Eastern Europe Core Materials Market Trends, Insights and Future Outlook

Other |

2026-04-27 03:46:12

As the senior strategy advisor and chief industry analyst at PW Consulting, I present a concise briefing on the strategic takeaways from our latest Flat Panel X‑Ray Detectors Market report. The sector is no longer a niche component market — it is a strategic frontier for medical-imaging OEMs, service providers, and industrial imaging specialists. The global market expanded from roughly USD 2.45 billion in 2020 to about USD 3.20 billion in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 5.6% through the 2026–2032 forecast window, reaching an estimated USD 4.69 billion by 2032. This trajectory creates both runway and urgency for decisive investments in technology, go‑to‑market, and regulatory preparedness.

Flat Panel X Ray Detectors Market

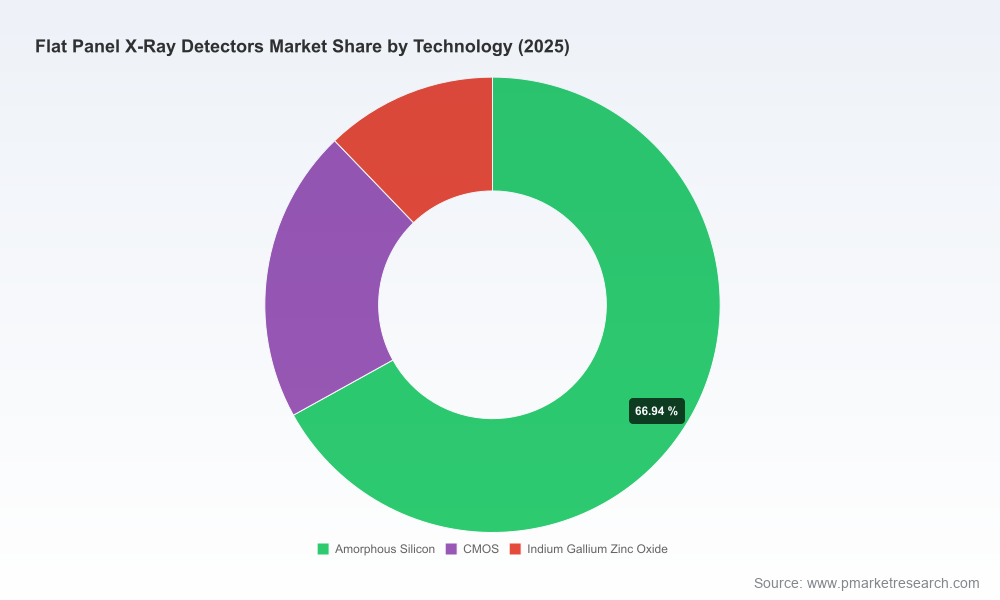

Technology transition is accelerating. The competitive battleground has shifted from purely panel size and basic sensitivity to material stacks and sensor architecture — amorphous silicon, IGZO, and advanced CMOS platforms are each driving differentiated clinical and operational value. Suppliers who translate sensor advantages into measurable workflow and diagnostic outcomes will capture disproportionate value.

Flat Panel X Ray Detectors Market

Regulatory gating is becoming a strategic constraint. Flat panel detectors used in mobile and stationary systems are regulated under established device classifications and 510(k) routes; recent 510(k) clearances across a range of vendors demonstrate that market access is attainable but requires a disciplined product/clinical evidence strategy. Expect regulatory timelines to materially influence product launch sequencing and channel rollouts in 2026.

Flat Panel X Ray Detectors Market

Pricing and margin pressure coexist with premiumization. Entry-level tethered panels remain a volume play, while glassless wireless and high‑definition panels command premium pricing. The market is maturing into a two‑track environment where differentiation (durability, image quality, wireless robustness, integration) enables higher ASPs, but commoditization at the low end compresses margins for unprotected suppliers.

Market structure and concentration create strategic windows. The market exhibits moderate concentration: the top three firms account for a meaningful share, and the top five approach a clear majority hold. This dynamic favors both targeted consolidation and strategic partnerships for firms seeking to scale quickly or enter adjacent product/system spaces.

We designed the report as a practitioner’s playbook for executives who must make capital, R&D, M&A, and market-entry decisions in 2026. Core deliverables include:

The report profiles the market’s diverse player set: global OEM incumbents, specialist detector manufacturers, imaging‑sensor companies, and cost‑competitive OEM suppliers. Leading independent detector manufacturers and established medical imaging conglomerates continue to anchor the market with broad installed bases and integrated product portfolios. At the same time, agile specialists focused on CMOS/IGZO innovation, and a cohort of Asian OEM suppliers, are increasing competitive intensity — particularly in mobile and price‑sensitive segments.

Notable firm archetypes we examine:

Recent regulatory approvals and product clearances we track validate the trajectory above — new 510(k) clearances in 2025 across multiple vendors underscore the market’s openness to new entrants but also reinforce the need for robust evidence packages and standard compliance.

PW Consulting’s analysis yields five prioritized actions for organizations planning to shape or defend market position in 2026:

The combination of steady market growth, moderate concentration, and technology-driven differentiation creates attractive deal opportunities — particularly for roll-up strategies that combine R&D capabilities with scale manufacturing and go‑to‑market reach. Use our M&A scorecards and cash‑flow models to stress-test assumptions under different adoption and pricing scenarios.

PW Consulting’s full Flat Panel X‑Ray Detectors Market report provides the granular segmentation, proprietary vendor scorecards, pricing matrices, and downloadable forecast models that executives and investment committees need to finalize 2026 plans. In this briefing I deliberately present the directional insights and strategic imperatives you must act on now; the full report contains the segment‑level detail, supplier rankings, and scenario tools that operationalize those decisions.

If your 2026 strategy depends on capturing share in imaging platforms, optimizing product roadmaps, or allocating capital into component manufacturing or M&A — the choices you make in the next 12 months will determine whether you lead or follow. PW Consulting’s report is designed to turn market foresight into executable decisions.

For detailed analysis of this topic, please visit the official page:Flat Panel X Ray Detectors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com