues to focus investment on vaccines and on managing secondary bacterial complications.

Antiparasitic approvals and stewardship shape product choice. Macrocyclic lactones and other ectoparasiticides retain central importance for mange and lice control, but shifting regulatory frameworks and residue concerns require adaptive labeling, withdrawal strategy planning, and robust pharmacovigilance.

Low-cost topical adjuncts remain an essential part of field practice. Fungicidal preparations and iodine solutions continue to be widely used for ringworm and localized fungal or inflammatory issues, representing a persistent low‑margin but high‑volume segment for local manufacturers and distributors.

Supply chain and manufacturing capacity are strategic levers. Recent investments in sterile injectable capability and site upgrades underscore manufacturer focus on secure supply of critical anti-infectives used to manage dermatological complications.

The report’s corporate profiles synthesize strategy, portfolio breadth, manufacturing reach, and recent strategic moves for leading animal-health players. Collectively, established multinational vendors maintain advantages through scale, integrated R&D pipelines, and global commercial networks; meanwhile regional and specialized players compete on formulation agility, local regulatory expertise, and cost position.

Large integrated companies with broad veterinary portfolios continue to invest in both preventive (vaccines) and therapeutic (ectoparasiticides, antibiotics, antifungals) solutions. Their ability to bundle herd health solutions and integrate diagnostic services remains a key differentiator.

Specialist firms and regional champions concentrate on scalable, field‑proven formulations (topicals, injectables) and on nimble regulatory execution across jurisdictions with high livestock density.

Recent notable developments highlight tactical shifts: a conditional regulatory approval for a topical fluralaner solution addressing myiasis-type infestations demonstrates how fast‑moving approvals can unlock new indications and drive substitution; concurrent investments in sterile injectable capacity by manufacturing-focused players signal the strategic importance of supply security for anti-infective lines.

PW Consulting’s study is structured to support immediate business decisions in 2026. Key deliverables include:

Market sizing and trend analysis (historical 2020–2025; forecast 2026–2032) with scenario modeling and sensitivity analysis around pricing, adoption curves, and regulatory outcomes.

Therapeutic-class and product-type mapping that identifies where value pools are shifting and which formulation formats are likely to gain share under different regulatory and price-pressure scenarios.

Animal-type demand vectors and distribution-channel diagnostics that inform GTM (go‑to‑market) prioritization without disclosing the granular segment tables reserved for the full report.

Regulatory tracker and risk matrix capturing vaccine guidelines, residue standards, and ectoparasiticide approvals across representative regulatory regimes to aid launch planning and compliance budgeting.

Manufacturing and supply‑chain stress tests with mitigation playbooks for raw material availability, cold chain dependencies, and sterile injectable scale‑up timelines.

Competitive intelligence dossiers on leading and fast‑growing players, including investment rationales, likely partnership targets, and M&A heat maps.

Actionable recommendations and investment cases: capital allocation frameworks, R&D prioritization scorecards, pricing playbooks, and sample commercial pilots designed for rapid deployment in 2026.

Prioritize portfolio presence in parasiticides and preventive vaccines. Our scenario work shows that solutions addressing ectoparasites and herd-level preventive measures are durable revenue drivers and hedge regulatory pressure on therapeutic antibiotics.

Invest selectively in sterile-injectable capacity and contract-manufacturing relationships. Supply security is now a board‑level concern; capacity investments can be de‑risked through tolling and geographic diversification.

Develop low-cost, field-ready topical options for smallholder segments. These products support penetration in markets where veterinary infrastructure is thin and where budget constraints drive preference for inexpensive adjunct therapies.

Build regulatory intelligence and local registration playbooks. Faster approvals for novel indications (e.g., certain topical antiparasitics) create windows of opportunity for first‑mover advantage in specific jurisdictions.

Pursue partnerships across vaccine development and distribution networks. Given the centrality of vaccination for viral dermatological threats, alliances with vaccine specialists and public health bodies can accelerate adoption and build long-term channel advantage.

Embed antimicrobial stewardship into product and commercial strategy. Companies that proactively demonstrate reduced‑antibiotic protocols, validated by field data, will benefit from regulatory goodwill and payer preference.

Use granular scenario planning to set go/no‑go thresholds. The report’s scenario models allow management to define clear investment triggers tied to price erosion, approval timelines, and manufacturing ramp milestones.

Executives tell us they need three things from market intelligence in 2026: reliable topline trajectories, pragmatic operational playbooks, and clear triggers for capital allocation. This report delivers on all three. By combining robust historical data, probabilistic forecasts, regulatory mapping, and named-competitor intelligence, we convert ambiguity into a set of prioritized, executable options with measured downside protections.

This briefing highlights the strategic contours and tactical implications. The full PW Consulting report contains the complete dataset, breakouts by therapeutic class, animal type, and distribution channel, as well as downloadable model files and an interactive scenario dashboard to support board-level discussions and investment memoranda. To access the full segmentation tables, company scorecards, and the downloadable forecasting model, please visit our report landing page.

For bespoke support — including tailored scenario runs, M&A target screening, or a rapid 90‑day go‑to‑market playbook calibrated to your portfolio — PW Consulting’s Livestock Therapeutics practice is accepting limited advisory mandates for 2026. Contact our team to schedule a briefing.

PW Consulting — Translating veterinary market intelligence into actionable strategy for confident decision‑making in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Livestock Dermatology Drugs Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com