Seeking the Ideal Balance of Adventure and Peace in the Mountains

Other |

2026-06-26 17:01:15

PW Consulting today publishes an executive briefing accompanying our full market research report, Dust Collectors For Mining Market (Base Year: 2025; Forecast: 2026–2032). This briefing is written from the vantage of PW’s senior strategic advisory team and is intended to help C-suite leaders, procurement heads, and engineering managers make high-confidence decisions in 2026. It presents the strategic implications of our findings without disclosing the report’s full granular splits — the detailed regional, product and process breakdowns are reserved for the full report.

Dust Collectors For Mining Market

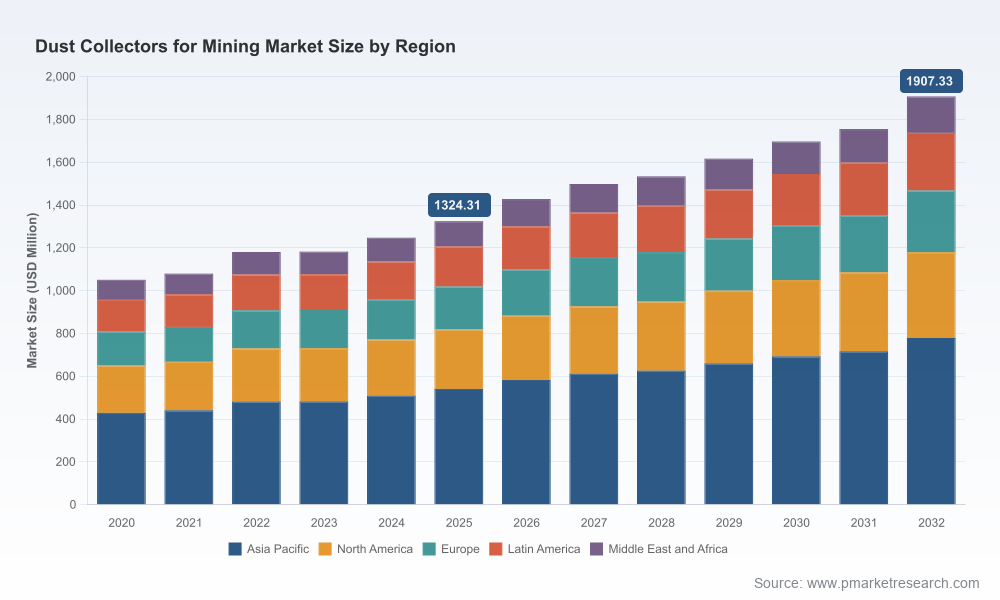

After a measured recovery from 2020–2025, the global dust collectors for mining market enters 2026 with clear momentum. Our market sizing places the industry at approximately USD 1.32 billion in 2025 and projects expansion to roughly USD 1.91 billion by 2032, reflecting a compound annual growth rate (CAGR) of 5.35% across the forecast period. That trajectory is driven by a confluence of regulatory pressure, capital replacement cycles in aging fleets, and the acceleration of engineering-led controls at mine sites.

Dust Collectors For Mining Market

Market structure remains neither a pure oligopoly nor highly fragmented — the top three suppliers account for under a third of global revenue, while the top five approach the mid‑40 percent range. The resulting competitive dynamic favors suppliers that combine robust product engineering, field-proven reliability in abrasive and combustible environments, and scalable aftermarket service models.

Dust Collectors For Mining Market

Regulatory timing compresses decision windows: The Mine Safety and Health Administration’s (MSHA) final silica rule — establishing a uniform PEL and an engineering-controls-first compliance model — places immediate compliance obligations on the mining industry. For many operators, 2026 is the year to convert compliance intention into procurement and retrofitting programs.

CapEx vs retrofit calculus: Mines face a deliberate choice between targeted retrofits to meet regulatory and operational objectives, versus broader equipment refresh cycles. Our analysis shows that well-targeted engineering controls, integrated with modern dust collectors and local capture systems, materially reduce long-term health, environmental and operational costs versus ad hoc administrative measures.

Input-cost volatility matters for equipment design and sourcing: Steel and ferrous material price movements affect manufacturing economics for heavy-gauge collectors. For example, benchmark iron ore pricing trends between 2024 and 2026 exert measurable influence on capex sizing and supplier pricing strategies — an input that procurement teams must stress-test in TCO models.

Engineering-first compliance: Regulatory guidance now emphasizes engineering controls as the primary compliance path. This elevates demand for systems that can demonstrably reduce respirable crystalline silica exposures at source — an emphasis that benefits suppliers able to provide validated performance data and integrated solutions (capture hoods, conveyance enclosures, and downstream filtration).

Performance in harsh environments: Mining dust streams are frequently abrasive, combustible and moisture‑laden. Suppliers that can show field longevity of filtration media, modular serviceability and explosion‑proof design principles will enjoy a procurement advantage.

Service and aftermarket economics: With replacement cycles overlapping mines’ CAPEX constraints, aftermarket service agreements, spare-part availability, and rapid field servicing are differentiators. Total cost of ownership (TCO) conversations increasingly dominate bid evaluations.

Retrofit opportunity set: A sizeable portion of near-term demand is retrofit-driven — older baghouse and cartridge systems require either upgrades to meet new PELs or full replacement where engineering controls were previously insufficient.

The market is populated by a mix of global filtration specialists, regional fabricators, and niche systems integrators. Key established players include:

Donaldson Company, Inc. (Bloomington, Minnesota) — recognized for the Torit® family and a strong portfolio of baghouse and cartridge systems tailored to mining environments.

Camfil APC (Jonesboro, Arkansas) — offers rugged industrial collectors designed for fine particulate (PM2.5/PM10) control and modular deployment in harsh conditions.

RoboVent (Sterling Heights, Michigan) — positions modular Senturion collectors for heavy-duty mineral processing and combustible dust control.

Sly Inc. (Strongsville, Ohio), Imperial Systems, Inc. (Jacksonville, Illinois), C&W DustTech, Ducon Environmental Systems, Scientific Dust Collectors, AAF International, Camcorp, and Baghouse.com — each brings strengths in baghouse systems, wet / dry scrubbers, cyclones, or application-specific engineering for minerals such as phosphate, potash, coal, and hard-rock ores.

Recent industry activity underscores the market’s consolidation around proven engineering solutions: Scientific Dust Collectors showcased mining-focused technologies at 2026 trade events; Albarrie highlighted advanced filtration media at MINExpo 2025; and Superior Industries promoted transfer-point control solutions aligned to MSHA silica standards. These signals point to suppliers emphasizing product validation, field demonstrations, and materials innovation.

Our full report is structured to move executives from awareness to implementation. Elements include:

Market sizing and scenario forecasts (2026–2032) with base-year reconciliation to 2025 and a clear methodology enabling in-house validation and bespoke recalibration.

Regulatory impact modeling that translates MSHA’s silica rule into compliance pathways, timelines and estimated engineering-control obligations by mine type. This section treats regulation as a quantifiable procurement driver rather than a checkbox.

Supplier scorecards and procurement playbooks: side‑by‑side assessments of engineering capability, service footprint, price‑to‑performance, spare‑parts logistics, and explosion‑protection credentials. These are designed to support RFx development and bid evaluation without prescribing a one-size-fits-all vendor.

TCO and CapEx/Opex models: modular spreadsheets that allow teams to stress-test scenarios — including steel-price swings, downtime costs, filter replacement cadence, and regulatory penalty sensitivities — in their own currencies and project windows.

Retrofit decision matrix and implementation roadmap: pragmatic sequencing for site surveys, pilot installations, monitoring plans and scale-up, with sample KPIs that align with health-and-safety and production metrics.

Case study annexes and commissioning checklists: anonymized project briefs that demonstrate how engineering controls translated into measurable exposure reductions and operational benefits, while protecting detailed revenue or installation metrics for confidentiality.

Prioritize engineering audits: Treat a focused engineering audit (source capture mapping, nanoparticle and respirable silica sampling, flow-balance analysis) as a precondition for capital allocation. Audits de-risk procurement and shorten the path to demonstrable compliance.

Model procurement around TCO and availability: Incorporate aftermarket parts availability and service SLAs into bid scoring. A lower initial capex can be outweighed quickly by filter, blower and downtime costs.

Adopt a staged retrofit approach: Small pilot installations with validated exposure reductions can de-risk site-wide rollouts and create precedents for faster permitting and worker buy-in.

Lock in supply-chain contingencies: Given input-material price sensitivity for heavy-gauge assemblies, negotiate price-lock windows and consider alternative materials or modular designs that reduce exposure to raw-material volatility.

Use regulatory timelines to accelerate funding: Align compliance investments with MSHA milestones and leverage demonstrated engineering controls in conversations with insurers and lenders to improve underwriting outcomes.

In keeping with the “trailer” principle, this briefing intentionally omits the detailed regional and application-level numeric breakdowns and the proprietary supplier scoring weightings contained in the full report. Those elements are the core analytic assets of our research product and are provided with the full deliverable to enable site-specific decision-making, RFx templates, and defensible budgeting. If you are evaluating investments, bid strategies, or retrofits in 2026, accessing the full report will materially shorten your decision cycle.

Procurement teams: Use the TCO worksheets and supplier scorecards to structure RFPs that go beyond capex and reflect long-term operability.

Health & safety leaders: Apply the compliance roadmaps and pilot checklists to demonstrate regulatory alignment and measurable exposure reduction within 90–180 day windows.

CEOs and CFOs: Review the scenario forecasts to align mid‑term capital plans with regulatory timelines, and to understand how modest incremental investment in engineering controls can reduce long‑tail liabilities.

For organizations preparing budgets, negotiating supplier contracts, or executing retrofits in 2026, our Dust Collectors For Mining Market report provides the actionable analytics and implementation playbooks needed to turn regulatory pressure into a source of competitive differentiation. To obtain the full report, supplier appendices, and the downloadable CapEx/TCO models, visit PW Consulting’s market research portal or contact our advisory desk for a briefing tailored to your portfolio.

For detailed analysis of this topic, please visit the official page:Dust Collectors For Mining Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com