Exosome Therapeutics Market Analysis: Supply Chain, Pricing, and Forecast 2025 –2032

Gardening |

2026-06-16 05:28:12

As organizations reset safety, procurement, and environmental priorities for 2026, the transition from fluorinated aqueous film-forming foams (AFFF) to fluorine-free F3 formulations has moved from regulatory aspiration to operational imperative. PW Consulting's latest F3 Firefighting Foam Market study (base year 2025; forecast 2026–2032) synthesizes regulatory timing, supplier capability, system compatibility, and cost-of-ownership across legacy and next‑generation foam chemistries to help executives make pragmatic, defensible choices in the year ahead.

F3 Firefighting Foam Market

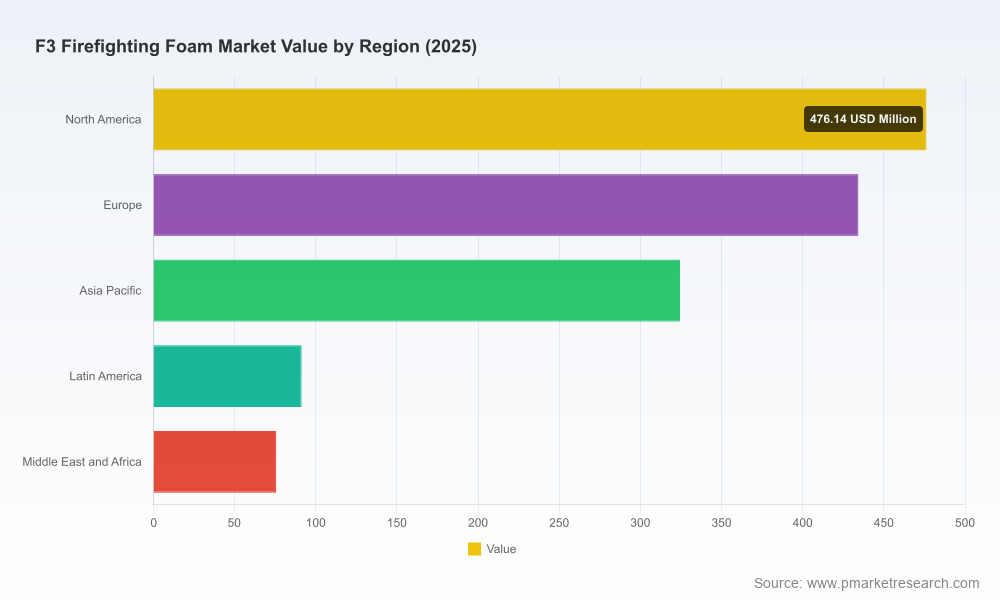

The market for F3 (fluorine-free) firefighting foams has undergone a sustained acceleration. From a mid‑market base in 2020, the industry expanded rapidly through 2025 and is poised to grow materially as transition timelines, product approvals, and replacement cycles converge. Our top‑line model—incorporating historic demand, announced regulatory milestones, adoption lags, and technology rollouts—projects robust expansion through the forecast window, driven by intensified purchasing from airports, oil & gas, maritime, and municipal fleets.

F3 Firefighting Foam Market

Key macro takeaways you should anchor 2026 plans on:

F3 Firefighting Foam Market

For decision‑makers, the timing of regulation and standards activity is the dominant short‑term driver. Multiple regulatory levers reached decisive milestones between 2024 and early 2026—ranging from defense procurement prohibitions and aviation guidance to shipping and regional chemical restrictions. These actions have two practical consequences for 2026 strategy:

Executives should assume that the combination of legislative deadlines and new product certifications will compress decision timelines in 2026 — forcing simultaneous choices on inventory disposition, system compatibility testing, and supplier contracting.

Our study was designed as an operational brief for procurement directors, EHS leaders, risk managers, and investors. It goes beyond market sizing to deliver tools that are immediately actionable:

We intentionally present these deliverables as interactive, model‑driven assets in the full report; the schematic above is illustrative of the capabilities we provide to clients who need to convert strategy into procurement and implementation plans in 2026.

The competitive field combines legacy foam houses with newer fluorine‑free specialists. Leading players have pursued differing strategic plays—some leveraging first‑mover fluorine‑free chemistry and broad certification footprints, others focusing on regional service, specialized formulations for aviation or marine, or integrated training ecosystems. The market shows a mix of concentrated scale and fragmentation in specialty niches; early evidence indicates the winners in 2026 will be those who combine certified product portfolios with strong systems‑integration and after‑sales support.

Prominent firms in our analysis are notable for one or more of the following: early F3 product leadership, MIL‑SPEC/ICAO/FM approvals, bespoke formulations for high‑risk sectors, and investment in training and field support. Recent developments—validations that expand fixed‑system approvals and high‑visibility product launches—are already reshaping vendor shortlists and RFP templates in 2026 procurement cycles.

We built this study to be more than a market map. It’s a playbook for converting regulatory pressure and approval events into executable programs. The report combines a transparent top‑down market model, scenario testing that stresses supply and certification risk, and operational tools—supplier scorecards, retrofit calculators, and staged procurement templates—designed for the next 12–18 months.

Because the most valuable insights are often in the details—segment‑level projections by application, region, and concentration dynamics, as well as vendor‑level performance benchmarks—we intentionally preserve those datasets for the full report and client briefings. Executives who require the underlying tables, proprietary modelling workbooks, or customized transition scenarios will find the full suite indispensable when drafting 2026 budgets or negotiating long‑term supply agreements.

If your 2026 planning cycle touches facility safety, environmental compliance, or critical procurement, PW Consulting can provide the tailored intelligence and implementation support you need to move from policy to practice. The public briefing outlined here is designed to orient senior teams—our full report and advisory engagements provide the segment‑level forecasts, supplier analytics, and contract tools that operational teams use to execute with confidence.

Contact PW Consulting to access the complete F3 Firefighting Foam Market report and to schedule a briefing tailored to your asset base and decision horizon. In an environment where regulatory deadlines, product approvals, and asset life cycles are converging, early, data‑informed action in 2026 will materially reduce cost, compliance and operational risk.

For detailed analysis of this topic, please visit the official page:F3 Firefighting Foam Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com