Green Geopolymer Concrete Market: Strategic Playbook for 2026 Decision-Makers

PW Consulting's latest market research on Green Geopolymer Concrete (GGC) distills industry-scale dynamics and executable strategies that matter for boardrooms, procurement teams, and innovation leads as they finalize 2026 roadmaps. Our analysis combines a rigorous, data-driven growth forecast with hands-on commercial guidance — intentionally presented as a "trailer" to surface actionable insight while directing readers to the full report for granular commercial models and segment-level intelligence.

Green Geopolymer Concrete Market

Executive snapshot

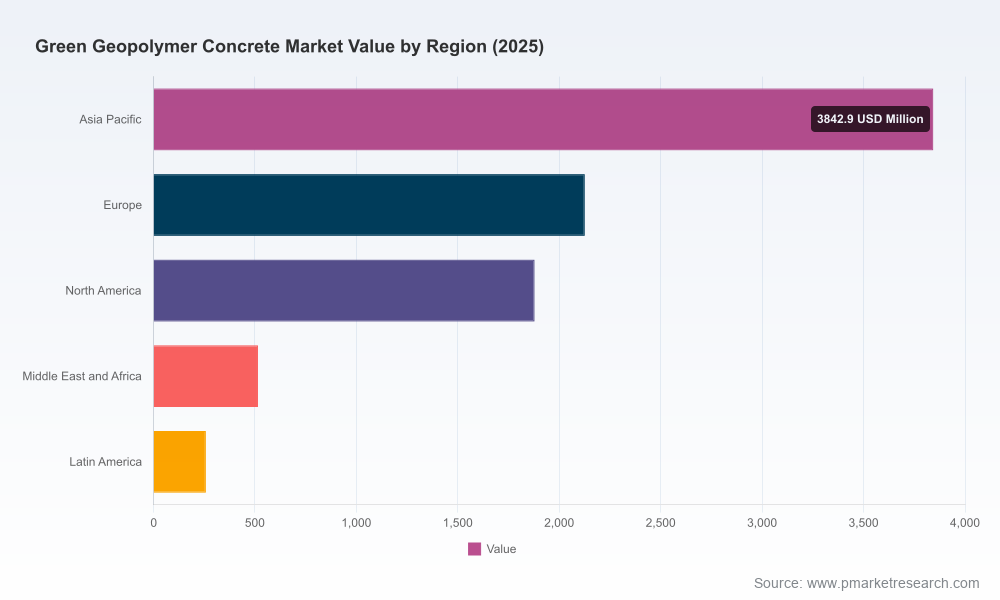

The green geopolymer concrete market is transitioning from niche pilots to industrial-scale adoption. PW Consulting estimates the global market at USD 8,620.45 Million in 2025, with a trajectory that accelerates sharply thereafter. Under our baseline forecast, the market expands at a compound annual growth rate (CAGR) of 25.01% during 2026–2032, reaching USD 41,105.49 Million by 2032. This pace reflects compounding demand drivers: decarbonization mandates, improved precursor availability, and maturing commercial products that meet performance and regulatory thresholds.

Green Geopolymer Concrete Market

Why this matters for 2026 decisions

- Time window for first-mover advantage: High growth and ongoing standardization create a narrow period in 2026–2028 where volume commitments, technology tie-ups, and project references will disproportionately shape market standing through 2030.

- Capex versus procurement trade-offs: Developers and infrastructure owners must balance investment in on-site activation/mixing capacity against supplier-led ready-mix geopolymer solutions. Early alignment with reliable precursor sources de-risks both cost and schedule.

- Regulatory arbitrage: Regions that embed carbon pricing and border adjustment mechanisms are already favoring low-embedded-carbon materials, making geopolymers commercially attractive in tenders that factor lifecycle emissions.

Market structure and concentration — implications for partners and investors

The market remains fragmented: the three largest firms account for approximately 18.5% of market share, and the top five about 28.3%. Fragmentation creates dual opportunities — consolidation playbooks for investors and differentiation pathways for specialized suppliers. For strategic buyers, this means multiple potential partners but variable maturity in product, certification, and supply security. For investors, consolidation through platform roll-ups, or bolt-on acquisitions of niche technology providers, can accelerate scale and market presence.

Green Geopolymer Concrete Market

Competitive landscape — what to watch in 2026

Our competitive review surfaces three categories of incumbents and challengers, each with distinct strategic implications:

- Product innovators with certification-led market access: Firms that have validated performance against fire, chemical, or structural standards gain preferential access to regulated projects. For example, Geopolymer Solutions, LLC secured Underwriters Laboratories certifications in early 2025 for spray-applied fireproofing formulations — a capability that materially expands use-cases in high-safety environments.

- Integrated material-to-project providers: Companies that pair geopolymer formulations with supply-chain integration and project delivery (e.g., shotcrete applications, precast components) accelerate adoption in infrastructure. Wagners’ commercialization of Earth Friendly Shotcrete in mid-2025 and prior deployments in recognized climate-friendly housing projects signal a maturing route to scale.

- Activator and admixture specialists: Suppliers of alkali activators, superplasticizers, and mix-design IP — often partnering with concrete producers — are critical to reproducible performance and site flexibility. Partnerships between formulators and chemical suppliers (as seen in European collaborations) materially shorten certification timelines.

Recent developments that re-shape competitive dynamics

- Geopolymer Solutions’ UL certifications (March 2025) for spray-applied fireproofing broaden application sectors beyond conventional precast and in-situ pours.

- Wagners’ Earth Friendly Concrete (EFC) deployments in certified climate-friendly housing and the July 2025 launch of a zero-cement shotcrete variant suggest a rapid expansion into civil infrastructure and repair markets.

- Commercial partnerships that marry activator chemistry with local manufacturing capacity are accelerating repeatable supply models in mature construction markets.

Raw-material, supply-chain, and regulatory dynamics

Three supply-side realities will dominate procurement strategy in 2026:

- Precursor availability and price volatility: Fly ash and ground granulated blast-furnace slag remain primary precursors. Regional price and supply dynamics diverge — for example, US fly ash prices trended higher in late 2025 with further upward pressure projected into early 2026, while some Asian markets show ample supply and downward price influence. These differentials create arbitrage opportunities for multinational procurement and localizers that secure low-cost feedstock contracts.

- Policy tailwinds: Established approvals — such as national building authority recognitions — materially lower adoption friction. Historical approvals have unlocked residential and public-sector projects and remain a template for approvals elsewhere. Overlying carbon mechanisms (emissions trading and carbon border adjustments) in 2026 are further tilting specification preferences toward low-embedded-carbon concretes.

- Sourcing resilience: As geopolymer adoption scales, buyers must plan for feedstock shifts (e.g., moving from certain fly ash streams to alternative industrial by-products) and invest in flexible mix designs to protect against single-supplier risk.

What PW Consulting’s report delivers (practical, non-theoretical outputs)

Our study is purpose-built for executives who need executable plans — not just charts. Key practical deliverables include:

- Decision-ready financial models: project-level NPV and unit-cost models calibrated to 2026 pricing scenarios and supply contingencies (sensitivity analysis included).

- Procurement playbook: supplier qualification criteria, contract templates, and logistics options for securing precursors and activators across major construction markets.

- Certification and regulatory matrix: a country-by-country checklist showing pathways and timelines to achieve fire, structural, and environmental approvals.

- Commercialization templates: pilot-to-scale roadmaps, performance acceptance testing protocols, and partner-governance models for public-private projects.

- Technology readiness and IP mapping: comparative analysis of mix platforms, activator chemistries, and scalability risks to inform M&A and partnership choices.

- Scenario playbooks: three-tier scenarios (conservative, base, and accelerated adoption) with strategic responses for corporate strategy, sales, and R&D teams.

Actionable recommendations for 2026

Based on our synthesis, PW Consulting recommends the following prioritized actions for decision-makers:

- Lock in feedstock diversity: Negotiate medium-term offtake or tolling agreements with multiple precursor suppliers. A diversified feedstock base (including renewable and biomass ashes where feasible) reduces cost volatility and lowers regulatory exposure.

- Deploy certification-first pilots: Target projects where certification or regulatory acceptance is the gating factor (e.g., fireproofing, critical infrastructure). Early certified installations build transferable references that accelerate tender wins.

- Structure supplier partnerships for technology transfer: For large contractors and precasters, form JVs or licensing arrangements with proven geopolymer formulators to secure technology while retaining control over project delivery.

- Design flexible plant investments: When committing capex to on-site or local production, choose modular activation units that can adapt to alternative precursor chemistries as supply evolves.

- Monitor policy levers: Embed carbon-pricing scenarios into bid evaluation and prioritize projects in jurisdictions with explicit lifecycle-emission scoring in procurement.

Why the full report matters

This release is intentionally selective: it surfaces the strategic contours and near-term tactical choices that underpin successful 2026 execution. The comprehensive report contains the granular, segment-level breakdowns, supplier scorecards, cost build-ups, and downloadable financial models that teams will need to operationalize the strategies summarized here. For organizations evaluating investments, partnerships, or procurement strategies in the next 12 months, that level of detail materially shortens time-to-decision and reduces execution risk.

Next steps

- Download the full PW Consulting Green Geopolymer Concrete Market Report to access segment-level forecasts, supplier matrices, and the customizable financial model.

- Schedule a strategy workshop with our consulting team to tailor the procurement playbook and pilot roadmaps to your portfolio.

- Subscribe to our monthly briefings for ongoing tracking of precursor pricing, certification progress, and competitive moves that will impact 2026–2028 planning windows.

PW Consulting’s market intelligence combines macro forecast rigor with transaction-grade implementation instruments. As 2026 begins, organizations that pair early strategic commitments with flexible supply architectures will capture outsized gains in a market expanding at an annualized 25.01% over the forecast horizon. Our report equips you to make those decisions with confidence.

For detailed analysis of this topic, please visit the official page:Green Geopolymer Concrete Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com