PW Consulting Report: Optical Brighteners Market to Expand at a 5.12% CAGR Through 2032

Other |

2026-07-06 14:28:58

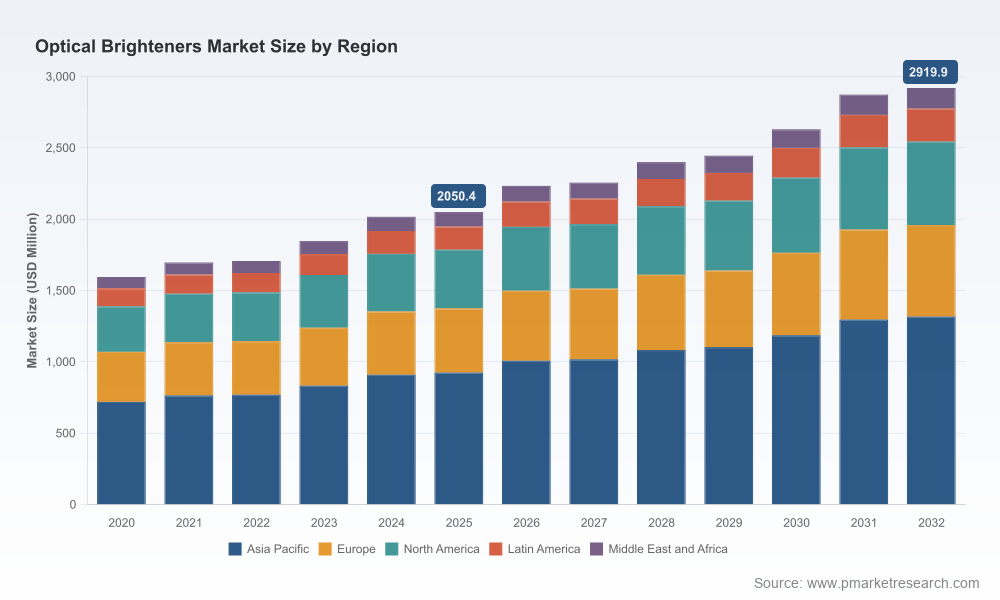

The optical brighteners market has moved from a niche industrial input to a strategically sensitive materials segment where regulatory pressure, raw-material volatility and customer sustainability demands intersect. Our latest market model — based on a 2025 base year and a 2026–2032 forecast horizon — shows the market expanding from approximately USD 2,050.4 Million in 2025 toward USD 2,919.9 Million by 2032, representing a compound annual growth rate (CAGR) of 5.12% across the forecast period. This trajectory masks important structural shifts: evolving chemistries, differentiated purity and formulation requirements, tariff-driven sourcing reconfigurations and an intensifying premiumization of compliant, low-impact grades.

Optical Brighteners Market

Timing of investment: With growth steady but not explosive, capital allocation in 2026 should prioritize margin-protecting moves (purification, formulation upgrades, compliance) over broad greenfield capacity unless tied to secured offtakes.

Optical Brighteners Market

M&A and portfolio plays: The market’s moderate concentration (top three suppliers ≈ 28.5%; top five ≈ 41.2%) creates windows for well-capitalized buyers to scale as strategic niches consolidate — especially in detergent and high-purity applications.

Optical Brighteners Market

Supply-chain resilience: Tariff and trade interventions, raw-material linkages to petrochemicals, and regional regulatory divergence make supplier rationalization and near‑sourcing urgent components of 2026 procurement strategies.

Commercial differentiation: Brands and formulators increasingly buy on compliance and lifecycle impact; companies that can prove ZDHC/eco-label alignment and offer low‑persistence chemistries command pricing premiums and strategic contracts.

Proprietary quantitative market model (historical 2020–2025; detailed forecast 2026–2032) with scenario toggles for macro variables (oil price shocks, tariff impositions, regulatory tightening).

Interactive pricing and margin sensitivity analysis tied to petrochemical feedstock indices and common contract structures.

Supplier capability matrix and commercial scorecard — technology leadership, regulatory-ready portfolios, capacity, geographic footprint and customer concentration.

Regulatory impact tracker covering EU REACH, ZDHC MRSL, U.S. trade rulings and likely near-term amendments—linked to product re-formulation levers and compliance costs.

Actionable M&A playbook: target screening criteria, valuation heuristics for technology vs. capacity bets, and integration checklists focused on process safety, analytical labs and customer contracts.

Go‑to‑market templates for producers and ingredient suppliers, including segmentation-based commercial tactics (industrial vs consumer-packaged goods customers), tiered pricing and sustainability claims governance.

Operational advisory: recommendations for CAPEX prioritization (e.g., purification/pakking lines), contract manufacturing vs. in‑house production trade-offs, and inventory/hedging policies under tariff risk.

Regulatory pressure is the single largest non-market demand driver. European REACH restrictions on specific stilbene derivatives and tightening ZDHC and eco‑label requirements are prompting formulators and producers to accelerate migration to lower‑impact chemistries and certifiable production processes. For companies operating without compliant grades, 2026 should be the year to finalize either reformulation or offloading strategies.

Trade and tariff environment materially reconfigures competitiveness. Recent reinstatements of antidumping duties and new tariff measures have altered import cost dynamics, making local or regionalized manufacturing more attractive for some customer segments while raising the bar for low‑cost exporters to sustain margins.

Raw‑material exposure remains a core commercial risk. Optical brightener production is dependent on petrochemical intermediates; therefore, crude oil swings and intermediate‑chemical availability have direct, sometimes lagged, effects on input cost curves and working capital requirements.

Segmentation of demand is evolving. End users are differentiating between commodity whitening needs and high‑specification, durability‑oriented brighteners (bleach/heat resistance, low yellowing, regulatory-ready). Producers that can certify performance across these vectors capture better contract terms and lower churn.

The competitive map is composed of global specialty players, integrated chemical majors, regionally dominant low‑cost producers and a growing cohort of niche innovators. Strategic patterns to observe in 2026 include asset sales and targeted acquisitions, capacity debottlenecking focused on purification, and portfolio pivots toward sustainability‑compliant grades.

Archroma — Reinach, Switzerland: Leveraging brand‑level sustainability and cross‑application capability (textiles, paper, detergents). Its ULTRAPHOR® and Leucophor® platforms, showcased at industry venues in late 2025, are positioned to capture premium, compliant demand streams.

Catexel — Wiesbaden, Germany (ICIG): A critical strategic development is the closing of the acquisition of BASF’s optical brightening assets including the Monthey production site in early 2026. This transaction immediately expands Catexel’s detergent‑focused portfolio and manufacturing competency, and is exemplary of the kind of bolt‑on consolidation likely to continue.

Huntsman, Clariant, Eastman, 3V Sigma: These firms compete on integrated supply, high‑purity capability and service level. Huntsman’s commissioning of a new E‑GRADE purification unit in 2025 is a direct response to regulatory and quality demands in sensitive applications.

Indian and Chinese producers (e.g., Meghmani, Deepak, regional manufacturers): Cost competitiveness remains their advantage, particularly in less regulated segments. However, trade remedies and regulatory compliance requirements increasingly bifurcate the market between cost‑led and compliance‑led supply pools.

Specialists and additives houses (e.g., Milliken, Day‑Glo, Chemworld): Compete on niche formulations, polymer‑compatible grades and rapid customer support for product development, often serving as agile partners to downstream compounders and formulators.

Re-prioritize portfolio investment toward compliant chemistries and high‑value formulations. Delay broadscale volume expansions unless paired with secured long‑term offtake agreements.

Accelerate supplier diversification and near‑shoring for customers exposed to tariff or antidumping risk. Tactical stockpiling and hedging of key intermediates can buy negotiation room during policy shocks.

Modularize CAPEX: invest first in analytical and purification capacity that supports multiple chemistries and certifications rather than single‑product trains.

Use M&A to acquire regulatory‑ready technologies and customer relationships rather than purely to chase volume — targets with eco‑label credentials or niche thermal/bleach‑resistant grades typically provide higher ROI.

Embed compliance narratives in commercial talks. Buyers increasingly require traceability and third‑party verification; treating certification as a revenue enabler, not a cost center, unlocks premium pricing.

Design scenario‑based procurement contracts that include escalation clauses tied to intermediate indices, with shared‑savings mechanics for volumetric swings.

This market brief is a distillation of the analytical horsepower embedded in our full Optical Brighteners Market report. Subscribers gain access to the underlying models, downloadable data and a hands‑on implementation toolkit: supplier heat maps, M&A screening templates, regulatory compliance checklists, and a 12‑month operational playbook tailored to a company’s strategic posture (defensive, consolidator, or challenger).

Importantly, the full report provides the granular regional and application splits, company‑level operational metrics, and scenario outputs that CFOs, heads of procurement and business unit leaders need to finalize 2026 budgets and investment stances. Our “trailer” here shows the direction and the levers — the detailed tables, sensitivity runs and sourceable supplier contacts are available in the full deliverable.

For boards and executive teams: request the PW Consulting interactive model to stress‑test 2026 CAPEX and M&A plans under tariff and REACH tightening scenarios.

For commercial and procurement leads: schedule a supplier rationalization workshop leveraging our supplier scorecard and risk heat map to identify at‑risk contracts and negotiate resilience terms.

For R&D and product teams: use our chemistry‑roadmap section to prioritize reformulation projects that maximize compliance and minimize cost-to-implement.

To access the full report, detailed spreadsheets and company profiles that underpin this brief, please visit our publication page. The granular datasets and strategic playbooks contained therein are designed to convert the forecasts and dynamics summarized here into executable decisions in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Optical Brighteners Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com