Neutron Counter Market Research Market: Trends, Drivers, and Challenges

Other |

2026-04-07 09:52:42

As enterprises, communications service providers (CSPs), and cloud platform owners plan capital and product roadmaps for 2026, the CNF (Cloud-Native Network Function) software market will be a central driver of network transformation, edge economics, and application delivery strategies. PW Consulting’s new market research brief synthesizes a detailed, actionable view of the CNF landscape: a market that expanded rapidly through 2020–2025 and, based on our analysis, is poised for sustained, high‑velocity growth across the 2026–2032 forecast window at a compound annual growth rate of 22.4%.

Cnf Software Market

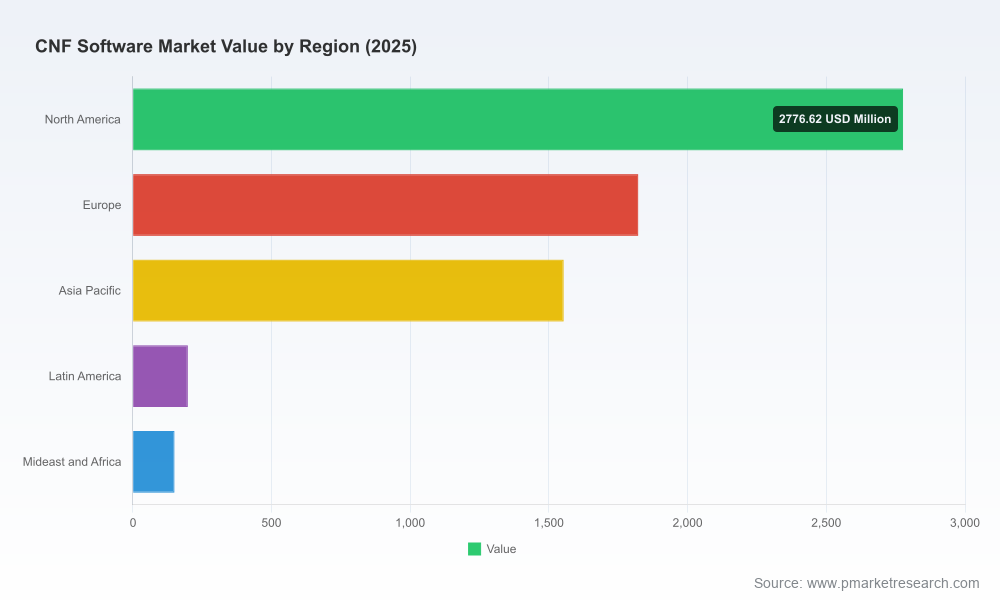

From an addressable market perspective, CNF software has moved from a nascent functional play to a mainstream architectural mandate for greenfield 5G and brownfield cloud modernization. Our base-year analysis (2025) captures both vendor product maturity and early large-scale operator deployments. Looking ahead, our forecast through 2032 assumes aggressive adoption across public, private, and hybrid clouds, with the resulting compound growth driving multi-fold increases in software spend, integration services, and cloud infrastructure consumption.

Cnf Software Market

Strategic implication: Organizations that delay vendor selection or architecture standardization into 2026 risk being locked into higher migration costs and suboptimal integration paths when CNF consumption accelerates.

Cnf Software Market

Strategic implication: Procurement cycles that incorporate software, orchestration, and certification timelines — rather than treating CNFs as isolated components — will realize better time-to-market and lower TCO.

Three converging dynamics make 2026 a make-or-break year for CNF strategies:

Standards and orchestration alignment: Kubernetes-centered orchestration patterns have become the de facto operational model for CNFs, shaped by ETSI NFV MANO adaptations and Container Infrastructure Service Management (CISM) practices. This reduces technical ambiguity but raises the bar for operations and verification.

Vendor certification and ecosystem validation: Major vendors are scaling certification programs and partner validation frameworks to secure interoperability and reduce integration risk — a trend that materially shortens deployment cycles for certified stacks.

Labor and skills pressure: The developer community supporting cloud native and telecom domains has expanded rapidly, increasing both the talent pool and the competition for specialized CNF orchestration and DPU-acceleration skillsets.

Our report is built to be operationally useful to CIOs, CTOs, procurement leads, and strategy teams. It avoids generic trend summaries and instead provides toolkit elements that teams can use in 90–180 day implementation windows:

Deployment playbooks — step-by-step guidance for validating CNF candidates in Kubernetes-based environments, including deployment patterns for public, private, and hybrid cloud footprints, and checklist-driven acceptance criteria for carrier-grade SLAs.

Integration and interoperability checklists — prescriptive tests to run against vendor CNFs (control plane, user plane, signaling, security), and a matrix of required platform capabilities (CNI, CSI, service mesh considerations, DPU support) to streamline proofs-of-concept.

Commercial evaluation templates — scoring models and RFP language tailored to CNF procurement that embed non-functional requirements like lifecycle management, observability, and upgrade automation, enabling apples-to-apples comparisons across vendors.

TCO and scenario models — forward-looking financial models that estimate operational costs and infrastructure consumption under different migration paths, and sensitivity analyses that quantify the impact of orchestration choices, workload placement, and acceleration hardware.

Vendor playbooks and vendor-risk mapping — assessment frameworks that combine technical compatibility, go-to-market readiness, and ecosystem commitments (e.g., certification programs) to prioritize vendor selections under time and budget constraints.

Live-lab validation summaries — documented outcomes from interoperability labs and partner integrations that highlight common failure modes and successful mitigations in multi-vendor CNF stacks.

The CNF vendor landscape is shaping into a mix of incumbent network systems vendors, cloud-native software specialists, and platform integrators. Each archetype presents distinct trade-offs for buyers:

Nokia (Espoo) — Strength lies in disaggregated CNFs for packet core and communication suites that are optimized for Kubernetes and carrier-grade reliability. Enterprises benefit from Nokia’s deep telecom lineage bundled with cloud-native architectural advances; buyers should weigh integration velocity against long-term roadmap alignment.

Ericsson (Stockholm) — Ericsson’s push to validate third-party CNFs through an expanded certification program de-risks open network strategies. Operators seeking a neutral, multi-vendor CNF ecosystem will find this particularly valuable; certification translates directly into shorter integration cycles.

F5 (Seattle) — F5’s evolution to cloud-native BIG-IP CNFs and recent releases that add DPU acceleration and provider-edge features signal a focus on performance-sensitive data plane functions. For edge and high-throughput use cases, vendors offering DPU-enabled CNFs can reduce server costs and latency footprints, provided orchestration and platform support are present.

Cisco (San Jose) — With containerized broadband and mobile CNFs, Cisco is positioning to protect incumbent operator relationships while transitioning architectures to cloud native. Their strength is in end-to-end operational tooling, which matters for operators with large legacy estates.

Ribbon Communications (Plano) — Focused CNFs for SBC, policy, and IMS map well to operators undergoing IMS cloudification; smaller, function-focused vendors can be attractive as point solutions but require rigorous interoperability gates.

Titan.ium Platform (Canada) — Microservices-first CNF vendors are accelerating innovation in signaling and subscriber functions, often delivering lighter-weight paths to modern architectures for greenfield deployments and specialist verticals.

Red Hat (Raleigh) — Platform vendors play a multiplier role: supporting CNF lifecycles via OpenShift and partner validations eases operator adoption. Platform support for CNF certification and DPU/edge integrations is an important differentiator.

Recent vendor moves underscore two strategic realities: first, performance and acceleration (e.g., DPU adoption) are migrating from lab proof to product priorities; second, ecosystem-level certification initiatives materially reduce integration risk and accelerate operator adoption. PW Consulting’s vendor profiles map these dynamics to procurement and integration timelines so decision-makers can quantify time-to-revenue vs. vendor risk.

Adopt a layered procurement strategy: separate core CNF selection from lifecycle orchestration and platform provisioning to enable competitive differentiation while leveraging certified platform stacks for risk reduction.

Prioritize lab validation of DPU-enabled CNFs for high-throughput or latency-sensitive services; include observability and crash-diagnostic benchmarks in acceptance criteria given recent product improvements in this area.

Insist on vendor commitments to open certification programs and third-party validations; certified CNFs shorten operator integration timelines and ease multi-cloud portability.

Invest in developer and operations upskilling now — the expanding cloud-native developer community is beneficial, but specialized orchestration and telecom-domain skills remain scarce and will command premium rates if recruitment is deferred.

Run parallel TCO scenarios that include cloud infrastructure, orchestration, traffic growth, and lifecycle management costs; use shock tests (e.g., rapid scale, partial-cloud outages) to validate SLAs and recovery plans.

Concentration metrics indicate a market that is consolidating around providers with strong platform and ecosystem plays, yet still leaves room for focused CNF specialists and platform partners. For strategic buyers, this means a dual-track sourcing approach can capture innovation without increasing systemic risk.

We built the brief to be a decision accelerator: it combines a robust market-sizing model (historical calibration through 2025 and scenario-driven forecasts for 2026–2032), primary interviews with operator and vendor engineering leads, live-lab validation summaries, and procurement-ready artifact templates. The report is intentionally prescriptive — not just descriptive — because 2026 will reward organizations that convert vendor selection and platform decisions into executable roadmaps.

Because this document serves as a strategic preview, we have deliberately withheld detailed subsegment-level figures and proprietary vendor scores to ensure readers engage with the full report and supporting datasets. The full report contains the granular breakdowns, vendor scorecards, scenario worksheets, and a downloadable lab checklist that your integration teams can use immediately.

Download the full PW Consulting Cnf Software Market report for detailed segment-level forecasts, vendor scorecards, and executable deployment artifacts.

Request a tailored briefing: we offer short workshops to map the report’s scenarios to your organization’s migration timelines and to stress-test vendor shortlists against your operating model.

In the rapidly evolving CNF ecosystem, the combination of vendor certification programs, Kubernetes-driven orchestration maturity, and performance acceleration will shape which platforms capture scale and which deployments remain pilot projects. For strategic decision-makers planning 2026 budgets and roadmaps, our analysis supplies the contextual urgency, operational playbooks, and vendor-risk frameworks needed to convert market momentum into measurable outcomes.

For detailed analysis of this topic, please visit the official page:Cnf Software Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com