Cloud Advertising Market Trends Driven by Video Advertising Growth

Other |

2026-03-31 07:10:50

As critical technology and emissions-control supply chains reorder themselves for the latter half of this decade, cerium(IV) oxide (CeO2) has moved from a niche industrial commodity to a strategic input for semiconductor CMP, automotive catalysts, and next‑generation energy devices. PW Consulting’s upcoming Cerium(IV) Oxide Market report — anchored on a 2025 base year and a 2026–2032 forecast horizon — synthesizes hard market sizing, supply‑chain stress testing, and executable commercial playbooks to guide boardroom decisions in 2026.

Ceriumiv Oxide Market

Market trajectory: Our topline model pegs the global CeO2 market at roughly USD 1.05 billion in 2025 and projects sustained expansion through 2032 at a compound annual growth rate (CAGR) of approximately 6.2%, reflecting both cyclical recovery in end uses and structural demand from high‑technology segments.

Ceriumiv Oxide Market

Concentration and competition: The market displays a mid‑to‑high level of vendor concentration among a small group of vertically integrated and specialty chemical producers — an important consideration for procurement and M&A strategy.

Ceriumiv Oxide Market

Strategic inflection points: Upstream raw‑material policy, export controls on processing technologies, and localized capacity additions are now the primary determinants of near‑term availability and pricing volatility.

Procurement leads, CTOs, and corporate development teams face three converging forces in 2026: accelerated demand from semiconductor planarization and automotive emissions control, geopolitical constraints on rare earth purification technologies, and margin pressure from raw‑material swings. Our analysis converts these macro trends into concrete actions — from hedging and strategic inventory sizing to targeted investments in purification capacity and process R&D. The report equips C‑suite teams to prioritize capital, select partners, and design contracting frameworks that protect throughput and gross margins.

Demand drivers: High‑precision polishing (CMP) and catalyst formulations continue to lift the share of high‑purity grades. Adoption cycles in semiconductor node transitions and tightening automotive emissions standards are two durable demand pillars.

Supply shocks and policy risk: Two recent developments illustrate systemic risk. First, China’s inclusion of cerium oxide purification technologies on its export control list has materially complicated cross‑border technology transfers and manufacturing partnerships. Second, facility‑level capacity additions outside China — notably recent processing investments commissioned in Australia — are shifting the geographic balance of separation and downstream processing capacity.

Input cost baseline: Industry price reporting and commodity surveys indicate that base cerium oxide feedstock prices remain a sensitive input for finished CeO2 economics, and even modest upstream price moves cascade into polishing slurry and catalyst cost structures.

We recommend three practical scenarios for boardroom stress testing:

Contained disruption: Regional export controls and quotas remain in place but are mitigated by spot market activity and recycled streams. Short‑term price spikes occur but normalize within 12–18 months.

Structural tightness: Export controls deepen, and a combination of environmental shutdowns and geopolitical barriers restrict upstream bastnäsite output. Outcome: longer lead times, selective allocation to incumbent customers, and permanent margin re‑rating for integrated producers.

Decoupled diversification: Demand continues to grow while significant non‑China capacity ramps (processing and purification) create multi‑sourcing options. Competitive dynamics favor players that invested early in vertical integration and quality differentiation.

Our full report provides quantitative P&L and working capital impacts for each scenario, plus break‑even curves and sensitivity matrices that link raw‑material price changes to finished‑goods margins.

The market is a mix of specialty chemical incumbents, rare‑earth processors, and distributors. Peripheral capabilities — whether high‑purity powder synthesis, catalyst washcoat expertise, or precision polishing formulations — determine commercial access to high‑value downstream buyers.

Treibacher Industrie AG (Austria): Specialist in high‑purity powders with strong pedigree in glass polishing and semiconductor lapping; its technical know‑how makes it a natural partner for precision slurry providers.

American Elements (USA): Flexible offer mix (nanopowders, sputtering targets) enables fast response to research and industrial customers; strength lies in catalogue breadth and custom formulations.

Merck KGaA / Sigma‑Aldrich (Germany): Laboratory and technical grades carry strong brand trust in R&D and specialty applications; premium channels make Merck an important barometer for quality thresholds.

Tosoh Corporation (Japan) & Umicore SA (Belgium): Both combine materials expertise with catalyst‑level know‑how, positioning them well for automotive and energy market transitions.

Chinese producers (e.g., Ganzhou Chenguang, Hebei Suoyi): Cost‑competitive supply for industrial applications; their market behavior will continue to influence spot pricing and industrial grade availability.

Lynas Rare Earths Ltd: Recent capacity expansion outside China is strategically significant — the commissioning of additional separation facilities introduces alternative supply pathways for cerium feedstocks, with long‑term implications for global sourcing structures.

PW Consulting’s company profiles in the full report include capabilities maps, manufacturing footprints, margin proxies, and an acquisition target shortlist tailored to buyers seeking either upstream feedstock control or downstream product differentiation.

Export controls and quotas: National controls on purification technologies and rare‑earth production quotas are high‑impact levers that change the economics of cross‑border manufacturing partnerships.

Tariffs and trade measures: Additional duties on imported cerium compounds from certain jurisdictions create a persistent cost wedge for buyers dependent on single‑source suppliers.

Environmental enforcement: Mine and processing site shutdowns on environmental grounds are a plausible near‑term supply constraint that procurement teams must incorporate into inventory and sourcing policy.

We designed the report for implementers. Highlights include:

Market sizing and a detailed 2026–2032 forecast model with transparent assumptions and downloadable scenario inputs.

Supply‑side mapping that traces the value chain from bastnäsite/monazite feed through separation, purification, and finished CeO2 formulation.

Cost build‑up and price sensitivity models (including a commodity price baseline and break‑even analysis by product grade).

Vendor benchmarking (technology, quality, capacity, and strategic intent) with M&A candidate scoring and integration risk diagnostics.

Commercial playbooks — suggested contracting terms, inventory policy, and tiered sourcing strategies for OEMs and slurry formulators.

Regulatory monitoring templates and an early‑warning indicator dashboard to trigger sourcing or capex decisions.

Procurement: Move from single‑tier spot sourcing to a hybrid model combining long‑term off‑take agreements, option contracts, and strategic inventory for critical high‑purity grades.

R&D/Operations: Prioritize investments in in‑house purification or partner with licensed processors to reduce exposure to export‑control bottlenecks.

Corporate Development: Target bolt‑on acquisitions that extend either upstream feed control or downstream formulation capabilities; value in targets is tied to technical depth rather than pure volume.

Risk & Compliance: Implement a policy matrix that maps supplier jurisdictions to tariff exposures and export‑control risks; embed monthly reviews into procurement cadences.

Our estimates combine bottom‑up production and capacity data, company financial disclosures, proprietary pricing feeds, and field interviews with supply‑chain participants. The model’s base year is 2025; the forecast period runs through 2032 and is accompanied by sensitivity testing across demand, policy, and price axes.

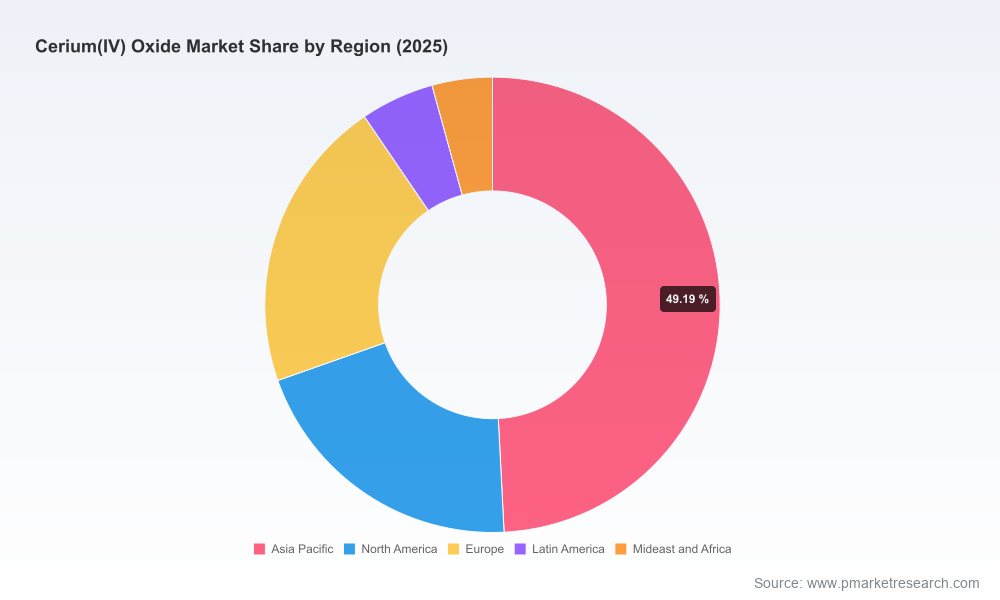

This preview underscores the strategic value of the full Cerium(IV) Oxide Market report for 2026 planning cycles. To preserve strategic confidentiality for our clients and to drive actionable engagement, detailed segment‑level tables (regional and application splits), per‑company capacity figures, and the downloadable forecast model are reserved exclusively for the complete report package.

For boards and operational leaders planning capex, procurement, or M&A activities in 2026, PW Consulting’s full report is the practical toolkit that converts market insight into executable programs. Visit our report page to access the complete dataset, interactive scenario models, and the supplier due‑diligence annex.

For detailed analysis of this topic, please visit the official page:Ceriumiv Oxide Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com